Prices & Decision Making

advertisement

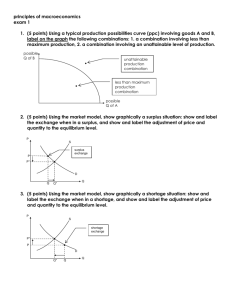

Prices & Decision Making Advantages of Prices • Prices link producers and consumers • prices in a competitive market economy favor neither the producer or consumer – Prices are a result of competition between producers • Prices in a market economy are flexible – Major events can change prices – New technology can change prices • Prices have no cost of administration – Prices happen without outside help or interference – Even when prices change, most people don’t notice because it is gradual. Prices as a System • As long as we have a pricing system we have a way to allocate resources • We don’t have to ration or barter • In a competitive market, we have a market equilibrium = situations where prices are relatively stable, and supply of goods and services is equal to the demand • Surplus = situation where the quantity supplied is greater than the quantity demanded – Surplus turns up as unsold products on shelves and takes up space in suppliers warehouses – Sellers then figure out their prices are too high and have to lower the price to get rid of the surplus • Shortage = a situation in which the quantity demanded is greater than the quantity supplied at a given price – Producers have no more to sell and wish they had charged more for their product – As a result, both price and quantity supplied will go up next time • Equilibrium price = the price that “clears the market” by leaving neither a surplus or shortage at the end of the trading period – When price is too high, the surplus will tend to force it down – When price is too low, the shortage tends to force it up – As a result, the market tends to seek its own equilibrium. Explaining and Predicting Prices • Change in price is normally a result of a change in supply, a change in demand, or changes in both – Changes in Supply: • Example: agriculture experiences big swings in prices • Weather can change the supply, and therefore the price – Changes in Demand: • Changes in income, tastes, prices of related products, expectations, and number of consumers all affect demand for goods and services – Example: gold prices have changed dramatically over the last 20 years – 1980, rising prices, uncertain economic conditions, etc. created high demand for gold – So gold producers opened closed mines and resumed production – This increased the supply and drove the price of gold down