Capital Structure and Leverage

advertisement

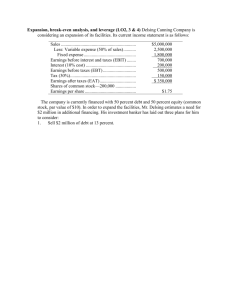

Capital Structure and Leverage • • • • Business vs. financial risk Optimal capital structure Operating leverage Capital structure theory • The use of debt increases the risk borne by shareholders • However, using debt leads to higher expected rates of return by shareholders. • The firm’s optimal capital structure is the one that balances the influence of risk and return and thus maximizes the firm’s stock price. Four factors influence the firm’s capital structure decision 1. Business risk Uncertainty about future operating income (EBIT) if it used on debt The greater the firm’s business risk, the lower its optimal debt ratio 2. The firm’s tax position A major reason for using debt is that interest is deductible, which lowers the effective cost of debt. 3. Financial flexibility This is the firm’s ability to raise capital with reasonable terms under adverse conditions. The greater the probable future need for capital, and the worse the consequences of a capital shortage, the stronger the balance sheet should be. 4. The conservatism or aggressiveness of management Firms with aggressive managers are more inclined to use debt in an effort to boost profits. Business risk is affected primarily by: • • • • Uncertainty about demand (sales). Uncertainty about output prices. Uncertainty about costs. Ability to adjust output prices for changes in input prices. • Operating leverage (the extent to which costs are fixed). What is operating leverage, and how does it affect a firm’s business risk? • Operating leverage is the use of fixed costs rather than variable costs. • If most costs are fixed, hence do not decline when demand falls, then the firm has high operating leverage. • A high degree of operating leverage implies that a relatively small change in sales results in a large change in ROE. • Operating breakpoint The amount quantity at which Sales = Costs, hence when EBIT = 0. Sales = Costs P*Q = V*Q + F Where P is average sales price per unit of output, Q is units of output, V is variable cost per unit EBIT = PQ – VQ- F = 0 Breakeven Q = F/(P-V) EX) Plan A :F = $40,000, P =$4, V=$3, Assets = $ 400,000 Plan B: F = $120,000, P =$4, V=$2 Assets = $ 400,000 BE for A = 40,000 units BE for B = 60,000 units • More operating leverage leads to more business risk, for then a small sales decline causes a big profit decline. Rev. $ Rev. $ } TC Profit TC FC FC QBE Sales QBE Sales • Plan B has a higher expected EBIT (and hence ROE), but this plan also entails a much higher probability of losses. • In general, holding other factors constant, the higher the degree of operating leverage, the greater the firm’s business risk. Probability Low operating leverage High operating leverage EBITA EBITB • Degree of operating leverage (DOL) The degree of operating leverage is defined as the percentage change in operating income (EBIT) that results from a given percentage change in sales. DOL = % change in EBIT / % change in sales Another way to estimate DOL is: DOLQ = Q (P-V) / [Q (P-V) – F] based on output units Q DOLS = S -VC / [S -VC – F] based on dollar sales Assume the quantity produced in the previous example is 100,000 units. For Plan A: DOLQ = Q (P-V) / [Q (P-V) – F] = 100,000 (4-3) / [100,000 (4-3) – 40,000] = 1.67 For Plan B: DOLQ = 100,000 (4-2) /[100,000 (4-2)– 120,000] = 2.5 • The results suggest that if Plan A has 1% increase in sales, it’s EBIT will increase by 1.67%, while for Project B the increase in EBIT will be 2.5%. What is financial leverage? Financial risk? • Financial leverage is the extent to which fixedincome securities (debt and preferred stock) are used in a firm’s capital structure • Financial risk is an increase in stockholder’s risk over and above the firm’s basic business risk, resulting from the use of financial leverage. • The use of debt (financial leverage) concentrates the firm’s business risk on its stockholders. This concentration occurs because debtholders who receive fixed interest payments bear none of the business risk. Business Risk vs. Financial Risk • Business risk depends on business factors such as competition, product liability, and operating leverage. • Financial risk depends only on the types of securities issued: More debt, more financial risk. Consider 2 Hypothetical Firms Firm U No debt $20,000 in assets 40% tax rate Firm L $10,000 of 12% debt $20,000 in assets 40% tax rate Both firms have the same operating leverage, business risk, and probability distribution of EBIT. Differ only with respect to use of debt (capital structure). Firm U: Unleveraged Bad Prob. 0.25 EBIT $2,000 Interest 0 EBT $2,000 Taxes (40%) 800 NI $1,200 Economy Avg. Good 0.50 0.25 $3,000 $4,000 0 0 $3,000 $4,000 1,200 1,600 $1,800 $2,400 Firm L: Leveraged Economy Bad Avg. Good Prob.* EBIT* Interest EBT Taxes (40%) NI 0.25 $2,000 1,200 $ 800 320 $ 480 *Same as for Firm U. 0.50 $3,000 1,200 $1,800 720 $1,080 0.25 $4,000 1,200 $2,800 1,120 $1,680 • Basic Earning Power (BEP) BEP = EBIT / Total Assets This ratio shows the raw earning power of the firm’s assets, before the influence of taxes and leverage. It is useful for comparing firms with different tax situations and different degrees of financial leverage. • Times Interest Earned (TIE) ratio = EBIT / Interest charges A measure of the firm’s ability to meet its annual interest payments. • Coefficient of variation = standard deviation / expected return CV shows standard measure of the risk per unit of return, and it provides a more meaningful basis for comparison when the expected returns on two alternatives are not the same. Firm L Bad Avg. BEP* 10.0% 15.0% ROE 4.8% 10.8% TIE 1.67 2.5 *BEP same for Firms U and L. Good 20.0% 12.0% 8 Avg. 15.0% 9.0% 8 Bad 10.0% 6.0% 8 Firm U BEP* ROE TIE Good 20.0% 16.8% 3.3 Expected Values: 8 E(BEP) E(ROE) E(TIE) U 15.0% 9.0% L 15.0% 10.8% 2.5 Risk Measures: sROE CVROE 2.12% 0.24 4.24% 0.39 For leverage to raise expected ROE, must have BEP > kd. Why? If kd > BEP, then the interest expense will be higher than the operating income produced by debt-financed assets, so leverage will depress income. Conclusions • Basic earning power = BEP = EBIT/Total assets is unaffected by financial leverage. • L has higher expected ROE because BEP > kd. • L has much wider ROE (and EPS) swings because of fixed interest charges. Its higher expected return is accompanied by higher risk. • Degree of financial leverage (DFL) Financial leverage takes over where operating leverage leaves off, magnifying the effect of changes in sales on EPS. For this reason, operating leverage is sometimes referred to as first-stage leverage and financial leverage as second-stage leverage. • The degree of financial degree is defined as the percentage change in EPS that results from a given percentage change in EBIT. DFL = % change in EPS / % change in EBIT. or = EBIT / [EBIT – I] • Jayco has $2 million in sales, variable costs of 70% of sales, fixed costs of $100,000 and annual interest expense of $50,000. If Jayco’s EBIT increases by 10% how much % will its EPS increase? Combining operating and financial leverage So far, we know that: The greater the use of fixed operating costs as measured by DOL, the more sensitive EBIT will be to change in sales The greater the use of debt as measured by DFL, the more sensitive EPS will be to changes in EBIT If a firm uses a considerable amount of both operating leverage and financial leverage then a slight change in sales will lead to wide fluctuations in EPS. The degree of total leverage, which combines the degree of operating leverage and financial leverage, shows how a given change in sales will affect EPS. • DTL = DOL* DFL = (% EBIT/ % sales) * (% EPS/ % EBIT) = % EPS/ % sales DTL = [Q (P-C)] / [Q(P-V)-F-I] DTL = [S-VC] / [ S-VC-F-I ] Ex) How much will Jayco’s EPS increase if the company’s sales increase by 10%?