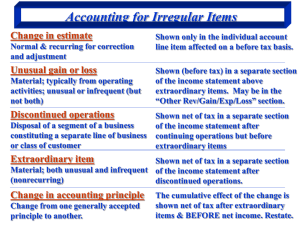

21. In 2003, Teller Co. incurred losses arising from its guilty plea in its first antitrust action, and from a substantial increase in production costs caused when a major supplier's workers went on strike. Which of these losses should be reported as an extraordinary item? a. b. c. d. Antitrust action No No Yes Yes Production costs No Yes No Yes 22. In open market transactions, Gold Corp. simultaneously sold its long-term investment in Iron Corp. bonds and purchased its own outstanding bonds. The broker remitted the net cash from the two transactions. Gold's gain on the purchase of its own bonds exceeded its loss on the sale of the Iron bonds. Gold should report the a. Net effect of the two transactions as an extraordinary gain. b. Net effect of the two transactions in income before extraordinary items. c. Effect of its own bond transaction gain in income before extraordinary items, and report the Iron bond transaction as a loss in income before extraordinary items. d. Effect of its own bond transaction as an extraordinary gain, and report the Iron bond transaction loss in income before extraordinary items. 23. Under SFAS 130, Reporting Comprehensive Income, corrections of errors are reported in a. b. c. d. Other comprehensive income. Other income/(expense). Retained earnings. Stockholders' equity 24. Service Corp. incurred costs associated with relocating employees in a restructuring of its operations. How should the company account for these costs? a. b. c. d. Measured at fair value and recognized over the next two years. Measured at fair value and recognized when the liability is incurred. Recognized when the costs are paid. Measured at fair value and treated as a prior period adjustment. 25. On January 1, 2003, Deer Corp. met the criteria for discontinuance of a business component. For the period January 1 through October 15, 2003, the component had revenues of $500,000 and expenses of S800,000. The assets of the component were sold on October 15, 2003, at a loss for which no tax benefit is available. In its income statement for the year ended December 31, 2003, how should Deer report the component's operations from January 1 to October 15, 2003? a. $500,000 and S800.000 should be included with revenues and expenses, respectively, as part of continuing operations. b. $300,000 should be reported as part of the loss on operations and disposal of a component. c. S300,000 should be reported as an extraordinary loss d. $500,000 should be reported as revenues from operations of a discontinued component. 26. Which of the following criteria is not required for a component's results to be classified as discontinued operations? a. Management must have entered into a sales agreement. b. The component is available for immediate sale. c. The operations and cash flows of the component will be eliminated from the operations of the entity as a result of the disposal. d. The entity will not have any significant continuing involvement in the operations of the component after disposal. 27. On November 1, 2003, management of Herron Corporation committed to a plan to dispose of Timms Company, a major subsidiary. The disposal meets the requirements for classification as discontinued operations. The carrying value of Timms Company was $8,000,000 and management estimated the fair value less costs to sell to be $6,500,000. For 2003, Timms Company had a loss of $2,000,000. How much should Herron Corporation present as loss from discontinued operations before the effect of taxes in its income statement for 2003? a. b. c. d. $0 $1.500,000 $2,000,000 $3,500,000 28. On December 1, 2003, Greer Co. committed to a plan to dispose of its Hart business component's assets. The disposal meets the requirements to be classified as discontinued operations. On that date, Greer estimated that the loss from the disposition of the assets would be $700,000 and Hart's 2003 operating losses were $200,000. Disregarding income taxes, what net gain (loss) should be reported for discontinued operations in Greer's 2003 income statement? a. b. c. d. $0 $(200,000) $ (700,000) $(900,000) 29. A component of Ace, Inc. was discontinued during 2004. Ace's loss on disposal should a. b. c. d. Exclude the associated employee relocation costs. Exclude operating losses for the period. Include associated employee termination costs. Exclude associated lease cancellation costs. 30. When a component of a business has been discontinued during the year, this component's operating losses of the current period should be included in the a. b. c. d. Income statement as part of revenues and expenses. Income statement as part of the loss on disposal of the discontinued component. Income statement as part of the income (loss) from continuing operations. Retained earnings statement as a direct decrease in retained earnings. 21. Extraordinary items are events and transactions that are distinguished by both the unusual nature and infrequency of an occurrence. Teller Co.'s loss arising from its first antitrust action meets both of these criteria and should be reported as an extraordinary item. On the other hand, the strike against Teller Co’s major supplier should not be reported as an extraordinary item because it is usual in nature but may be expected to reoccur as a consequence of continuing business activities. 22. (c) Extraordinary items are material items which are both unusual in nature and infrequency of an occurrence. Therefore, the loss on sale of a bond investment is not extraordinary. In addition, SFAS 145 rescinded SFAS 4 which required gains or losses on extinguishment of debt to be reported as an extraordinary item. Thus, neither item is treated as extraordinary. 23. (c) SFAS 130 does not completely operationalize the concept of comprehensive income per SFAC 5 and 6 which state all transactions and events other than those with owners should be reported in comprehensive income. Under SFAS 130, corrections of errors shall continue to be reported net of tax in retained earnings as an adjustment of the beginning balance. 24. (b) SFAS 146 provides that costs of exit activities (including restructuring charges) should be measured and recognized at fair value when they are incurred. D.2. Discontinued Operations 25. (b) The operating loss of $300,000 ($500,000 revenues less $800,000 expenses) relates to a discontinued component, so it is part of discontinued operations, not continuing operations. It is combined with the loss from disposal on the income statement. Discontinued operations is a category distinct from extraordinary items. 26. (a) SFAS 44 includes a number of requirements for disposal of a component to be presented as discontinued operations. However, management is not required to have entered into a sales agreement. It is sufficient if management is committed to a disposal plan that is reasonable. The other items are all required for presentation as discontinued operations. 27. (d) In discontinued operations, SFAS 144 requires the presentation of the income or loss from operations of the component and the gain or loss on disposal. Since the company met the requirements for “held for sale" status in 2003, the subsidiary should be written down to its fair value less cost to sell. This would result in a loss of $1,500,000 ($8,000,000 carrying amount$6,500,000 fair value). Therefore, the loss from discontinued operations would be $3,500,000 ($2,000,000 loss from operations + $1,500,000 loss on planned disposal). 28. (d) According to SFAS 144, the loss from discontinued operations would equal the loss from operations plus the estimated loss from disposal of the component. 29. (с) benefits, lease termination, and consolidating facilities or relocating employees related to a disposal activity that involves discontinued operations should be included in the results of discontinued operations. SFAS 146 states that costs of termination 30. (b) The requirement is to determine how a discontinued component's operating losses for the current period should be classified in the financial statements. According to SFAS 144, the "income (loss) from operations" is combined with the loss on disposal.