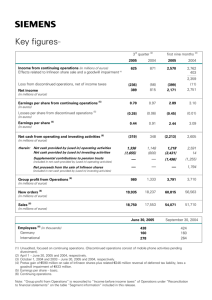

Annual Report 2002

advertisement