1.2 Opp cost

advertisement

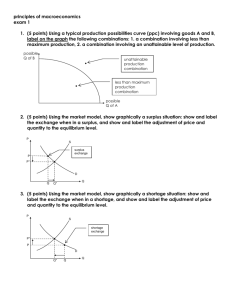

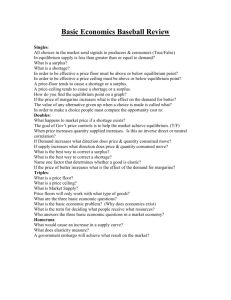

Unit 1 Basic Economic Problems Our wants are UNLIMITED but resources are LIMITED……… So there is SCARCITY Hence we have to make CHOICES 3 major economic questions: •What to produce •How to produce •Whom to produce Basic Economic Problem- 3 decisions • WHAT TO PRODUCE • Food or Clothes • Cars or hospitals • ipods or Cosmetics or military strength Basic Economic Problem- 3 decisions HOW TO PRODUCE techniques used. least cost method of production labour intensive or capital intensive • Production: Creating goods and services • Consumption: Using the goods and services to satisfy want Labor The Enterprise: - Organizes the 3 factors and production process - Takes the risk (Profit and Loss) Opportunity Cost If I ask you, what will you choose?? DEMAND DEFINED What is Demand? Demand is the different quantities of goods that consumers are willing and able to buy at different prices. What is the Law of Demand? The law of demand states There is an INVERSE relationship between P and QD. 12 Income The incomes of consumer change the demand, but how depends on the type of good. 1. Normal Goods – As income increases, demand increases – As income falls, demand falls – Ex: cars, jewelry, homes, TV’s 2. Inferior Goods – As income increases, demand falls – As income falls, demand increases – Ex: instant noodles, used cars, used clothes, 13 Prices of Related Goods The demand curve for one good can be affected by a change in the price of ANOTHER related good. 1. Substitutes are goods used in place of one another. – If the price of one increases, the demand for the other will increase (or vice versa) – Ex: If price of Pepsi falls, demand for coke will… 2. Complements are two goods that are bought and used together. – If the price of one increase, the demand for the other will fall. (or vice versa) – Ex: If price of skis falls, demand for ski boots will... 14 What Causes a Shift in Demand? 5 Determinates (SHIFTERS) of Demand: 1. Market size 2. Expectations of future price 3. Related goods price 4. Income 5. Tastes and preferances Changes in PRICE don’t shift the curve. It only causes movement along the curve. 15 6 Determinants (SHIFTERS) of Supply 1. 2. 3. 4. 5. 6. Prices/Availability of inputs (resources) Number of Sellers Technology Government Action: Taxes & Subsidies Expectations of Future Profit Other – War, weather Changes in PRICE don’t shift the curve. It only causes movement along the curve. 16 Supply and Demand are put together to determine equilibrium price and equilibrium quantity Demand P Schedule $5 P Qd S P Qs 4 $5 10 $5 50 Equilibrium Price = $3 (Qd=Qs) $4 40 3 $4 20 $3 30 $2 50 $1 80 Supply Schedule 2 $3 30 1 o D 10 20 30 40 50 60 70 Equilibrium Quantity is 30 80 Q $2 20 $1 10 17 Supply and Demand are put together to determine equilibrium price and equilibrium quantity Demand P Schedule $5 P Qd 3 $4 20 $2 50 $1 80 S P Qs 4 $5 10 $3 30 Supply Schedule 2 What if the price increases to $4? 1 o $5 50 $4 40 $3 30 D 10 20 30 40 50 60 70 80 Q $2 20 $1 10 18 At $4, there is disequilibrium. The quantity demanded is less than quantity supplied. Demand P Schedule $5 P Qd How much is the surplus at $4? Answer: 20 $4 20 $1 80 P Qs 4 3 $2 50 S Surplus (Qd<Qs) $5 10 $3 30 Supply Schedule 2 $4 40 $3 30 1 o $5 50 D 10 20 30 40 50 60 70 80 Q $2 20 $1 10 19 How much is the surplus if the price is $5? Demand P Schedule $5 P Qd 3 $4 20 $2 50 $1 80 S P Qs 4 $5 10 $3 30 Supply Schedule 2 What if the Answer: price 40 decreases to $2? 1 o D 10 20 30 40 50 60 70 80 Q $5 50 $4 40 $3 30 $2 20 $1 10 20 At $2, there is disequilibrium. The quantity demanded is greater than quantity supplied. Demand P Schedule $5 P Qd S P Qs 4 How much is the shortage at $2? Answer: 30 $5 10 3 $4 20 $3 30 $2 50 $1 80 Supply Schedule 2 o 10 20 30 40 $4 40 $3 30 Shortage (Qd>Qs) 1 $5 50 D 50 60 70 80 Q $2 20 $1 10 21 How much is the shortage if the price is $1? Demand P Schedule $5 P Qd Supply Schedule S P Qs 4 $5 10 Answer: 70 3 $4 20 $3 30 $2 50 $1 80 $5 50 $4 40 2 $3 30 1 o D 10 20 30 40 50 60 70 80 Q $2 20 $1 10 22 The FREE MARKET system automatically pushes the price toward equilibrium. Demand P Schedule $5 P Qd Supply Schedule S When there is a surplus, producers P Qs lower prices $5 50 When there is a shortage, producers $4 40 raise prices $3 30 4 $5 10 3 $4 20 $3 30 $2 50 $1 80 2 1 o D 10 20 30 40 50 60 70 80 Q $2 20 $1 10 23 Where do you get the Market Demand? Frank Yao Ming Other Individuals Market Price Q Demd Price Q Demd Price Q Demd Price Q Demd $5 $4 $3 $2 $1 $5 $4 $3 $2 $1 $5 $4 $3 $2 $1 $5 $4 $3 $2 $1 1 2 3 5 7 P 0 1 2 3 5 P $3 P $3 3 D Q 9 17 25 42 68 P $3 2 D Q 10 20 30 50 80 $3 25 D Q 30 D Q • What you DO NOT CHOOSE is your Opportunity Cost • Opportunity Cost is the 2’nd best option Production Possibility Curve (PPC) • Every decision/choice we make has an Opportunity Cost • This idea of Opportunity Cost can be illustrated using a PPC A Typical PPF …………. Unattainable Opportunity cost of is increasing… Inefficient PPC is also tells you: • What you can and cannot produce • What is the cost of producing the other good Production Possibilities How does the PPC graphically shows trade-offs, opportunity costs, and efficiency? Impossible 14 (given current resources) A B 12 Bikes G C 10 8 Efficient D 6 Inefficient= Unemployment 4 2 E 0 0 2 4 6 8 10 Computers 30 Opportunity Cost Example: 1. The opportunity cost of moving from a to b is… 2 Bikes 2.The opportunity cost of moving from b to d is… 7 Bikes 3.The opportunity cost of moving from d to b is… 4 Computer 4.The opportunity cost of moving from f to c is… 0 Computers 5.What can you say about point G? Unattainable 31