Consumer Confidence

advertisement

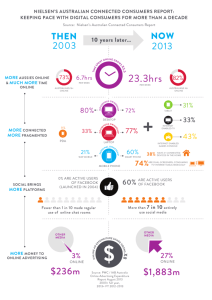

The New Consumer Economy: What to watch and What to do James Russo, Nielsen 1 Title of Presentation Copyright © 2012 2010 The Nielsen Company. Confidential and proprietary. The world has changed Consumers over 65 watch the most TV, close to 7 hours a day Only 5% of advertising targets them, despite being the top buyers in 97% of CPG categories Boomers showed less brand loyalty than their younger counterparts Satisfying their unique need fuels growth for this consumer segment By 2050, ethnic household will be the in the United States Today, 22 of 100 metros are “majority minority” populations Reaching requires resonating With unique connection preferences majority Women control $12 of $18 trillion in global consumer spending—close to 70% Women in 95% of countries say quality is the #1 driver of brand loyalty Transitions strategic conversations from pricing to quality; includes production, marketing, packaging, in-store global middle class will be more than half of the world’s population By 2020, the By 2030, 79% of the middle class will be in the emerging world Business models move from fixed to flexible Accessible Available Mobile Customized Connected Consumer Confidence: Still a global concern HOVERING NEAR PRE-RECESSION LEVELS Global Consumer Confidence Index 102 94 90 90 85 84 92 94 89 88 89 91 77 2H'06 2H'07 2H'08 Q1 Q3 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 2009 2009 2010 2010 2011 2011 2011 2011 2012 2012 Source: Nielsen Global Omnibus Consumer Confidence Survey 2Q2012 EMERGING MARKETS LEAD OVERALL CONFIDENCE AP 101 MEA 98 LA 96 91 NA 87 EU 73 Source: Nielsen Global Omnibus Survey 2Q2012 GROWTH, ONCE AGAIN, BEING DRIVEN BY EMERGING MARKETS Leaders Laggards Movers INDONESIA INDIA PHILIPPINES S. ARABIA MALAYSIA U A EMIRATES BRAZIL CHINA THAILAND HONG KONG 120 119 116 115 111 108 106 105 104 104 HUNGARY PORTUGAL ITALY GREECE CROTIA SOUTH KOREA SPAIN JAPAN FRANCE ROMANIA 30 40 41 43 45 50 52 57 61 62 FRANCE BELGIUM GREECE EGYPT FINLAND SWITZERLAND POLAND AUSTRIA MALAYSIA U A EMIRATES Source: Nielsen Global Omnibus Consumer Confidence Survey 2Q2012, movers vs 1Q2012 +11 +10 +7 +6 +6 +6 +6 +6 +5 +4 U.S. Consumer Confidence: Precarious LET’S GROUND THE CONVERSATION June 2009 NBER May 2012 NIELSEN Recession Officially Ends 75% of consumers say we are in a recession 14 What’s In Store: 2012 Copyright © 2012 The Nielsen Company. Confidential and proprietary. Aug-12 Jun-12 Apr-12 Feb-12 Dec-11 Oct-11 Aug-11 Jun-11 Apr-11 Feb-11 Dec-10 Oct-10 Aug-10 Jun-10 Apr-10 Feb-10 Dec-09 Oct-09 Aug-09 Jun-09 Apr-09 Feb-09 Dec-08 Oct-08 Aug-08 Jun-08 Apr-08 Feb-08 Dec-07 Oct-07 Aug-07 Jun-07 Apr-07 Feb-07 Dec-06 Oct-06 Aug-06 Jun-06 Apr-06 Feb-06 Dec-05 Oct-05 Aug-05 Jun-05 Apr-05 Feb-05 Dec-04 Oct-04 Aug-04 Jun-04 Apr-04 Feb-04 Dec-03 Oct-03 Aug-03 Jun-03 Apr-03 Feb-03 Dec-02 Oct-02 Aug-02 Jun-02 Apr-02 Feb-02 Dec-01 Oct-01 Aug-01 Jun-01 Apr-01 0 Great Recession 20 Source: The Conference Board - Nine census regions, 5,000 US households; 1985 = 100; conducted by Nielsen 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003 2002 140 2001 120 100 80 60 40 Consumer Confidence Index 5 YEARS OF A “NEW NORMAL” CONSUMER CONFIDENCE SIGNIFICANTLY OFF PRE –RECESSION NORMS HEIGHENTED ECONOMIC CONCERNS WHAT ARE YOUR BIGGEST CONCERNS OVER THE NEXT SIX MONTHS…… Economy 27% Debt 11% Jobs 11% Fuel prices 9% Health 8% Source: Nielsen Global Omnibus Consumer Confidence Survey 2Q2012 vs year ago REPAIRING BALANCE SHEETS ONCE YOU HAVE COVERED YOUR ESSENTIAL LIVING EXPENSES, WHAT DO YOU WITH YOUR SPARE CASH….. Savings 40% Paying Debts 33% No Spare Cash 30% Apparel 27% OOH Entertainment 19% Source: Nielsen Global Omnibus Consumer Confidence Survey 2Q2012 vs year ago UTILIZING COPING MECHANISM 52% compare prices before deciding what to buy 47% 41% use coupons +6 +14 use store circulars increase in the coupon redemptions growth of Store Brands in the past 3 years Source: Nielsen Scantrack & Homescan – US Buying Trends June 2012 UNCERTAINTY PERSISTS BUT LESS VOLATILE HOUSING EQUITY MARKETS FUEL COSTS Source: Yahoo Finance; DQNews; ChicagoFed.org; EIA.gov LABOR MARKETS INFLATION U.S. HOUSEHOLD WEALTH DECLINED BY $12 T 0 -5 -10 -$3T HOUSING DECLINE -$9T ALL OTHER BETWEEN Q4 2007-Q4 2008 Source: US Federal Reserve Board Flow of Funds THE WEALTH EFFECT WILL NOT DRIVE RECOVERY EVERY $100 Δ IN HOUSING WEALTH LEADS TO AN ESTIMATED $7 CONSUMER SPENDING. Δ IN OVERALL $500B LOST IN CONSUMER SPENDING BETWEEN 2006 AND 2011. LOW HOUSE PRICE GROWTH FOR AT LEAST 5 Source: The Demand Institute YEARS. RENTAL DEMAND IS LEADING THE RECOVERY 0-2 YEARS STRONG RENTAL DEMAND 3-5 YEARS ACCELERATION OF HOME SALES Source: The Demand Institute SHOPPING HABITS WILL CHANGE MORE FREQUENT SHOPPING & SMALLER BASKETS Source: The Demand Institute MORE ONLINE REPLENISHMENT MORE INTEREST IN LOCAL STORES MORE EXPERIENCE SEEKING CPG NON-DURABLES DEMAND IS SHIFTING DEMAND FOR MORE SMALLER PACK SIZES VALUE-ORIENTED PRODUCTS DUE TO LESS STORAGE Source: The Demand Institute CONSUMERS SEEK FLEXIBLE HOME ENTERTAINMENT PORTABLE DEVICES Source: The Demand Institute INTEGRATED DEVICES Sector Insights WHAT TO WATCH CONTRASTING VIEW OF RETAIL SALES Dollar Sales Unit Sales Source: Total U.S. All Outlets Combined, All Depts. , All Brands (UPC); % Change vs. Year Ago; 13 wk quarters, YTD 31-wks ending 8/4/2012 SHOPPER TRIPS HAVE NOT RETURNED, BUT OTHER DRIVERS AT WORK Economic Growth Great Recession Post Recession 176 158 151 Avg Annual Trips Per Shopper Avg Annual Trips Per Shopper Avg Annual Trips Per Shopper 2002 - 2007 2008 - 2009 2010 - 2011 Source: Nielsen Scantrack, Total U.S. – All Outlets Combined; 52 weeks ending 6/9/2012 (vs. prior year); UPC-coded FRESH DRIVES STORE TRAFFIC AND BASKETS 30% 1.5 to 2.1 Grocery Store Sales Times Larger with Fresh Sources: Homescan, TSV 52 weeks ending December 2011; Nielsen Perishables Group FreshFacts® Total US 52 weeks ending 12/31/2011 (Grocery channel only) AND CAN CREATE A POINT OF DIFFERENTIATION Market Differentiation Top 3 Shopper Equity Retail Brand Quality Prepared Foods Selection of Meat & Fish Quality Fresh Food Customer Service Quality Fresh Food Pleasant Store Environment Long Opening Hours Selection of Fresh Fruit and Veg Pleasant Store Environment Source: Nielsen Shopper Trends 2010 Correspondence Analysis Results Among Dependable Shoppers in retailers’ primary census region #C360 WHILE INNOVATION ACROSS CHANNELS, RETAIL WINNERS AT THE POLES 6% 8% Same Store Sales Growth Same Store Sales Growth VALUE RETAILERS 3% Same Store Sales Growth MAINSTREAM RETAILERS INNOVATION Source: Company financials, most recentSource: reporting:Nielsen Dollar General, DollarTotal Tree, Costco, Scantrack, U.S. – All Sam’s, CVS Macys, Target, Kroger, Rite aid, Wal-mart, Whole Foods, Nordstroms Outlets Combined; 52 weeks ending 6/9/2012 (vs. prior year); UPC-coded HIGH END RETAILERS LOCALIZATION AND CUSTOMIZATION “H.E. Butt Grocery Co…. opened a new store in the Montrose section of Houston Wednesday that will convert part of its parking lot to an outdoor events plaza on weekends for concerts, movies and artisan markets… the chain's first food truck that will serve gourmet items Fridays and Saturdays in the parking lot.” URBAN REVITALIZATION – WALGREENS • 700 fine wines • Fresh sushi & sashimi • Manicures • and, more! Photos: David Schaper / NPR & John Gress / Reuters/Landov Retail 2016 E-COMMERCE: INTENSIFYING AND BLURRING Source: Financial Times & NBC San Diego (photo) U.S. Consumer Trends FORMAT EVOLUTION: NEWER, UPSCALE, SMALL STORE CONCEPTS “The sporting goods company describes its S. A. Elite concept as a boutique store with bright lighting, an open layout, on-site footwear and fitness specialists, and tennis, golf and yoga collections. “ Source: Sports Authority COLLARBORATION: STORE WITHIN A STORE “Apple currently also operates a "store within a store" at over 600 Best Buy locations with "Apple Shops," some of which feature staffing by Apple Solution Consultants. Best Buy has over 1,000 total stores in the US.” Source: Apple Insider & Wired (photo) Retail 2016 RETHINKING MARKETING: DIGITAL BILLBOARDS TO SCROLL CUSTOMER TWEETS Source: Houlihan’s