SECURITIZATION FOR THE HOUSING SECTOR

advertisement

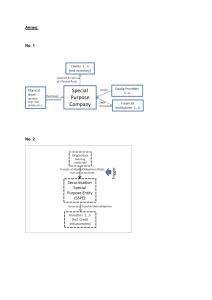

SECURITIZATION FOR THE HOUSING SECTOR Dr. Victor S. Limlingan Asian Institute of Management 18 May 2000 1 Outline I. II. III. IV. V. VI. Background The Promise of Securitization The Process of Securitization The Progress of Securitization Securitization and the Housing Sector Proposed Securitization Plan for the Housing Sector 2 Background: The Philippine Conference on Securitization From July to November of 1999, a private sector group comprised of FINEX, CMDCI, AGILE and AIM-WSPC worked closely with the public sector group comprised of the EMG, HUDCC and DOF to explore the potentials of asset backed securities in developing the Philippine capital market. 3 Background: The Philippine Conference on Securitization On 22 November 1999, after a series of roundtable meetings, the Philippine Conference on Securitization was held to formally addressed the issues raised in the roundtable meetings and focused on the theme: Mobilizing Markets for Housing: The Case for Asset Backed Securities 4 Background: The Philippine Conference on Securitization Specifically the issues discussed were: General market concerns of potential investors in Asset Backed Securities (ABS) Housing Finance Sector Taxation regime with respect to ABS BSP and SEC rules on the issuance and trading of ABS Legislative support for ABS 5 Background: The Philippine Conference on Securitization On the basis of our role as ... Co-Chairman of the Conference and on additional research undertaken after the conference, we have prepared this paper. 6 The Promise of Securitization : SEPARATION ASSET LIABILITY EQUITY SEPARATE ASSET ASSET 7 The Promise of Securitization : TRANSFORMATION MARKETABLE SECURITIES after SEPARATE ASSETS with Future Cash Flow Streams before 8 The Promise of Securitization: MULTIPLICATION BORROWER 1 2 3 COMPANY INVESTOR = CASH 9 The Promise of Securitization Benefits to consumer-borrowers Lower cost of funds Increased menu of credit packages Competitive rates and terms Benefits to originators Readily saleable assets Turnover income Additional service income More efficient use of capital 10 The Promise of Securitization Benefits to investors High yield on rated securities Liquidity Potential trading profits Benefits to intermediaries New product line Underwriting income Potential trading profits 11 The Process of Securitization: Basic Requirements Standard contracts Grading of risk by rating agencies Standardization of applicable rules and regulations Standardization of servicer quality Reliable supply of quality credit enhancers 12 PROCESS FLOW HONG KONG MORTGAGE CORPORATION Mortgage-Backed Securities “Back-to-Back Structure” HOLD SPC BANK A BANK A SELL Sells loans to HKMC Sells loans to SPC Issues MBS with HKMC guarantee to Bank A Bank can hold MBS or sell to other professional investors 13 BASIC STRUCTURE OF ASSET-BACKED SECURITIES 1 BORROWER LOAN ORIGINATOR 4 3 RATING AGENCY 6 2 SPECIAL PURPOSE TRUST CREDIT ENHANCER 5 UNDERWRITER INVESTOR 7 14 The Progress of Securitization in the Philippines Securitization in Non-housing sectors PLDT PAL Securitization in the Housing Sector Citibank MBS PAG-IBIG Urban Bank NHMFC-DOF Thrift Banks 15 Securitization in Non-housing Sectors: PLDT PLDT through Citicorp securitized net settlements, the asset which arises from the imbalance between calls coming into the country from the Filipino diaspora and the much smaller quantity of outgoing calls. Citicorp arranged a US$98m deal for PLDT in December 1997 and a US$ 100m in March 1998 16 PLDT’s SECURITIZATION STRUCTURE PLDT RECEIVABLES RECEIVABLES receives discounted proceeds MBIA Monoline Wrap RECEIVABLES sells receivables every three months CXC Liquidity Facility Provider payments on maturing asset-backed CP Sponsor/ Administrator Source: Asiamoney, ASIA, PLDT INVESTORS Legal Owner 17 Securitization:Housing Sector Business World Archives July 21, 1994 - HIGC to accelerate implementation of mortgage securitization program November 28, 1995 - Yasay vows support for development of asset-backed securities mart May 9, 1996 - NHMFC bats for mortgage securities trading 18 Securitization: Housing Sector January 29, 1997 - Bankers Trust in talks with KBs on securitization June 12, 1997 - Finance pushes secondary mart for mortgage IOUs September 2, 1997 - Guidelines on sale of asset-backed securities drafted October 30, 1997 - BAP, Citibank eye secondary mortgage firm 19 Securitization: Housing Sector March 25, 1998 - Mortgage-backed securities to debut at PSE by October June 2, 1998 - PSE, Urban Bank to formulate rules on trading of asset backed securities April 30, 1999 - Mortgage-backed securities of IFC, Urban postponed 20 Securitization: Housing Sectors December 1, 1999 - FOCUS: A secondary market for housing March 20, 2000 - Government to exempt housing securities from taxes April 25, 2000 MONEY MANAGERS Finding Pag-IBIG Fund's real identity 21 Securitization Housing Sectors: NHMFC-DOF Euroweek May 5,1999 Philippines mulls housing loan sell-off The government aims to either streamline or shut down the operations of agencies which have been responsible for building up portfolios of non-performing mortgage loans averaging 40% to 60% of the total. 22 Securitization Housing Sectors: NHMFC-DOF The Philippine government is envisaging either a straight sale to third parties of both portfolios, totaling Ps42bn ($1.04bn) for NHMFC and Ps38bn ($940m) for Pag-IBIG, or creating a new merged government-owned entity responsible for bad debt workout and improved revenue collection 23 Securitization Housing Sectors: NHMFC-DOF A number of banks including Goldman Sachs, Lehman and Salomon Smith Barney have already put forward proposals. But as one banker said, "This has resulted in very optimistic government projections envisaging the realization of 50% to 70% of face value. The actual prices it should expect to receive will come nowhere near these levels." 24 Securitization Housing Sectors: NHMFC-DOF The government only guaranteed the first 22% of potential losses, so if any part of the portfolio is worth less than 78% of face value, so the three funders will be prepared to absorb the losses themselves from any potential sale. Many bankers doubt whether the government has the political will to absorb losses. 25 Securitization in the Housing Sector Why so little progress for so much promise? 26 Why is there no secondary market for mortgage-backed securities? 1. Secondary market for government securities is practically non-existent 2. Primary mortgage market is weak 3. NHMFC, designed as government secondary mortgage institution is not functioning as such. - Romeo L. Bernardo Former Undersecretary Department of Finance 27 Our Analysis Under a free market system, if there is a demand for a product or service, some entrepreneur motivated by profit and not by public service will come in and supply the the product or service. If not, then we have a market failure. 28 Addressing Market Failure Government takes the initiative to address the market failure - The Malaysian Model: Cagamas Government provides the incentives for the private sector to address the market failure - The Hong Model 29 The Malaysian Model: Cagamas Cagamas Berhad, The National Mortgage Corporation, was incorporated in 1986 to support the Malaysian Government’s policy of encouraging house ownership, particularly of the lower income group. By providing liquidity to the financial institutions and at the same time, to develop the private debt securities market. 30 The Malaysian Model:Cagamas Since commencing operations in October 1987 with an initial bond issue of RM 100 million, the total volume mortgage purchased stood at RM 19,419 million as of end December 1999. As a result, Cagamas has securitized 25.1% of the outstanding loans of the financial institutions as of the end of December 1999. 31 The Hong Kong Model The Hong Kong Mortgage Corporation (incorporated March 1997) creates a market for low-income and middle-income housing loans through purchase of MBS papers, loan guarantees and outright subsidies The Hong Kong Monetary Authority encourages the securitization of highincome housing projects 32 The Hong Kong Model The Hong Kong Mortgage Corporation Limited (HKMC) launched its Guaranteed Mortgage-Backed Securities (MBS) Programme on 22 October 1999 with Dao Heng Bank Limited (DHB). MBS papers provided a new alternative for banks in Hong Kong to liquefy their residential mortgage loans in the market with a powerful new balance sheet management tool. 33 The Hong Kong Model 1997 - HKMA asks banks to reduce mortgage exposure to 40%. Dah Sing Bank mortgages stood at 46%. Dah Sing moved a portion of its residential mortgage portfolio (HK$ 300m) off balance sheet. The transaction enabled the bank to move below the HKMA's 40% limit. 34 The Hong Kong Model 1998 -Without HKMA, any prodding by Deutsche Bank reopened the Hong Kong mortgage securitization market in April 1998. The HK$244.15m transaction was for its own account, parceling a portfolio of mortgages made the previous year. 35 The Hong Kong Model 1999 - Private sector expands securitization The Wharf (Holdings) Ltd undertakes nonJapan Asia's biggest ever securitization. Sino Land Ltd and Chinese Estates Ltd followed. Société Générale repeated that approach in November for Chinese Estates 36 Conclusion While Malaysia and Hong Kong have used securitization to restructure the badly battered real estate sector as well as provide needed liquidity and future market-based rating of the banking system, the Philippines seems to have completely abandoned a promising tool of monetary management. 37 Proposed Securitization Plan for the Housing Sector Conference Resolution #1 Conference Resolution #2 Recommendation 38 Conference Resolution #1 The conference members submitted to the President proposals in the form of a: Draft Executive Order instructing the concerned agencies of government to develop a legal, fiscal and regulatory framework for ABS Draft Securitization Law creating special purpose corporations and secondary market institutions and providing tax incentives for ABS. 39 Conference Resolution #2 The private sector conference participants bound themselves to undertake the following: Endorse to the BSP Governor a framework on a legal and regulatory regime on assetbacked securities Promote the organization and operation of a ‘private sector-led’ SMI 40 Conference Resolution #2 Initiate the standardization primary mortgage market documentation Initiate the creation of a central depository for good titles and the introduction of title insurance 41 Recommendation: Creation of a Public Good Conference resolutions are really seeking the creation of the infrastructure that must be present before securitization of the housing sector can proceed. In order words, a public good must first be produced before private gains can be realized. 42 Recommendation: Champions of Securitization Needed We believe that the infrastructure will be built if: 1. A government agency will act as champion in building the infrastructure; and 2. An entrepreneur will convert the act of securitizing the housing sector into a highly profitable business 43 Recommendation: Build on Existing Infrastructure Moreover, if there is a will, a way will be found to build the infrastructure by building on existing foundations and programs without resorting to the issuance of Executive Orders or the passing of Legislation 44 Recommendation : BSP, the Ideal Champion The government agency who should build the infrastructure is the Bangko Sentral ng Pilipinas (BSP): 1. Banks are the major players in asset securitization as originators, trustees, issuers, servicers and investors 45 Recommendation : BSP, the Ideal Champion 2. Securitization will provide the needed liquidity to some illiquid banks or their illiquid clients. 3. BSP has the technical expertise, the financial credibility and the regulatory power to build the securitization infrastructure. 46 Recommendation : ABS Innovator Needed International Financial Institutions specializing in ABS will be needed given: 1. The apparent lack of interest of the local players without the incentives considered too generous by government agencies; 2. The expertise, the resources and the credibility that these players can provide. 47 Recommendation: Proposed Plan of Securitization BSP invites financial institutions who would be interested in developing a market for Mortgaged Backed Securities in the Philippines. BSP reviews with the interested financial institutions BSP Circular 185 (Series of 1998) as basis for developing the market. 48