Consumer Credit: Credit

Cards and Student Loans

CHAPTER PLAYLIST SONGS:

“One Piece at a Time” by Johnny

Cash and June Carter Cash

“Ring of Fire” by Johnny Cash

McGraw-Hill/Irwin

Copyright © 2013 by The McGraw-Hill Companies, Inc. All rights reserved.

Learning Objectives

• LO 5-1 Explain the responsibilities, importance,

•

•

•

and cost of credit as well as the options

available for accessing credit.

LO 5-2 Evaluate the features, benefits, and

disadvantages of many different types of

credit cards.

LO 5-3 Describe the mechanics of obtaining and

repaying student loans.

LO 5-4 Assess the benefits and drawbacks of

payday loans, title loans, and rent-to-own

credit options and identify alternatives.

5-2

Credit

A contractual agreement in which a borrower

receives something of value now and agrees to repay

the lender at some date in the future, generally with

interest

Family and Friends

General Purpose Credit Card

Secured

Unsecured

Store Credit Cards

Depository Institutions

Finance Companies

5-3

Friends and Family

Advantages

Friendly money

No credit application

No credit check

Low/no interest rate

Common Uses

First car

Down payment on first

home

Money when needed

quickly

Disadvantages

Can ruin family

relationships through

jealousy and nonpayment

Can cause financial hardship

on the lender

Does not build credit record

Advice

Have everything in writing

Treat it as one of your most

important payments

Refinance with a traditional

lender as soon as possible

5-4

General Purpose Credit Cards

(i.e., Visa, Discover, MasterCard, American Express)

Advantages

Widely accepted

Builds credit record

Buyer protection

Recordkeeping

Miles or cash back

Common Uses

Household items

Auto repair

Auto rental

Airline and hotel

reservations

Online purchases

Disadvantages

High interest rate

Fees and charges

Easy to overspend

Once in credit card debt it is

hard to get out of debt

Advice

Only use credit card for

emergencies

Always repay the full

balance

Pay on time every time

5-5

General Purpose Credit Cards

Secured Credit Cards

Require a deposit to be

held by the credit card

company

Credit limit is the

amount on deposit

Good for starting a credit

file or rebuilding a credit

file after bankruptcy

Unsecured Credit Cards

No deposit required

Credit limit and interest

rate depends on your

income, credit score

No collateral required

5-6

Store Credit Cards

(i.e., Sears, Best Buy, BP, Home Depot, Macy’s)

Advantages

Special Promotion

Recordkeeping

Builds credit record

Buyer protection

Common Uses

Household items

Home repair

Auto repair and fuel

Disadvantages

Only accepted at specific store

High interest rate

Fees and Charges

Easy to overspend

Once in credit card debt, it is

hard to get out of debt

Advice

Always repay the full balance

Pay on time every time

5-7

Depository Institutions

Advantages

Builds relationship with local

lender

Builds credit record

Generally lower interest rates

Oldest form of credit

Common Uses

Automobile

Home improvement

Major purchases

Disadvantages

Higher credit standards

and harder to get the loan

Loans hard to get if under

$1,000

Advice

Build a relationship with

your banker so he/she

knows you

Only take out a loan if you

really need it

5-8

Finance Companies

Advantages

Ease of credit

Some specialize in

specific areas

Will finance lower loan

amounts

Common Uses

Automobile

Home furniture

Major appliances

Disadvantages

Higher interest rates

Fees and charges

Advice

Shop for your best rate and

terms

Only take out a loan if you

really need it

5-9

Characteristics of the Differing Credit Options

5-10

Revolving Line of Credit

Revolving Lines of Credit: You pay a commitment fee and can take and repay

funds at will

Credit Limit: $1,000

Charge: - $300

Balance: $700

How much more you can borrow: $700, Owe: $300

Previous Balance: $700

Payment: $200

Balance: $900

How much more you can borrow: $900, Owe: $100

Previous Balance: $900

Payment: $100

Balance: $1,000

How much more you can borrow: $1,000, Owe $0

5-11

Applying for Credit

Sections of the credit application

Demographics

Income

Assets and liabilities

Contacts

Attest and authorization

5-12

Five Cs of the Credit Decision

Character

Responsibility in repaying loan

Capacity

Enough income minus expenses to pay loan

Collateral

Something of value to secure the loan

Capital

Net worth, other assets that could be sold to pay the loan

Conditions

Economic conditions for specific industries

5-13

Risk and Interest Rates

The higher the risk of not being repaid, the higher

the interest rate charged to offset the risk

Risk determined by your 5 Cs of credit and credit

score

If you have high income, your risk decreases

If you have collateral, your risk decreases because

the lender can sell collateral

If you have a lot of capital (high net worth), your

risk decreases and rates are lower

5-14

Credit Cards

First credit card was in 1950s with Diners Club

1957: American Express and BankAmericard (now

Visa) enter market

In 2010…

Average household credit card debt > $10,000

Average undergraduate credit card debt > $3,000

Average college senior credit card debit > $4,000

5-15

Advantages of Credit Cards

Arbitration

Interest-free loans

Automatic bill

Purchase

payments

Identity theft

safeguards

Credit builder

Extended

warranties

protection

Rental car coverage

Rewards

5-16

Features of Credit Cards

Credit limit – The amount you can borrow without

penalties and fees for over-the-limit transactions

Grace period – The time you have to pay your bill

before finance charges are activated. Not all credit

cards have a grace period

Interest rate – The charge you have for borrowing

money

Can be fixed or variable based on an index rate

Can be very high for some credit cards

5-17

Credit Card Charges and Fees

Finance Charges

Adjusted balance method – Payments or credits received

during the current billing period are subtracted from the

balance at the end of the previous billing period.

Average daily balance method – Most common method.

Every day your balance reflects any charges and/or payments.

Minimum finance charge – The minimum interest that is

charged per billing cycle.

5-18

Doing the Math 5.2

5-19

Fees

Annual - Charge for the privilege of having the card

Cash Advance

A flat fee for the advance

A percentage fee for the amount of money taken

Late-Payment – A penalty fee charged for paying late

Over-Limit – A penalty fee for charging over your credit

limit

Return-Item – A penalty fee for a bounced check

Balance Transfer – A percentage fee for transferring

balance from one card to another

5-20

Errors on Your Statement

According to the Fair Credit Billing Act:

Contact credit card company in writing within 60

days after statement date on the bill with the error

Send letter to “billing inquiries” address on

statement

5-21

Errors on Your Statement, ctd.

Include your name/account number and state the

error, why it is an error, and the date of the error–

and include copies of any supporting documents

Keep a copy; the credit card company will investigate

the complaint and if the charge is found to be in

error, you will not have to pay any interest on the

disputed amount

5-22

Household Use of Credit/Economy Impact

Credit Picture Different for Rich, Poor Households

http://www.npr.org/player/v2/mediaPlayer.html?action=1&t=1&islist=false&i

d=90112615&m=90127338

5-23

Choosing a Credit Card

CC1:

Credit Card Features

Priority

Rank

Rank

CC1 Score

(Priority

Rank*CC1

Rank)*

CC2:

Rank

CC2 Score

(Priority

Rank*CC2

Rank)*

CC3:

Rank

CC3 Score

(Priority

Rank*CC3

Rank)*

APR: purchases

APR: cash advances

APR : balance transfers

APR if you pay late

Interest Rate: fixed, variable or tiered

Grace Period: balance paid off

Grace Period: carry a balance

Grace Period for cash advances

Finance charge calculation: 1 or 2 cycles

Finance charge include/exclude new purchases

Ave or Adjusted finance charge calculation:

Minimum finance charge

Fee: annual

Fee: late payment

Fee: over credit limit

Fee: set-up

Cash Advance: Transaction fee

5-24

Tips for keeping credit card rates and fees low

Select a card based on how you plan to use it

Pay on time

Don’t charge over your credit limit

Maintain balance < 30% of your credit limit

Look out for new fees

Be judicious about all your personal finance activity

Complain if your rates or fees increase

5-25

Student Loan Categories

Federal student loans made directly to the student

Federal student loans made to the parents (PLUS)

Private student loans made to students or parents

Application: Free Application for Federal Student Aid

(FAFSA) www.fafsa.ed.gov.

5-26

Subsidized vs. Unsubsidized Federal Student Loans

Comparison Table

5-27

Student Loan Payments

Student Loan Consolidation and Refinancing

One rate for all your student loans

One lender

Deferment

Delays the repayment of the loan

No interest is accrued for subsidized loans

Forbearance

Can postpone or reduce payments for a specific period of time

Interest continues to accrue

Alternate Payment Options

5-28

Student Loan Payments

Standard Repayment

10 year repayment

$50 minimum payment

Extended Repayment

Not to exceed 25 year repayment

Minimum loan amount of $30,000

Graduated Repayment

Start out low and increase every two years

Up to 10 year repayment

Income-Based Repayment (IBR)

Based on income and family size

Monthly payment less than 10-year standard repayment

Must submit annual documentation to set payment

5-29

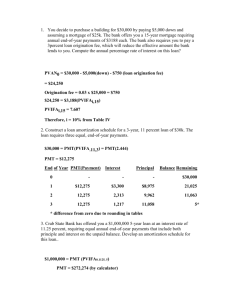

Calculating Payments

PVA = PMT ({1 – [1/(1 + i)n]}/i) where

PVA = Present Value of an Ordinary Annuity

PMT = Payment

i = Interest Rate per Period

n = Number of periods

Example: Financing $1,000 at 12% interest annually (or 1%

monthly) for 1 year making monthly payments:

PVA = $1,000

i = .01

n = 12

5-30

Calculating Payments Formula Example

$1,000 = PMT ({1 – [1/(1 + .01)12]}/.01)

$1,000 = PMT {[1 – (1/1.0112)]/.01}

$1,000 = PMT {[1 – (1/ 1.126825)]/.01}

$1,000 = PMT (1 - 0.887449)/.01

$1,000 = PMT (0.112551/.01)

$1,000 = PMT (11.25508)

Next solve for PMT by dividing both sides by 11.25508

$1,000/11.25508= PMT (11.25508)/11.25508

PMT = $88.85

5-31

Example: Amortization Table $1,000, 1 year, at 12% APR

5-32

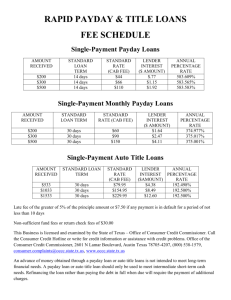

Costly Cash

Payday Loans

Title Loans

Rent-to-Own

Usury Law: State laws that specify the maximum legal

interest rate at which loans can be made

Predatory Lending: Act of lending money at an

unreasonably high interest rate, making repayment

excessively difficult or impossible for the borrower

5-33

Payday Lenders

Short-term loans

Write the payday lender a check for the amount you

want to borrow plus a fee

If you don’t pay off the loan on the specific date,

there is a roll-over fee

Annual percentage rate, including the fees, can be

250% or higher

5-34

Title Loans

Title of an automobile is collateral for the loan

Typically for no more than 25% of the value of the

automobile

Short-term loan

Could lose your vehicle if you don’t repay the loan

High interest rate

5-35

Rent-to-Own

Make purchases with low weekly payments

Effective interest rates very high

5-36

Alternatives to Payday Loans

5-37