Size-Related Aomalies and Stock Return Seasonality

advertisement

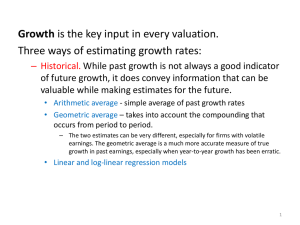

SIZE-RELATED ANOMALIES AND STOCK RETURN SEASONALITY Further Empirical Evidence by Donald B. KEIM Received June 1981, final version received June 1982 Stacey Basallo Rina Bryan Lais Ogata Jenna Yered INTRODUCTION As discussed by last week’s presentation on Banz and Reinganum’s study, there is a significant negative relation between abnormal returns and market value This study looks at the month to month stability of the size anomaly Daily abnormal return distributions in January have large means relative to the remaining months in the year The relationship between abnormal returns and size is always negative and much more defined in January SIZE EFFECT HYPOTHESES Hypotheses that were implied by others to explain the size effect do not seem to explain the January Effect Brown, Kleidon, Marsh argued that the size effect may be explained by an omitted risk factor in the pricing model; would not explain just the January returns Stoll and Whaley – transaction costs DATA AND PORTFOLIO SELECTION CRSP Daily Stock Returns Returns from 1963-1979 (17 years) NYSE and AMEX Listings – firms listed and had returns the entire calendar year Sample size ranges from 1,500 – 2,400 firms throughout the study Beta estimates that adjust for non-synchronous trading DATA AND PORTFOLIO SELECTION CONT. Negative relationship between firm size (market value = # of shares outstanding at YE * YE Price per share of common shares) and abnormal risk adjusted returns (security daily return less equal weighted daily return of the control portfolio) Divide into 10 portfolios; 1 being small firms, 10 being large Re-rank and assess annually Annually firms enter and leave the sample due to bankruptcies, de- listings, mergers, etc. SENSITIVITY OF SIZE ANOMALY TO TRADING INFREQUENCY Roll suggests that the size effect could be due to improperly measured risk Dimson points out a downward bias for small firms (infrequently traded) and an upward bias for large firms (frequently traded) Reinganum acknowledges this, however it is not large enough to explain returns Even when the betas are adjusted for trading frequency, they still show a pronounced negative relationship between small and large portfolios Table 2 shows the average differences between daily CRSP excess returns of small and large portfolios by month SIZE RELATED ANOMALIES AND STOCK RETURN SEASONALITY 50% of the size anomaly occurs in January February, March, July also show higher returns but much lower than January October displays the opposite; size discount All other months are concentrated around 0% abnormal return This seasonality is even more pronounced in the small firms portfolio compared to the large firms portfolio SIZE RELATED ANOMALIES AND STOCK RETURN SEASONALITY Reignanum suggested that the size anomaly was obtained continuously month to month year to year However this report contradicts the month to month stability of the size effect and shows January return premiums occurred every year Average annual size premium of 30.3% declines to 15.4% when the January data is removed FIGURE 2: STOCK RETURN SEASONALITY AND SIZE EFFECT A CLOSER LOOK AT THE JANUARY EFFECT Large portion of the size effect occurs during the first 5 trading days and more specifically the first day The first day’s difference is positive in every year 10.5% of the annual size effect for an average year happens on the first day 26.3% occurs in the first week If we took the average of the size anomaly, only .4% would be expected each day; however the first week of January averages 8% THE JANUARY ANOMALY Even during periods (1969-1973) where large firms had higher returns than small firms, the size premium was still significantly positive in January After accounting for the always positive January effect, the year to year instability of the size anomaly remains Even when the size effect does not hold, January still outperforms other months HYPOTHESES REGARDING THE JANUARY EFFECT Tax Loss Selling Hypotheses – small firms are biased towards inclusion of large price declines in share price and are more likely to experience tax loss selling However, if this hypothesis held, the significance of the January Effect should vary with changes to personal income tax rates One way to test this would be to look at countries with tax codes similar to the United States but with differing tax year ends and see if January still outperforms ALL HYPOTHESES WERE NOT TESTED AND WERE DEFERRED FOR FURTHER RESEARCH HYPOTHESES REGARDING THE JANUARY EFFECT Information Hypotheses – January marks a period of increased uncertainty and anticipation due to the impending release of important information related to company’s prior year performance Approximately 60% of the firms listed on NYSE and AMEX have a fiscal year end date of December 31st To test this hypothesis, you could align all firms’ excess returns in event time (fiscal year end) rather than in calendar time to see if returns increase following the fiscal year end ALL HYPOTHESES WERE NOT TESTED AND WERE DEFERRED FOR FURTHER RESEARCH CONCLUSION Abnormal returns are negatively related to size Daily abnormal returns in January have large means relative to the rest of the year Relationship between size and returns is always negative in January even in years where large firms outperformed small firms No other month had abnormal behavior in this study 50% of the size effect from 1963-1979 is due to January abnormal returns Almost 27% of the premium is due to large abnormal returns in the first week of the trading year Almost 11% is due to the first trading day of the year