CRCT Economics Review Sheet

advertisement

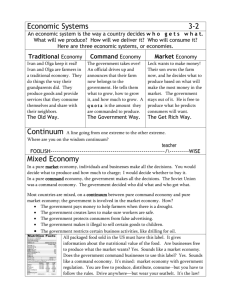

CRCT Economics Review Sheet Command Economy: All major decisions related to the production, distribution, & types of goods and services are all made by the government or central authority. Market Economy: In a market economy, buyers and sellers make economic decisions by spending money on goods and services they want. Traditional Economy: Things are done as they have been done in the past. Economy Type Command Market What to produce? Whatever the government says to produce Whatever consumers say to produce How to produce? However the government tells you to produce However the consumers tell you to produce For whom to produce? For whomever the government tells you to produce (ideally the entire society) For whomever the consumers tell you to produce Traditional Whatever ritual, habit or custom dictates However ritual, habit or custom dictate For whomever ritual, habit or custom dictate No country has a pure command or pure market economic system. Most economies combine market and command economic systems (MIXED) Country Cuba Place on Continuum 5% What to produce? controlled by the government; some small farms owned by individuals How to produce? controlled by the government; some small farms owned by individuals For whom to produce? controlled by the government; some small farms owned by individuals Russia Place on Continuum 30% Government owns large industries but there are some private businesses Government owns large industries but there are some private businesses Government owns large industries but there are some private businesses Brazil Place on Continuum 64% Germany Place on Continuum 65% United Kingdom Place on Continuum 78% Canada Place on Continuum 85% Australia Place on Continuum 95% Mostly decided by private businesses, but some government control of large industries Mostly decided by private businesses, but some government control Mostly decided by private businesses, but some government control of large industries Hard to start a business Mostly decided by private businesses, but some government control Mostly decided by private businesses, but some government control of large industries decided by private businesses decided by private businesses decided by private businesses decided by private businesses decided by private businesses decided by private businesses decided by private businesses easy to start a business decided by private businesses easy to start a business decided by private businesses easy to start a business Mostly decided by private businesses, but some government control Specialization - When one nation can produce a good or service at a lower cost than another nation. Specialization encourages trade. For example, if a country specializes in oil, they can trade oil for a certain food that another country specializes in so that both countries benefit. “Do what you do best; trade for the rest.” Tariff – A tariff is a tax placed on goods that one nation imports from another. Many nations use tariffs to protect their industries from foreign competition. Tariffs provide protection by acting to raise the price of imported goods. Quota – A quota sets a limit on the amount of certain goods that can be imported into a country. Embargo - An embargo is an order designed to stop the movement of goods. No trading!! NAFTA North American Free Trade Agreement: An agreement among Canada, Mexico, and the U.S. to trade without tariffs Exchange Rates - provide a way to determine the value of one country’s currency in terms of another country’s currency. Without a system for exchanging currencies, it would be hard for countries to trade with each other. There are four factors that most influence economic growth in a nation. These are: 1.) Land - Land provides the basic raw materials (natural resources)--plants, animals, minerals, fossil fuels--that are used in the production of goods. 2.) Labor – Work – by machines and people. 3.) Capital (2 kinds; human and physical – defined below) 4.) Entrepreneurship – when people take a risk to start a business Human Capital - education and training of workers Gross Domestic Product – The total value of all goods and services produced within a country in a year. When countries increase capital/human capital, their GDP will also increase. Capital (Physical)- tools, equipment, buildings, and vehicles used in production. The higher the literacy rate of a country the higher the citizens’ standard of living will be. If a country improves its literacy rate, it will also usually improve the standard of living. . . Cuba 5% Pure Command Russia 30% Brazil 64% United Kingdom 78% Continuum Germany 65% Canada 85% Australia 95% Pure Market