Module 5 (ppt file)

advertisement

")

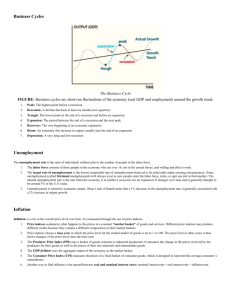

Cory Ando - cra21 Corey Holland - cph9 Ada Nina Johnson-Kanu - aj47 Jenna Watkins - jrw27 Andrew Kuntz - awk6 Where are we now? To see how we are doing now, we need a point of reference, so let us turn back the clocks to look at the past and compare it to our now… Where should we look? To see if we are in a good economic state, let’s look at a bad economic state. The National Bureau of Economic Research defines a recession as “a significant decline in economic activity [that] spreads across a economy…” So lets look a little before the last recession and after it to see how some of this economic activity was affected. FRED – Civilian Unemployment Rate (2006-2011) 4.6% prior to the recession Fluctuated around 5% in early recession Rapid increase throughout recession Peak of 10.1% in October 2009 Typical trend for this leading indicator used to predict the onset of recession. Gradually fell to around 9.5% in July 2010 Rose to 9.8% over the following 4 months Fell to 9.4% in December 2010 Fluctuated around 9% throughout 2011 The present rate of 9.1% is still far from the natural rate of unemployment, but, as a lagging indicator for recoveries, is not necessarily cause for alarm. FRED – Natural Rate of Unemployment (2006-2011) The Congressional Budget Office’s quarterly estimate of the natural rate of unemployment was 5% up until July 2007. The natural rate then rose incrementally to 5.12% at the end of 2008 and 5.2% at the end of 2009, where it has remained. When viewing the civilian unemployment rate in comparison, the effect of cyclical unemployment becomes clear. During 2010 and 2011, the gap between the real unemployment rate and the natural unemployment rate has narrowed. FRED – Consumer Price Index for All Urban Consumers: All Items (2006-2011) Since 2006, there has been a steady rise in the consumer price index (CPI). The end of 2007 through the first half of 2008 saw a rapid rise in CPI. CPI then fell nearly as much as it had risen over the following six months and has increased since that time. Estimated Inflation Inflation estimates are derived from percent changes in CPI, with rapid increases being indicative of the latter stages of an expansion, as has been the case throughout 2010 and 2011. FRED – Gross Domestic Product (2006-2011) Prior to the recession there was continuous growth. When the recession began, GDP was around $14,250 billion. During the recession it peaked at around $14,400 billion and then fell to around $13,850 billion. GDP then began another run of continuous growth, hitting pre-recession levels near the beginning of 2010, and has continued since to the current level of $15,000 billion today. In light of the changes observed in real GDP, the National Bureau of Economic Research’s Business Cycle Dating Committee determined that the U.S. economy entered recovery in June 2009. FRED – Corporate Profits After Taxes (2006-2011) Corporate Profits decreased prior to the recession and deeply troughed mid-recession. Once the recession ended, profits were close to pre-recession figures. Now, profits are greater than those in 2006, indicating that remaining companies are no longer experiencing such adverse effects from the financial crisis. FRED – Private Residential Fixed Investment (2006-2011) Residential investment by people has been decreasing since 2006. ~$415 billion in mid-recession (late 2008) ~$335 billion today The rate of new home construction is one third of the pre-recession level. Distressed and foreclosing properties Stress on financial Institutions Concern over house price declines. Tight credit conditions for builders and homebuyers. FRED – Leading Index for the United States (2006-2011) average weekly hours of production workers in manufacturing; average weekly initial claims for state unemployment insurance; The leading economic index (LEI) utilizes 10 data series to predict economic recessions and recoveries. manufacturers’ new orders for (non-defense capital goods, consumer goods, and materials); supplier deliveries (vendor performance diffusion index); new private housing (authorized by local building permits); stock prices (500 common stocks); M2 money supply (in 2000 dollars); interest rate spread (10-year Treasury bonds less the federal funds rate); University of Michigan’s index of consumer expectations As of early 2009, the LEI has been climbing and is currently at a level greater than pre-recession. Federal Reserve Chairman, Ben Bernanke The U.S. Economic Outlook Speech Exports have grown and the trade deficit has narrowed. September 8, 2011 Improved competitiveness of U.S. goods and services. Manufacturing and production have risen nearly 15% since the trough of the recession. Business investment in equipment and software has expanded. Aggregate output has not returned to pre-recession levels. GDP is estimated to have increased at an annual rate of less than 1 percent, on average, in Q1 and Q2. This can be partially attributed to disaster in Japan, which affected global supply chains and production. The slow economic growth has been ineffective at significantly reducing the unemployment rate. Although consumer spending expanded moderately in 2010, it decelerated in the first half of 2011 due to a reduction in consumer purchasing power due to the rise in commodity prices such as oil. Households are struggling with persistently high levels of unemployment, slow gains in wages, falling house prices, and high debt levels. Conclusion The economy is not in perfect conditions, with high rates of unemployment, it is clear that work still needs to be done. Things are getting better, although, with GDP, the CPI, and corporations making slow but steady recoveries. The economy seems to be starting to come back on track from where it left off when the recession began, as if the recession had just put economic growth on hold. References Bernanke, B. “The U.S. Economic Outlook”. Speech. Sept 2011. The Federal Reserve. Web. 12 Sept. 2011. http://www.federalreserve.gov/newsevents/speech/bernanke20110908a.htm Clayton, G, Geisbrecht, M.G., and Feng Guo. A Guide to Everyday Economic Statistics. Mcgraw-Hill. New York, New York. 7th Ed. Print. Federal Reserve Bank of St. Louis. "FRED Graph " Economic Research - St. Louis Fed. Web. 15 Sept. 2011. http://research.stlouisfed.org/fred2/graph/?g=2c6 Federal Reserve Bank of St. Louis. "Graph: Civilian Unemployment Rate" Economic Research - St. Louis Fed. Web. 14 Sept. 2011. http://research.stlouisfed.org/fred2/graph/?g=2c6 Federal Reserve Bank of St. Louis. "Graph: Consumer Price Index for All Urban Consumers." Economic Research - St. Louis Fed. Web. 14 Sept. 2011. http://research.stlouisfed.org/fred2/graph/?g=2c4 Federal Reserve Bank of St. Louis. "Graph: Corporate Profits After Tax." Economic Research - St. Louis Fed. Web. 14 Sept. 2011. http://research.stlouisfed.org/fred2/graph/?g=2c1 Federal Reserve Bank of St. Louis. "Graph: Gross Domestic Product, 1 Decimal" Economic Research - St. Louis Fed. Web. 14 Sept. 2011. http://research.stlouisfed.org/fred2/graph/?g=2c3 Federal Reserve Bank of St. Louis. "Private Residential Fixed Investment." Economic Research - St. Louis Fed. Web. 14 Sept. 2011. http://research.stlouisfed.org/fred2/graph/?g=2bY Image Sources http://www.worldculturepictorial.com/images/content/be_pleased_technically_not_a_recession_yet. jpg http://s.wsj.net/public/resources/images/OB-KC185_GDP4_E_20100920122215.jpg http://rssbroadcast.com/wp-content/themes/news_10/tools/timthumb.php?src=/wpcontent/uploads/2011/09/BERNANKE-articleInline_4e6981be4995b.jpg&h=180&w=180&zc=1 http://six11.wordpress.com/2010/06/15/living-in-the-present-future/ http://debragrayelliott.blogspot.com/2011/07/if-only-i-could-turn-back-hands-of-time.html