Budget Worksheets

advertisement

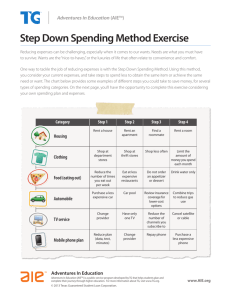

Budget Worksheet Budgeting helps you manage your money more effectively by planning how to allocate your income to cover your expenses. The dual goals of budgeting are: · Spending less than you earn · Increasing your savings People often hesitate to budget, either because they’re not sure how to do it or think they are committing themselves to a rigid system that they can’t possibly follow. Neither is true. Making a budget is fairly simple. And while sticking to your budget can be a challenge, you should think of it as a work in progress rather than a set of rules. In fact, it’s probably wiser to forget the word budget. What you’re developing is a spending plan. And, like most plans, you can expect to do some juggling until it works for you. To learn more about Lightbulb Press visit us on the web at: http://www.lightbulbpress.com This budgeting worksheet was created as a companion to Veterans Handbook, ©2012 Lightbulb Press. To see a sample of the Handbook or to purchase a copy, visit us at www.lightbulbpress.com/bookstore. Or contact us at info@lightbulbpress.com or 212-485-8800. Budget Worksheet: Income Step 1: Calculate Monthly Income Calculate your current monthly household income from all regular sources using the Income Worksheet. This is the amount you can afford to spend each month. Don’t include income from occasional part-time work or gifts you can’t count on receiving each month. When you enter your salary or wages, use net income, which is the amount reported on your pay stub each pay period. If you’re paid twice a month, be sure to add the amounts from both periods to find monthly income. Net income is calculated after federal and state income taxes and FICA taxes have been withheld from your gross income. If health insurance premiums or contributions to retirement savings plans have also been withheld, you do not need to include these amounts as expenses when you get to Step 2. Income Worksheet Income Sources Current Monthly Income Net Salary or Wages Benefits: a) Disability b) GI bill c) Other Interest and Dividends Other Income Total Monthly Income SAVE RESET This budgeting worksheet was created as a companion to Veterans Handbook, ©2012 Lightbulb Press. To see a sample of the Handbook or to purchase a copy, visit us at www.lightbulbpress.com/bookstore. Or contact us at info@lightbulbpress.com or 212-485-8800. Budget Worksheet: Expenses Step 2: Project Your Monthly Spending Allocate your monthly income to cover your expenses by filling in the Proposed Monthly Spending column in the Expenses Worksheet. If you do not have an expense for a particular category, just leave that line blank. If you have a regular expense that’s not included, add it to the list. Base the amounts you enter on what you are spending now for each expense. You can use bank account and credit card statements to find many of these numbers, but you may have to track the things you pay for with cash for several weeks to estimate your current out-of-pocket expenses. Be sure you allocate something to savings each month, concentrating on your emergency fund until you have accumulated three to six months living expenses. Step 3: Compare Your Income and Expenses Add the numbers in the Proposed Monthly Spending column and compare the total with your monthly income. If your proposed spending is more than your income, you need to rework your spending plan. Some expenses, like your rent or mortgage, are fixed. A smart approach is to enter these fixed expenses first and then figure out how much is left to allocate to variable expenses. Variable expenses, such as food and entertainment, can change from month to month and are the places where you can usually economize. Remember, you pay some expenses quarterly or annually. It’s a good idea to budget for those costs each month so you’ll have the money available when you need it. Step 4: Determine Your Actual Monthly Spending At the end of the month, complete the Actual Monthly Spending column using records you keep during the month. Hit Enter on your keyboard to compare what you planned to spend with what you actually spent. If you spent more than you budgeted, you can tackle the problem in several ways. For example, you can: • Analyze the reason for overspending to decide if it is likely to recur • Reallocate your planned spending, moving money from categories where you had a surplus to categories where you had a deficit • Reduce your spending in certain categories Step 5: Track Your Progress Follow the same process every month. At the end of the year, assess how effectively you are managing your money. Ideally, you’ll be spending less than you’re earning so that you can increase your savings. PROVIDED BY LIGHTBULB PRESS. VISIT US ON THE WEB AT: WWW.LIGHTBULBPRESS.COM OR EMAIL INFO@LIGHTBULBPRESS.COM Expenses Worksheet Spending Category Proposed Monthly Spending Actual Monthly Spending Difference Savings: a) Emergency fund b) Retirement c) Education d) Down payment Rent or Mortgage Food and Household a) Groceries b) Supplies Clothing Utilities a) Electric b) Gas/Oil c) Water Childcare Education Expenses a) Yourself b) Spouse c) Kids Communications a) Mobile phone b) Landline c) Internet/Cable Credit Payments a) Credit cards b) Loans c) Other Transportation a) Transit pass b) Car care c) Gasoline Dues/Memberships Insurance a) Medical b) Life c) Auto Out-of-pocket Costs a) Prescription b) Medical copays c) Personal care d) Gifts/holidays Entertainment Miscellaneous Total Monthly Spending SAVE RESET