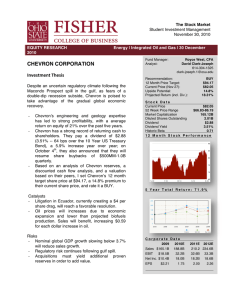

CVX

Chevron Corporation (CVX)

Energy and Natural Resources Coverage Group

Company Overview

• Upstream: exploring and developing oil and gas

– Benefits from high oil prices

– Revenue decrease of 18% in

2014

• Downstream: refining and purifying crude resources

– Benefits from low oil prices

– Revenue increase of 93.4% in

2014

Ticker

Price

Market Cap

Dividend

P/E

EPS

CVX

$106.68

$200.58B

$4.28

10.52

$10.14

• John S. Watson - CEO (2010-present)

– 30+ years of experience with the company

– Variety of managerial roles

• George L. Kirkland (2010-present)

– 40+ years at Chevron

– Engineer turned management

– Head of upstream - most important division

• Pierre R. Breber (2014-present)

– 25+ years as engineer and midstream exec

• Overall: seasoned team with relevant industry experience from both corporate and engineering perspectives

Management

Sector Performance

Thesis Summary

• The market has overestimated the damage of the fall in oil prices on global energy players

• Chevron is in the best position amongst these companies to take advantage of depressed energy prices and subsequent recovery

– Has achieved relatives success in vertical integration (especially transportation services) compared to its competitors

– Effective access to cash allows for expansion of oil projects as firms such as BP are forced to consolidate

– Multiple new projects to be brought online, such as the largest enhanced oil recovery project, and extensive technology development

• Price factors

– Lagging demand: slow global growth – China, Japan, Europe

– Will they recover?

– Increased supply: shale etc.

– Price elasticity of supply?

• Uncertain outlook

• Futures ~50% volatility with 95%

C.I. low price $30 and high end $90

• Supply disruptions in major geopolitical players?

– Iran, Venezuela, Russia

Oil Price Prediction

Rebounding Oil Prices

• Companies within OPEC such as Nigeria (whose oil minister is the president of OPEC) incredibly concerned with depressed prices and are currently in talks to organize future action

– Numerous countries such as Venezuela and Russia need higher oil prices to sustain their budgets

• Domestic producers (especially shale) are maintaining or cutting production, which will lead to less supply and higher prices

Vertical Integration Advantage

• Shell and BP have been investigated for antitrust issues in Europe

• Best hedged against ramifications of energy trade war with China (there are likely

Congressional tariffs on business with Chinese subsidiary companies) due to other companies not having majority control of their Chinese subsidiaries

Cash Advantage

• Chevron assumed leadership and partial ownership of multibillion dollar projects in Gila, Tiber, and the Gulf of Mexico from BP in

January

• Chevron has been increasing investments in the deepest areas of the Gulf of Mexico as other companies have continued to cut investment as well as began pumping from sources that have not been used in over a decade

• Chevron was able to raise $6 billion with bonds to help push through the volatility in oil prices

• Suspension of buy-back program will increase available capital for investment

Project and Technology Advantage

• Manages the world’s largest hyper-efficient, enhanced oil recovery extraction project

– Led to sell off when announced, but critical in in growing market share once oil markets normalize

• Had one of its best exploration years, with important discoveries in the deepwater

Gulf of Mexico, Australia, West Africa and the Permian Basin

• Recently brought a new deep-water oil platform online

– Expected to produce 94,000 barrels per day of oil/21 million cubic feet of natural gas.

• Can generate that 10% breakeven even at oil prices as low as $30 per barrel, and production is forecasted to increase 20% from 2013 industry benchmarks by 2017

• Chevron Technology Ventures is over a decade old and currently has invested over $200 million in start ups and other emerging technologies

Thesis Summary

• The market has overestimated the damage of the fall in oil prices on global energy players

• Chevron is in the best position amongst these companies to take advantage of depressed energy prices and subsequent recovery

– Has achieved relatives success in vertical integration (especially transportation services) compared to its competitors

– Effective access to cash allows for expansion of oil projects as firms such as BP are forced to consolidate

– Multiple new projects to be brought online, such as the largest hyper-efficient oil extraction project, and extensive technology development

Comps Model

Company Ticker Price

Chevron

ExxonMobil

CVX

XOM

$106.68

$88.54

Shell RDS $65.37

BP BP $41.44

ConocoPhillips COP $64.40

Market

Cap

P/E

$200.58B

10.52

$371.40B

11.66

$205.75B

13.87

$125.70B

33.86

$79.31B

11.69

1.3

2.14

1.19

1.13

1.55

P/B Dividend

Yield

4.00%

3.10%

4.70%

5.80%

4.50%

EV/EBITDA

5.90

7.06

5.18

5.28

5.00

Company

Chevron

ExxonMobil

Shell

BP

ConocoPhillips

Ticker Cash

CVX

XOM

RDS

BP

COP

$13.22B

$4.62B

$21.61B

$30.09B

$5.06B

Debt

More Comparatives

$27.82B

$29.12B

$45.54B

$52.85B

$22.56B

Debt/Equity

17.81

16.08

26.36

46.92

43.17

Exploration Failure

Rate

(Last reported year)

30%

39%

N/A

53%

N/A

• Tied to the uncertain oil market

• Downside risk

– Dip into cash reserve?

– Dividend impact?

– Future exploration projects affected by lower per barrel prices

• Ceiling for the foreseeable future?

– CVX vs market expectations

Risk Factors

Why aren’t we worried about Chevron?

• Well-positioned for decline in oil prices

– No real risk of dividend decline

– Ramifications of decline for smaller producers

– Cash on hand

• Not a short-term play

– Dividend in the interim

Downstream Hedge

• In the downstream, CVX completed important investments at

U.S. refineries, which contributed to improved financial and operational performance.

1. New premium lubricants base oil facility in Mississippi.

2. Expansion of additives plants in Singapore and France.

3. Chevron Phillips Chemical Company LLC, achieved startup of the world’s largest on-purpose 1-hexene plant and progressed construction of its new ethane cracker and polyethylene units in Texas.

Downstream

10%

2013

Downstream

20%

Earnings

2014

Upstream

80%

Upstream

90%

Discounted Cash Flow

Targets

• Target price: oil breaks $70/barrel, stock price around $122

• Exit if: oil drops below $35/barrel

• Timeline: 2-2.5 years