Long Service Leave Model - Department of Treasury and Finance

advertisement

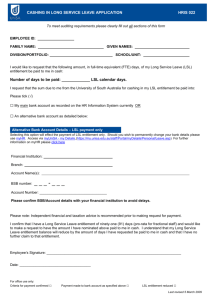

Long Service Leave Model TRIM reference: F07/2109 / D08/53149 Overview and Accounting requirements Anna Hooi, Manager – Accounting Policy Coverage • • • • • • • Background, Process and Consultation Key Features Relevant AAS Prescriptions FRD 17A LSL Wage Inflation and Discount Rates Disclosure Alignment Website Access and User Documentation Implementation Background, Process and Consultation • 2004 LSL Model • 2007 Prototype version - consultation with Depts and VAGO undertaken feedback received, analysed and modifications made retested by selective Depts - further refinements late 2007, briefed VAGO incorporated various VAGO comments • 2008 LSL Model Key Features • • • • • • simplified data input requirements in-built guidance and notes user friendly interface caters for 7 and 10 yr eligibility methodology complies with current AAS relevant to FRD 17A - LSL Wage Inflation and Discount Rates Key Features (cont’d) • alignment with 2008 Model Report for Vic Govt Depts • single weighted average discount rate • optional LSL Model features : - on-costs estimate employee number changes (MOG/admin) quarterly updates indexation factors Relevant AAS Prescriptions • Summary in - LSL Model Overview - 2008 Dept’al Model Report (Note 26 pg 159 – 161, Note 1 pg 83) • AASB 101 Presentation of Fin Statements • AASB 119 Employee Benefits • AASB 137 Provisions, Contingent Liabilities and Assets FRD 17A - LSL Wage Inflation and Discount Rates Requirement: • To calculate the PV of LSL liabilities, an entity must use the wage inflation rate and discount rates advised by the Minister for Finance, unless the entity can demonstrate that an alternative rate is more relevant and reliable • An entity must seek approval from the Minister and consult with the VAGO prior to the use of an alternative rate Disclosure Alignment • LSL Model displays estimates aligned to the 2008 Model Report SCREEN 5 Department of Technology Estimates for incorporation into the Provisions note for the 12 months ended June 2008 Employee benefits (LSL components only) Current Employee benefits: Unconditional and expected to be settled within 12 months $ 52,375 Unconditional and expected to be settled after 12 months $ 426,388 $ 478,763 $ $ 9,852 80,204 $ 90,056 Employee benefits $ 184,826 Provisions related to employee benefit on-costs $ 34,766 $ 219,591 Provisions related to employee benefit on-costs: Unconditional and expected to be settled within 12 months Unconditional and expected to be settled after 12 months Non-current Go to calculations sheet <<Back ? ? ? Print screen Finish>> ? Disclosure Alignment • Extract from the Model Report for Victorian Government Departments Provisions ($ thousand) 2008 Current Employee benefits Unconditional and expected to be settled within 12 months Unconditional and expected to be settled after 12 months 52 426 479 Provisions related to employee benefit on-costs Unconditional and expected to be settled within 12 months Unconditional and expected to be settled after 12 months 10 80 90 Total current provisions Non-current Employee benefits Provisions related to employee benefit on-costs Total non-current provisions Total provisions 569 185 35 220 789 Disclosure Alignment • Model Report v LSL Model Provisions ($ thousand) SCREEN 5 Department of Technology 2008 Current Employee benefits Unconditional and expected to be settled within 12 months Unconditional and expected to be settled after 12 months Estimates for incorporation into the Provisions note for the 12 months ended June 2008 Employee benefits (LSL components only) 52 426 479 Provisions related to employee benefit on-costs Unconditional and expected to be settled within 12 months Unconditional and expected to be settled after 12 months 10 80 Current Employee benefits: Unconditional and expected to be settled within 12 months $ 52,375 Unconditional and expected to be settled after 12 months $ 426,388 $ 478,763 $ $ 9,852 80,204 $ 90,056 Employee benefits $ 184,826 Provisions related to employee benefit on-costs $ 34,766 $ 219,591 Provisions related to employee benefit on-costs: Unconditional and expected to be settled within 12 months Unconditional and expected to be settled after 12 months 90 Total current provisions Non-current Employee benefits Provisions related to employee benefit on-costs Total non-current provisions Total provisions 569 Non-current 185 35 220 789 Go to calculations sheet <<Back ? ? ? Print screen Finish>> ? Website Access – LSL Model 3. 1. 2. User Documentation (1) Overview - High level summary - outline of Model, purpose, the overall methodology, disclosure requirements (2) User Guide - Low level details - Model screen navigation, data reqmts, comprehensive explanation of the methodology including a worked example - FAQs Implementation • Available in new financial year, from 1 July 2008 • Use of 2008 LSL Model not mandatory • Discount rates – despatch continuation • Enquiries on LSL Model - Check FAQs (located in Part D of User-Guide) - Letterbox - AccPol@dtf.vic.gov.au • Future feedback to AccPol@dtf.vic.gov.au Model methodology and assumptions Julie Osborn, Actuarial Adviser, Financial Risk Management Coverage • Data Requirements - First Time Use - Ongoing • Key Assumptions • Model Overview - Output - Methodology - Disclosure Format • Potential Variation Data Requirements – First Time Use • When the model is used for the first time, historical data will be required for: - Nominal value of LSL paid/taken each year Total value of unconditional LSL Nominal value of conditional LSL by years of VPS service Total number of employees Number of employees with >= 1 year of VPS service Number of employees who transfer in or out with >= 1 year of VPS service - On-costs as a proportion of salary/remuneration (optional) - Wage inflation rate - Discount rate Data Requirements – Ongoing • Once the required historical data has been entered it is possible to save the model and simply update it each year by entering data for the current period. Key Assumptions • Discount rate: a single weighted average discount rate is used, in accordance with AASB 119, and based on Reserve Bank of Australia quoted rate • Salary inflation: To allow for promotion, salaries are assumed to increase by 1% more than the DTF projected wage inflation rate. DTF will notify both of these rates on a quarterly basis. Key Assumptions • Payment pattern: The ratio of LSL paid/taken to the total nominal unconditional liability is used to imply the number of years over which the current liability will be paid. This is also used to estimate the LSL amount expected to be paid in the next 12 months • Probability of reaching eligibility period: The average rate of staff turnover, adjusted for transfers, is used to determine the probability of an employee remaining with the organisation until they become eligible for LSL (i.e. 7 or 10 years) Model Overview - Output The LSL model will provide the following outputs: • • • • Current and non-current LSL liability Current and non-current on-costs liability Indexation factor – by years of VPS service Retention rates – by years of VPS service Model Overview - Methodology • Current liability - The value of unconditional LSL is apportioned over future years based on the assumed payment pattern - The amount expected to be paid in the next 12 months is adjusted to allow for salary increases using: Nominal liability compounded wage inflation rate - The amount expected to be settled in each year after the first is inflated and discounted as follows: Nominal liability compounded wage inflation rate ÷ compounded discount rate Model Overview – Methodology (cont’d) • Non-current liability - This represents the present value of unconditional LSL and is calculated by summing the following across each year prior to eligibility for LSL: Nominal liability for y years of service compounded wage inflation rate ÷ compounded discount rate probability of reaching eligibility period - This is then multiplied by the ratio that the current LSL liability bears to the nominal value of unconditional LSL Model Overview – Disclosure Format Department of Technology Discounted Long Service Leave Provision for for the 12 months ended June 2008 Current liability 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 Total On-costs Non current liability Years of VPS service 0 1 2 3 4 5 6 Total On-costs Nominal liability $ 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 50,000 500,000 94,050 Inflated liability $ 52,375 54,863 57,469 60,199 63,058 66,053 69,191 72,477 75,920 79,526 400,000 350,000 300,000 250,000 200,000 150,000 100,000 1,750,000 329,175 553,526 462,373 378,348 300,993 229,875 164,588 104,750 Reported Discounted LSL liability Retention Indexation liability (a) rate (b) factor (c) $ $ 52,375 52,375 49,105 49,105 48,664 48,664 48,227 48,227 47,793 47,793 47,364 47,364 46,938 46,938 46,516 46,516 46,098 46,098 45,684 45,684 478,763 95.8% 90,056 Current Employee benefits: Unconditional and expected to be settled within 12 months Unconditional and expected to be settled after 12 months Provisions related to employee benefit on-costs: Unconditional and expected to be settled within 12 months Unconditional and expected to be settled after 12 months Non-current Employee benefits Provisions related to employee benefit on-costs Other information Discount rate: Inflation rate: Staff retention rate: 375,503 331,545 286,759 241,133 194,656 147,316 99,101 6,286 9,894 15,254 22,866 32,904 44,390 53,232 184,826 34,766 1.7% 3.1% 5.6% 9.9% 17.7% 31.5% 56.1% 1.6% 2.8% 5.1% 9.1% 16.5% 29.6% 53.2% 52,375 426,388 9,852 80,204 184,826 34,766 5.7% 4.8% 56.1% Notes: (a) For the non current liability this is the discounted liability adjusted by the retention rate and the ratio of the present value to nominal current liability. (b) Probability of an employee remaining with organisation until eligible for LSL by years of VPS service. (c) Indexation factor that can be used to allocate total LSL liability to cost centres. Print this sheet <<Back Finish>> Potential Differential • The LSL Model results are likely to differ from those produced by the 2004 Model • This is primarily due to: - discounting all LSL entitlements that are expected to be paid after 12 months; - the use of an average retention rate; and - the assumed payment pattern • While the magnitude and direction of the change is likely to vary by agency, in many cases a lower estimate is expected due to the increased application of discounting Demonstration Clive Brooks, Senior Adviser, Economic and Financial Policy Josephine Galea, Senior Financial Analyst, Accounting Policy Model Report 2008 Anna Hooi, Manager – Accounting Policy TRIM reference: F07/2109 / D08/15429 2008 Departmental Model Report – Main Features • • • • Scope and purpose Published and distributed last week Access from DTF website Accompanying documentation - Summary of Changes - Annual Report Preparation Guide Website Access – 2008 Model Report 3. 1. 2. Model Report 2008 Summary of Changes Report of Operations – Main Changes • FRD 24C Environmental data disclosures • FRD 29 Workforce Data disclosures - FRD 15A Exec Officer disclosures - FRD 22B Standard disclosures • Accounting Officer’s declaration • Machinery of Govt changes reporting • Attestation on Risk Mgmt Financial Report – Main Changes • AASB 7 Fin Instruments disclosure - Overview of AASB 7 Fin Instruments Disclosure Commentary – Operating Statement, Bal Sheet Note 32 Fin Instruments Other changes –Note 4 Income –Note 5 Expenses –Note 10 Receivables –Note 11 Other Fin Assets –Note 24 Payables –Note 25 Interest bearing liabilities –Note 29 Leases Financial Report – Main Changes • • • • • • Machinery of Government changes FRD 103C Non-current Physical Assets Financial guarantees Provisions for employee benefit on-costs Administered Items Note AAS 27, 29 and 31 replacements Appendices • Disclosure Index • Budget Portfolio Outcomes • FRD 24C disclosures Enquiries • Letterbox - AccPol@dtf.vic.gov.au Feedback • Letterbox - AccPol@dtf.vic.gov.au Model Report 2008