Cost Management and

Decision Making

Chapter 13

Decision making process

Step 1: Goal setting

Provides guidance

Goals

Tangible

Quantifiable

Target profit, market share, enrollment, etc.

Decision making process

Step 2: Gather information

Relevant information

Capable of influencing a decision

Differs among alternatives

Occurs now or in the future

Sunk costs are never relevant

Decision making process

Tradeoffs

Qualitative vs. quantitative

Objective vs. subjective

Accuracy vs. timeliness

Quality vs. cost

Decision making process

Step 3: Identify and evaluate

alternatives

Stay as is or change?

Consider the domino effect

What other changes will this alternative

necessitate?

Decision making process

Costs and benefits of each

Qualitative vs. quantitative

Numbers may not tell the whole story

The past may be a guide

Prototype or pilot project may be

appropriate

Common decisions

Make or buy?

Retain or drop?

Keep or replace?

Accept or reject?

Make or buy?

Make

Qualitative factors

Buy

Qualitative factors

Control

Dependence

Worker morale

Time and distance

Reputation

Greater risk

Reduced risk

Cultural

differences

Make or buy?

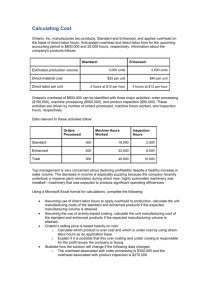

Material

Labor

Variable overhead

Fixed overhead

Total

Unit cost

based on

100,000 units

$

18.00

3.00

2.00

8.00

$

31.00

Purchase price

Shipping

Inspection

Unit cost

based on

100,000 units

$

22.50

0.50

0.25

Total

$

23.25

100,000 units are required each year. Some special-purpose equipment can be eliminated, along

with its operators, if the part is purchased, reducing fixed overhead by $80,000 per year. If

purchased, the capacity freed up could be used to "insource" another component, saving the

company $18,000 per year.

Make or buy?

Assume you chose to buy. Subsequent to your decision you discover you will need an interpreter

($30,000 per year) due to language differences. In addition, you incur travel costs ($60,000 per

year) for your engineers to travel to the supplier to solve problems.

Retain or drop?

Retain

Drop

Profitable?

Revenue lost

Support other

products, locations?

Costs avoided

Maintain image?

Shift to other

products, locations

Impact on

remaining workers,

community

Retain or drop?

Sales revenue

Cost of goods sold

Gross margin

Operating costs

Wages

Utilities

Rent

Fixture depreciation

Insurance

Operating profit

Store A

$ 7,800,000

6,240,000

1,560,000

Store B

$ 3,800,000

3,040,000

760,000

530,000

63,000

210,000

114,000

75,000

568,000

300,000

47,000

115,000

87,000

60,000

151,000

$

$

Store C

$ 1,700,000

1,360,000

340,000

$

Total

$ 13,300,000

10,640,000

2,660,000

230,000

1,060,000

14,000

124,000

80,000

405,000

52,000

253,000

40,000

175,000

(76,000) $

643,000

If store C is eliminated, 10% of its sales will migrate to the other two locations.

In addition, one manager, paid $50,000, will be moved to another store.

Should Store C be closed?

Keep or replace?

Keep

Replace

Serviceability

Cost

Operating costs

Available financing

Capacity

Operating costs

Obsolescence

Capacity

Useful life

Market value of old

asset

Keep or replace?

Existing

machine

Annual operating costs

Materials

Labor

Utilities

Maintenance

Depreciation

Total annual operating costs

Other information

Cost

Accumulated depreciation

Current resale value

Remaining useful life - years

$

$

$

Proposed

machine

38,000

17,000

3,000

4,000

4,500

66,500

$

50,000

22,500

18,000

5

$

$

$

38,000

6,000

1,400

500

18,000

63,900

95,000

5

What costs are relevant? Should the machine be replaced?

Accept or reject?

Accept

Does incremental

revenue exceed

incremental cost?

Unit/batch

Product/facility

Impact on other

products

Impact on other

customers

Reject

Not profitable

Negative impact

on current sales

Discriminatory

Negative impact

on image

Accept or reject?

Annual capacity

Current production, sales level

Selling price per unit

Cost per unit

Materials

Labor

Variable overhead

Fixed overhead

Total fixed overhead

Current production level

Fixed overhead per unit

Total cost per unit

$

$

$

200,000

170,000

25.00

12.00

3.50

1.80

391,000

170,000

$

2.30

19.60

A potential new customer asks the company to produce 50,000 units in special

packaging and offers to pay $20.00 per unit. The special packaging will increase

material cost by $0.10 per unit. Due to capacity limitations, the company will have

to reduce its current sales by 20,000 units if the special order is accepted. Should

the order be accepted? What is the minimum acceptable unit price for the special

order?

Life cycle costing

At some point, all costs must be

recovered

Previous examples only considered

incremental costs

Life cycle costing considers all of the

costs related to owning and using the

asset

Costs are then charged to customers

Life cycle costing

Ownership costs

Net cost consumed (cost – salvage value)

Opportunity cost or cost of capital

Ongoing fixed costs (insurance, taxes, etc.)

Operating costs

Utilities, repairs, maintenance, etc. related

to using the asset

0

0