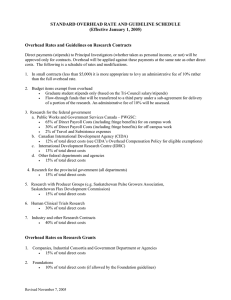

Chapter Nine - McGraw Hill Higher Education - McGraw

advertisement

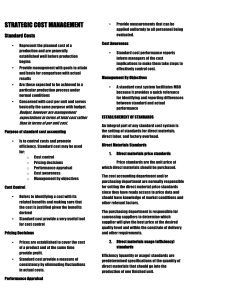

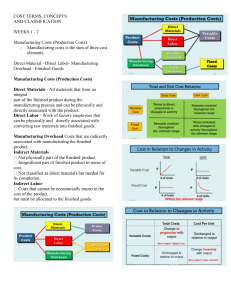

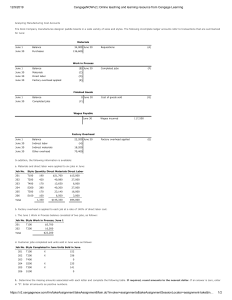

Chapter Ten An Introduction to Management Accounting © 2015 McGraw-Hill Education. Type of User versus Type of Information 10-2 10-3 Components of Product Cost Materials Labor Overhead 10-4 Average Cost per Unit Total Cost Number of Units = Average Cost per Unit For example, Average Cost Per Unit $1,000 4 = $250 10-5 10-6 Labor Costs 10-7 Overhead Costs 10-8 Total Product Cost 10-9 Overhead Costs: A Closer Look Indirect Costs Depreciation Supervisor’s Salary Utilities 10-10 Manufacturing Product Cost Summary Direct Materials Direct Labor Raw material costs that can be easily traced to products. Factory wages that can be easily traced to products. Manufacturing Overhead Other factory costs such as indirect materials and labor, utilities, rent, security, and depreciation. 10-11 The Flow of Manufacturing Costs Through the Accounting Records Balance Sheet Income Statement 10-12 Schedule of Cost of Goods Manufactured The Schedule of Cost of Goods Manufactured summarizes product cost information for manager analyses. Appears on Income Statement 10-13 Inventory Holding Costs Obvious Hidden Decreased Motivation Sloppy work Supervision Theft, damage, obsolescence Financing and Warehouse Space Increased Production Time 10-14 Just-in-Time Inventory JIT Reduction or Elimination of Non-value Added Activities Enables Avoidance of Lost Opportunities 10-15 Ethical Considerations • Certified Management Accountants are guided by the IMA Statement of Ethical Professional Practice • The statement provides standards on – Competence – Confidentiality – Integrity – Credibility – Resolution of ethical conflict 10-16 Benchmarking: Identifying Best Practices of Global Competitors Total Quality Management (TQM) Zero defects and Customer Satisfaction through Continuous Improvement Activity-Based Assessment of the Value Chain to create or Management refine value-added activities and eliminate or reduce non-value-added activities. (ABM) Comprehensive Value Chain Analysis Extends value chain analysis to all suppliers of a company, as well as servicers of the company’s products. 10-17 End of Chapter Ten 10-18