Tax Credit Pilot Case Studies

advertisement

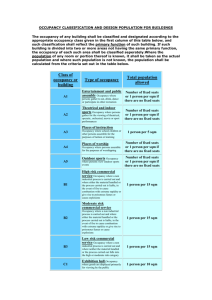

Tax Credit Pilot Case Studies Midwest Lender’s Conference – June 2013 Auburn Manor Acquisition and rehab of 100% Section 8 Project Tax exempt bonds with 4% tax credits; 223 (f) loan, GNMA swap program Project had been rehabbed prior to tax exempt bond financing; prior rehab counts for tax credits but not for meeting the bond requirements 3 tests for tax exempt bond financing (transaction must meet all three): 50% test: total tax exempt bonds issued must equal 50% or more of total transaction costs 95% test: 95% of bonds must be used for good costs: acquisition and rehab 15% test: rehab must equal at least 15% of acquisition cost less land that is financed with tax exempt bonds . Rehab must be incurred within 2 years after closing and no earlier than 60 days prior to the tax exempt bond inducement Example: Total project cost = $9 million; minimum $4.5 million of tax exempt bonds must be issued 95% test: $4,275,000 must be spent on good costs Acquisition cost = $6 million, value of land is $275,000 15% test: acquisition cost financed with bonds = $4,275,000 less land = $4 million; minimum rehab is 15% of $4 million or $600,000 Valley at Cobb Park Refinance of newly rehabbed 168 unit tax credit project under the waiver of the 3 year rule Existing project that was gut rehabbed and was 50% occupied at completion; 100% of the units restricted to 60% AMI Occupancy requirements for waiver: Sustaining Occupancy for 3 months prior to endorsement; 85% physical occupancy 3 months prior to endorsement. Sustaining occupancy for project calculated to be 83%. Project has a waiting list of over 400; Completion estimated to be June 30; 100% occupancy estimated by August 15. Sustaining occupancy and 85% test estimated early August. 3 month tests require closing not before November 1. Submission July 15, Firm Commitment September 15, closing November 1 Underwriting Issues Both projects incorporated green initiatives such as insulation, windows, HVAC systems, water saving appliances and fixtures. Historical utility costs were therefore not relevant; there are firms specializing in estimating utility costs going forward based on the specific type of renovation involved HUD requires the valuation NOI be based on market rents and expenses, therefore two NOIs have to be concluded by the appraiser and lender. Typical differences include: Higher market rents and tenant charges for market rate properties Higher advertising expense for market rate properties Higher payroll, administrative and management expenses for LIHTC properties