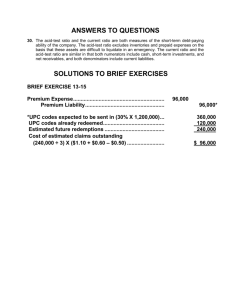

committees_a_latf_exposure_160115_npr_req

advertisement

Exposure of Amendment Proposal

NPR Requirements

Exposed for comment through January 15, 2016

Send comments to Reggie Mazyck

(RMazyck@NAIC.ORG)

Life Actuarial (A) Task Force/ Health Actuarial (B) Task Force

Amendment Proposal Form*

1.

Identify yourself, your affiliation and a very brief description (title) of the issue.

John Bruins, ACLI – Modifications to Net Premium Reserve requirements

2.

Identify the document, including the date if the document is “released for comment,” and the location in

the document where the amendment is proposed:

VM-20, June 18, 2015 adopted version, VM-01 and VM-20

3.

Show what changes are needed by providing a red-line version of the original verbiage with deletions and

identify the verbiage to be deleted, inserted or changed by providing a red-line (turn on “track changes”

in Word®) version of the verbiage. (You may do this through an attachment.)

See following 2 pages

4.

State the reason for the proposed amendment? (You may do this through an attachment.)

This provides for certain edits to clarify the requirements for certain items that have been identified and

concerning or unclear.

* This form is not intended for minor corrections, such as formatting, grammar, cross–references or spelling. Those types of changes do not

require action by the entire group and may be submitted via letter or email to the NAIC staff support person for the NAIC group where the

document originated.

NAIC Staff Comments:

Dates: Received

Reviewed by Staff

Notes:

W:\National Meetings\2010\...\TF\LHA\

Distributed

Considered

VM-01 – Definitions:

23.

A “secondary guarantee” is a guarantee that a policy will remain in force for more than five

1

years (the secondary guarantee period) even if its fund value is exhausted, subject to one or more

conditions.

27.

The term “universal life insurance policy” means a life insurance policy where separately

identified interest credits (other than in connection with dividend accumulations, premium deposit

funds, or other supplementary accounts) and mortality and expense charges are made to the policy. A

universal life insurance policy may provide for other credits and charges, such as charges for cost of

benefits provided by rider.

VM-20 – Requirements for Reserves for Life Insurance Policies

Section 3.

B. For purposes of this Section 3 and Section 6, the following definitions apply:

6.

For any universal life policy with a secondary guarantee period, during the secondary guarantee period

the net premium reserve shall be the greater of the reserve amount determined according to subsection

3.B.5, assuming the policy has no secondary guarantees, and the reserve amount for the policy

determined according to the methodology and requirements subsections 3.B.6.b through 3.B.6.e below.

C. Net Premium Reserve Assumptions

3.

Lapse Rates

a.

For policies that are not a universal life policies or riders containing a secondary guarantee or a

Term policy, the lapse rates used in determining the present values described in subsection 3.B

shall be 0% per year during the premium paying period and 0% per year thereafter.

b.

For Term Insurance policies, the annual lapse rates used to determine the present values described

in subsection 3.B shall vary by level premium period as stated below:

i.

10% per year during any level premium period of less than five years, except as noted in iii.

ii. 6% per year during any level premium period of five or more years, except as noted

in iii.

iii. For any policy with values subject to the requirements of C-45 {Note: C-45 is the

Actuarial guideline that defines NF parameters for ROP Term.} in VM-C, the annual

lapse rate is 6% for the first half of the initial level premium period, and 0% for the

remainder of the initial level premium period

1

Or five years or less if the specified premium for the secondary guarantee period is less than the net level reserve

premium for the secondary guarantee period based on the CSO valuation tables defined in this Section and the

valuation interest rates defined in this Section, or if the initial surrender charge is less than 100% of the first year

annualized specified premium for the secondary guaranteed period.

iv. 10% per year during any premium paying period after an initial level premium period of less

than five years.

v.

For policies or riders having a level premium of five years or longer, the lapse rate for the first

year following that level premium period shall be determined based on the length of the

current and renewal level premium periods and the percent increase in the gross premium per

$1,000 as shown in the table below instead of what would otherwise apply from i or ii above.

Length of

Current

Premium

Period

Length of

Renewal

Premium

Period

Percent increase

in gross

premium per

$1,000

Shock Lapse at

time of

premium

increase

1<PP≤5

1<PP≤5

ART

1<PP<=5

ART

ART

1<PP≤5

5<PP≤10

ART

ART

1<PP≤5

5<PP≤10

10<PP

ANY

ANY

< 400%

Over 400%

ANY

ANY

< 400%

Over 400%

ANY

ANY

ANY

50%

25%

70%

80%

50%

25%

70%

80%

70%

50%

50%

5<PP≤10

5<PP≤10

5<PP≤10

5<PP≤10

10<PP

10<PP

10<PP

10<PP

10<PP

c.

For universal life policies, with a secondary guarantee, the lapse rate, Lx+t, used to

determine the present values described in Subsection B at time t for an insured age x at

issue shall be determined as follow: