attachment_id=415

advertisement

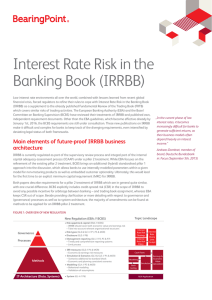

A layman’s guide to BCBS239 In January 2013, the Basel Committee on Banking Supervision (BCBS) issued a document titled “Principles for effective risk data aggregation and risk reporting”. It is generally known as “BCBS 239”.The document sets out guidelines for effective reporting of risk to the board and senior management of banks. So does BCBS 239 matter? Well, if a bank is a SIFI (systematically important financial institution), big enough so that its failure could cause instability in the financial system then it does matter since such banks need to comply with the guidelines, some as early as 2016. But I would argue these regulations are important even if a firm is not a SIFI simply because BCBS 239 describes the best practice of this important topic and does it concisely and clearly. The document says that one of its objectives is enhanced risk management and decision making, and to improve strategic planning – for the ultimate good of the firm and its shareholders. The BCBS has the interests of the taxpayers rather than shareholders in mind. Its motivation for issuing this document arise from the crisis of 2007 when some banks’ Risk functions could not cope and it was impossible to get good risk information for proper decision. In any future crisis, the regulators want the good time risk information to be able to wind-up the bank or perhaps organise a recovery. The document defines 14 principles and groups those into 4 areas; governance, aggregation, reporting and supervisory review. Table 1 summarises these. Table 1 The 14 principles Area Principle # Summary Governance and Infrastructure 1 Strong governance “in the round” 2 Risk IT must be able to cope in a crisis Aggregation 3 Achieve integrity and accuracy via automation 4 Completeness at group level but also drill down to entity 5 Timeliness-especially in the crisis 6 Adaptability-for changing circumstances Reporting Supervisory Review 7 Accuracy through reconciliation and validation 8 Comprehensiveness – include all material risks 9 Clarity - to facilitate informed decision making 10 Frequency of reporting-appropriate to nature of risk 11 Distribution to right people (and only them) 12 Periodic review and spot tests 13 Supervisor’s power to require remedial action 14 Supervisor home/host co-operation Governance and management controls and processes are the overriding preoccupation; these include controls, roles, ownership of data and independent validation. The document draws a rather arbitrary distinction between aggregation and reporting. Aggregation is the gathering all the data together which is a pre-requisite for reporting - providing useful, relevant summaries to inform better decisions. Supervisory review describes the supervisors’ powers to do periodic assessments (including spot tests) and to require the banks to perform remedial action if they fail these tests. These are several themes that resonate through the document. There are many references to ensure risk reporting not only works well in normal circumstances but also in a crisis situation – clearly this reflects the experience of the 2007 crisis. The board and senior management must be aware and in control of all aspects of risk reporting. They must define the information they need and must be aware of the weaknesses and omissions in the reports they receive. This holds true even if they delegate parts of the process to third parties. The buck stops with the board. The document states the ‘what’ but not the ‘how’. There are very few hard and fast rules on how the guidelines should be implemented. The only occasions when the guidelines are explicit are to state that banks must be able to report certain risks intra-day in a crisis situation and to stipulate the minimum content for a risk report. But for the rest, well it depends on what’s appropriate in the firm’s situation. The BCBS prefer automation of risk data processes. They have a strong suspicion of any manual process – these should be the temporary (and well documented and independently validated) exception rather than the rule. “Forward looking” reports are encouraged. These include stress test and scenario-based reports. The entire BCBS239 can be read from start to end in an hour – it is less than 30 pages. For those in hurry, I would suggest starting with Annex 1 which very clearly defines the terms so you appreciate BSBS’s distinction between key terms e.g. the difference between accuracy and precision or between completeness and comprehensiveness. Annex 2 is a summary of the 14 principles. For most people, this will be enough but for more detail, the initial sections cover the motivation behind these regulations, the context and then more background to the principles. BCBS 239 reflects a traditional reporting situation – it assumes that senior management receives their risk data as canned reports – hence their distinction between aggregation and reporting. It assumes a world where the summary risk data is selected as communicated to the board by risk management and risk IT. It does not consider the emerging world of selfreliant and self-service reporting where risk managers have good tools to visually explore and analyse the data. This is probably a reflection of the current status quo in most of the banks. In summary, BCBS 239 is a very useful document and not only for those firms for which the regulations apply. It provides well thought-out, well drafted guidelines with implications for all processes involved in ensuring that the board of a firm can take well informed decisions about the management of their financial risk.