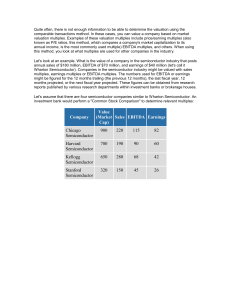

• In relative valuation (i.e. the multiples approach), the

objective is to value assets based on how similar assets are

currently priced in the market.

• While multiples are easy to use and intuitive, they are also

easy to misuse.

• There are two components to relative valuation:

– To value assets on a relative basis, prices have to be standardized,

usually by converting prices into multiples of earnings, book values, or

sales.

– To find similar firms. This is difficult to do since no two firms are

identical and firms in the same business can still differ on risk, growth

potential, and cash flows.

1

• The strengths of relative valuation are also its weaknesses:

– The ease with which a relative valuation can be put together, pulling

together a multiple and a group of comparable firms, can also result in

inconsistent estimates of value where key variables such as risk,

growth, or cash flow potential are ignored.

– The fact that multiples reflect the market mood also implies that using

relative valuation to estimate the value of an asset can result in values

that are too high when the market is overvaluing comparable firms, or

too low when it is undervaluing these firms.

– While there is scope for bias in any type of valuation, the lack of

transparency regarding the underlying assumptions in relative

valuations make them particularly vulnerable to manipulation.

2

• The most common multiples used are:

–

–

–

–

–

Price-earnings (PE) ratio

Price-book (PB) ratio

Price-sales (PS) ratio

Enterprise value/EBITDA

Enterprise value/Sales

3

Major classifications of multiples

• Price multiples – ratios of a stock’s market price to some

measure of fundamental value per share

• Enterprise value multiples – relate the total market value of all

sources of a company’s capital to a measure of fundamental

value for the entire company

4

Price to Earnings (P/E)

• Alternative definitions

– Trailing P/E

• a stock’s current market price divided by the most recent 4 quarters’ EPS

– Forward P/E

• also called the leading P/E

• A stock’s current price divided by next year’s expected earnings

• Rationales for using the P/E

– Earnings power is a chief driver of investment value

– It is widely recognized and used by investors

5

• Drawbacks

– EPS can be zero, negative, or insignificantly small relative to price, and

P/E does not make economic sense under these circumstances

– Tends to be highly variable because it reflects leverage

– The ongoing or recurring components of earnings that are most

important in determining intrinsic value can be practically difficult to

distinguish from transient components

– Differences in accounting standards adopted by firms may affect the

comparability of P/Es among companies

• Fundamental factors that could explain differences in P/Es

– Growth in EPS: companies with a higher growth rate are expected to

have higher P/Es

– Risk (measured by beta or leverage): companies with lower risk can

have higher P/Es

6

Price to Book Value (P/B)

• The ratio of the market price per share to book value per

share

• Most useful for valuing companies composed chiefly of liquid

assets, such as finance, investment, insurance, and banking

institutions

• Rationales for using the P/B

– Because book value is a cumulative balance sheet amount, book value

is generally positive even when EPS is zero or negative

– Book value per share is more stable than EPS. May be more

meaningful than P/E when EPS is abnormally high or low or is highly

variable

7

• Drawbacks

– Some assets (e.g., human capital, company reputation) are not

reflected on the balance sheet

– P/B may be misleading when the levels of assets used by the

companies under examination differ significantly. Such differences

may reflect differences in business models.

– Accounting effects on book value may compromise how useful book

value is as a measure of the shareholders’ investment in the company

• e.g. Intangible assets that are acquired are shown on the books; those that are

generated internally are not (R&D, advertising, marketing are expensed not

capitalized)

– Book value largely reflects the historical purchase cost of assets, net of

accumulated depreciation. Significant differences in the average age of

assets among companies being compared may weaken the

comparability of P/Bs among companies

– Share repurchases or issuances may distort historical comparisons

• Fundamental factors that could explain differences in P/Bs

– Return on Equity

– Risk

8

Price to Sales (P/S)

• The ratio of the market price per share to annual net sales

• Most useful for valuing certain types of privately held

companies, including investment management companies

and many types of companies in partnership form

• Appropriate for valuing the stocks of mature, cyclical, and

zero-income companies

• Rationales for using the P/S

– Sales are generally less subject to distortion or manipulation than are

other fundamentals, such as EPS or book value

– Sales are positive even when EPS is negative

– P/S is generally more stable than P/E

9

• Drawbacks

– A business may show high growth in sales even when it is not

operating profitably as judged by earnings and cash flows from

operations

– Sales is a prefinancing income measure while share price reflects the

effect of debt financing

– P/S does not reflect differences in cost structures among different

companies

– Although P/S is relatively robust with respect to manipulation, revenue

recognition practices have the potential to distort P/S

• Fundamental factors that could explain differences in P/Es

– Profit margin

– Growth in EPS

– Risk

10

Enterprise Value to EBITDA (EV/EBITDA)

• The ratio of the enterprise value to EBITDA

– EV = MV of Equity + MV of Debt + MV of Pref Shares – Cash and M/S

– EBITDA = Net income + Interest expense + Taxes + Depreciation +

Amortization

– Alternative denominators: EBITA, EBIT

• Frequently used in the valuation of capital intensive

businesses such as cable companies and steel companies

• Rationales for using the EV/EBITDA

– EV/EBITDA is usually more appropriate than P/E alone for comparing

companies with different levels of debt. EBITDA is a pre-interest

earnings figure; EPS is post-interest

– EBITDA controls for differences in depreciation and amortization

among business, in contrast to net income.

– EBITDA is frequently positive when EPS is negative

11

• Drawbacks

– EBITDA will overestimate cash flow from operations if working capital

is growing.

– Free cash flow to the firm (FCFF), which directly reflects the amount of

the company’s required capital expenditures, has a stronger link to

valuation theory than does EBITDA

• Fundamental factors that could explain differences in

EV/EBITDA

– Return on Capital

– Growth in FCFF

– Risk (as measured by WACC)

12

Enterprise Value to Sales (EV/Sales)

• The ratio of the enterprise value to sales

• Alternative sales-based ratio that is particularly useful when

comparing companies with diverse capital structures

13

• How do we use multiples?

–

–

–

–

Compare with a firm’s historical multiples

Compare with sector multiples

Compare as a ratio to the S&P multiple

Valuation

• Sum-of-the-parts valuation

14

• Sources:

– Pinto, Henry, Robinson, & Stowe, “Equity Asset Valuation”,

2nd ed.

– Damodaran, Investment Valuation, 2nd ed.

– McKinsey & Company, Koller, Goedhardt, and Wessels,

Valuation: Measuring and managing the value of

companies, 5th ed.

15

0

0