Intro-to-Valuation

advertisement

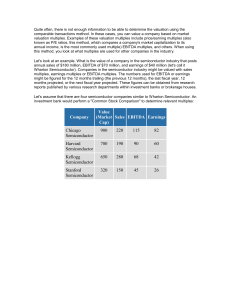

LIBOR Introduction to Valuation Why Valuation? Most important concept in Investment Banking Determining how much a company is worth Why do we need this? M&A (how much should I pay for target?) Equity (pricing shares) Debt (maximum debt capacity) Valuation This is not an exact science There is no ‘black box’ approach to valuation Depends greatly on banker’s judgments All valuations will be biased Cannot rely on just one method, each has its flaws Multiples Numerator= Measure of value Denominator= Operating Statistic Examples: P/E (What is this multiple really?) Market Cap/Net Income More commonly used on Wall Street are EV multiples (EV/EBITDA) Aside: Why is EV/NI not used? EV flows to both debt and equity holders, NI flows only to equity holders EV/EBITDA Break Down EV/EBITDA EV= Enterprise Value, commonly called Firm Value Market Cap + Total Debt – Cash & Cash Equiv Think: How much money would be needed to buy the whole company? EBITDA= Earnings Before Interest, Taxes, Depreciation and Amortization What is Firm Value? Example Company Acquirer wants to buy Company Target Company Target sells at $10 per share They have 100,000 shares outstanding What is the Market Cap? $1,000,000 Example Cont. But that’s not it, if A buys T they also take on their debt This is going to increase the total price of the purchase Example Cont. But what about Cash? If T has Cash, A can use it to pay down some of that Debt This is going to decrease the total price of the purchase Example Cont. Market Cap= $1,000,000 Add $1,000,000 in debt Subtract $500,000 in cash FV= $1,500,000 What is EBITDA? Metric to evaluate profitability Not GAAP, so there’s no legal requirements Strips out many expenses that may cloud actual performance EBITDA: What am I taking out and Why? Interest: It’s a function of management’s financing choices Taxes: Can vary widely depending on prior losses or acquisitions D&A: Subjective judgments like useful lives, different methods Now it’s easier to compare companies Comparable Companies Analysis Comps Reflects current valuation Can be affected by market conditions and sentiment Also called Public Market Comps You can only perform this with Public Companies due to the amount of information needed Step 1: Select Your Universe I am trying to value Company A As the name suggests, I need Comparable Companies These are similar public companies, peers, competitors Look for similar sectors/sub-sectors, products, geography, size Realistically you also ask your Associate/VP, they have immense sector and industry knowledge Step 2: Get the Financial Information Once I have my Comparable Companies, Locate financial information What drives value? both past and future performance Past Information- SEC filings, press releases Future Information- Research reports, consensus Step 3: Spread the Comps ‘Spreading’ Entering/Updating financial data and calculating statistics/ ratios/ trading multiples Calculate valuation measures: Mkt Cap, Equity Value, Firm Value And earnings measures: EBITDA, Net Income This is getting us to MULTIPLES Why Can’t we just use Yahoo Finance or Something? Things like Mkt Cap and FV may be available there, but You need to calculate earnings measures and valuation measures from scratch (this means inputting #’s like revenue, interest, shares outstanding, etc.) Allows for greater control and the ability to adjust just one piece People are going to want to know how you got to that number and why it’s so low/high You can’t trust it, they are often wrong or don’t take into account options/converts/one-time items What if it’s in between reporting periods? Did I not sell anything in that time period? If it were that easy, you wouldn’t have a job Step 4: Benchmarking I calculated the financial stats, used some Excel formulas to show my ratios and trading multiples Now, which are the closest, most relevant comparables Elimination of outliers, Creation of ranges for stats and multiples Determine Valuation Trading multiples of the Comparable Companies allow us to derive a value for the target Apply the range of multiples to Company A Some Simple Algebra I found that the average EV/EBITDA for my comps is 10x I know my financial statistics, EBITDA = $500,000 What is my EV? EV/EBITDA=10x EV/$500,000=10x EV=$5,000,000 Note that I will often be using estimated forward financial stats and multiples Pros and Cons Pros Based on actual public market data, reflects market’s expectations Can be updated based on day-to-day market data (What impact would a change in the price of a comp’s stock have?) Cons Market based- What happens if there’s excessive bearishness/a bubble? Relevant Comps may not exist Not an intrinsic valuation, not based on cash flow Precedent Transactions Analysis Precedents Similar to Comps Looks at multiples paid for comparable companies in past M&A deals Will always give you the highest valuation, why? If I am looking at what A paid for T 6 months ago, A likely paid a premium for T. This is because A saw the opportunity for synergies and needed to pay more than the market price for T Step 1: Universe This time I need a universe of similar companies that have been bought recently I’m looking at targets, why wouldn’t I care about buyers? Step 2: Get the Info I now need financial information for the M&A activity Proxy statements, 8K, 10K/Q Step 3: Spreading Enter key financial data such as purchase price, the target’s financial stats Use Excel to calculate multiples You’re going to end up with EV/EBITDA (or comparable multiple) and use that to find your firm’s EV Pros and Cons Pros Objective, I’m not making assumptions Market-based, based on what companies actually paid for similar companies Cons These deals, by definition occurred in the past Hard to find comps, harder to find precedents Hard to find info on some transactions Discounted Cash Flow Analysis DCF The value of a company is derived from the present value of its future cash flows What cash flows? Free Cash Flow How do I discount it to PV? WACC This is establishing an intrinsic value (as opposed to market value) Step 1: Project Free Cash Flow Projected for 5 years This is actually unlevered FCF Unlevered FCF= Cash that a company is able to generate after laying out money to maintain/expand its asset base This is the cash that could be paid out to lenders and investors How do I grow FCF? use growth assumptions developed by historical performance and expected sales growth rates, margins, capex, etc. Step 1 Cont. Why 5 years? by this time the company is deemed to have reached a ‘steady state’ Formula: EBIT * (1-Tax Rate) + D&A -Δ Net Working Capital -Capex = Unlevered Free Cash Flow Step 2: WACC We know that Present Value= Future Value/(1+i)n So we have FV (the FCF), now what do we discount this by? WACC= Weighted Average Cost of Capital Step 2 Cont. Every company has a capital structure made up of Debt and Equity Any investor in our company needs to be compensated, how much depends on whether they are taking on the risk of owning equity or owning debt What is the Cost of Equity? CAPM Cost of Debt? usually the current yield on outstanding issues (it’s complex and it’s DCM’s job) Step 2 Cont. So say rd =5% and re =10% My company’s cap structure is 70% debt and 30% equity Now we weight these WACC= (rd * (1-T) * % debt) + (re * % equity) What’s that tax rate doing? Interest paid is often tax deductible What happens after year 5, does the company cease to exist? No, use Terminal Value Step 3: Terminal Value (Perp Method) This will give us the value of all future FCF for the company beyond those 5 years How many years is this projecting out? 10, we use the final years FCF as a starting point We know WACC too, but what is g? Perpetuity growth rate= long-term growth rate usually b/t 2 % and 4% Step 4 Set up your formula, input your numbers Discount each cash flow for the 5 years, sum this, and add it to you TV calculation This number is equal to your company’s Firm Value Pros and Cons Pros Insulated from the market Based on cash flows, a very fundamental and intrinsic valuation Allows for flexibility (I can change factors affecting FCF in future periods) Cons Are your forecasts accurate? How much of my valuation is consumed by TV? (it’s often ¾’s or more) Small changes lead to big differences So What do you do Now? Combine Valuation Methods Think about which Method you feel is most accurate You can combine and weight them to come out with a number How to Pretend that you’re a Banker Turn it Gray Blue=Input, Black=Calculation, Green=Link to other sheet Center Across Selection Go back to the old Office Turn off your Excel Gridlines Unplug your Mouse Use Shortcuts Customize your Keyboard How quick are you? Sources Investopedia.com Investment Banking by Josh Rosenbaum and Josh Pearl