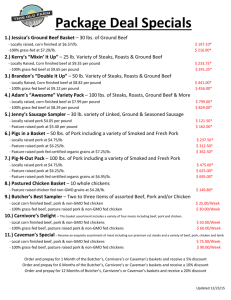

PowerPoint - dkerby.com.

advertisement

UNIT 1 ENTREPRENEURSHIP AND THE ECONOMY SUPPLY AND DEMAND HOW ARE PRICES DETERMINED? In a free market system(capitalism) • By the marketplace Sellers: Want the price to be the MOST they can CHARGE. Buyers: Want the price to be the LEAST they can PAY. ECONOMIC SYSTEMS • Pure market system: prices are set in the marketplace based on supply and demand with little government interference. • Command economic systems are run by a strong centralized government that decides how resources will be used and sets prices. • Mixed economies combine the principles of market and command economies. Ex: many prices are set in the marketplace but government laws set restricts to eliminate monopolies, price fixing, ripping off consumers. DEMAND • Demand refers to the quantity of goods or services consumers are willing and able to buy. Therefore: • When the prices goes UP, demand goes DOWN. • When the price goes DOWN, demand goes UP. Page 11 in text DEMAND ELASTICITY • The demand for some products and services is more effected by economic conditions such as price than others. • Elastic demand: demand IS effected by price. • Inelastic demand: price is NOT effected by demand. This is more likely when there is no substitute available and means you can charge more without affecting demand. • The law of DIMINISHING MARGINAL UTILITY says that price alone does not determine demand; other factors (income, taste, etc.) also play a role. Page 13 in text SUPPLY • Supply refers to the quantity of goods or services producers are willing and able to provide to the marketplace. Therefore: • When the prices goes UP, supply goes UP. • When the price goes DOWN, supply goes DOWN. Page 13 in text EQUILIBRIUM • Equilibrium is the price point where the demand meets supply, and consumers will buy all of a product supplied by producers. Pages 11 - 13 in text SCARCITY • Scarcity occurs when demand exceeds supply. This plays a large role in setting prices for some goods and services. Page 11 in text QUESTIONS • What might be considered scarce in today’s marketplace? • Think about it: At what price would you demand a cell phone? • • • • $50? $100? $150? $200? DEMAND SCHEDULE Price Quantity Demanded $50.00 $100.00 $150.00 $200.00 P r i c e 200 150 100 50 Quantity From econedlink.org LAW OF DEMAND Let’s take a look at the Netflix Controversy. • What happened to the quantity demanded of Netflix products when the company raised its prices by up to 60 percent? • How does this illustrate the law of demand? From econedlink.org LAW OF DEMAND Rising food prices sour Utah families: • When the price of beef increased, a consumer responded by substituting pork because it was relatively less expensive. Assuming that beef and pork are substitutes, what does this say about the relationship between the demand for a good (like pork) and the price of a substitute (such as beef)? From econedlink.org LAW OF DEMAND • Consider that beef hamburgers and hamburger buns are complements, or goods that go together. If the demand for beef decreases, what will happen to the demand for hamburger buns? • The video mentioned the price of ice cream. Suppose that this price is expected to increase in the future. What will happen to the demand for ice cream in the present? From econedlink.org LAW OF DEMAND The Income Effect • Based on the lesson from the video, would frozen vegetables be considered a normal or inferior good? Why? • The video reported that laptops are normal goods. Are other electronics, like music players, cell phones, and televisions also normal goods? Why? From econedlink.org LAW OF DEMAND The Income Effect • Demand curve shifting: • Shifting the demand curve to the right shows an increase in demand; the quantity demanded is higher at each price level. In the video, an increase in income caused the demand curve to shift to the right for normal goods. • Shifting the demand curve to the left shows a decrease in demand.; the quantity demanded is lower at each price level. In the video, an increase in income caused the demand curve to shift to the left for inferior goods. • Consider how future expectations of income affect demand. For example, if you expect your income to increase in the future, how will this affect your demand for most goods and services in the present? From econedlink.org QUESTION • Do you think your own income would affect your decision to purchase the cheap T-shirts versus the more expensive ones?