July Market Commentary

advertisement

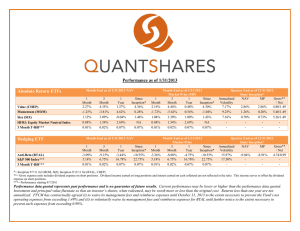

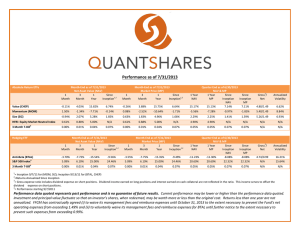

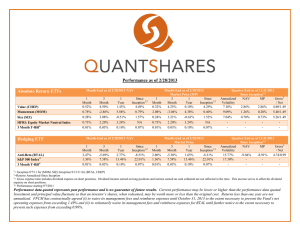

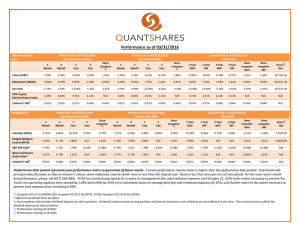

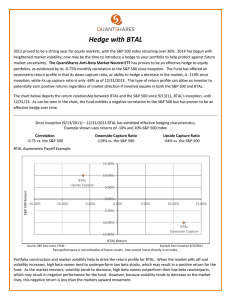

July Market Commentary The equity markets jockeyed for position throughout the month of July. Headlines from Europe and economic data from the US drove the majority of the market moves. Even with intra-month whipsawing, the equity markets finished positive for the month, with the Dow Jones Industrial Average (DJIA) up 1.15%, and the S&P 500 up 1.39%. Consumer Confidence in the US unexpectedly rose in July to 65.9 from an upwardly revised 62.7 in June. The Commerce Department report on personal income showed a slight increase of 0.50 percent in June. The jump in personal income went directly into savings as the savings rate rose to 4.4% in June, as there is still a concerted effort by US consumers to repair their personal balance sheets. Federal Reserve Chairman Bernanke addressed members of Congress this month in Washington. Fed officials identified “two main sources of risk,” Europe and the so-called fiscal cliff here in the US. Chairman Bernanke in his testimony cited, Congressional Budget Office estimates, that if the entirety of the spending cuts and tax increases were to go into effect, the US would be “knocked into a shallow recession” in 2013. He noted the Federal Open Market Committee (FOMC), may take further accommodative action, so far the Fed has refrained from implementing any new programs to prop up a stalling US economy, but may take additional action at their September 12-13 meeting if the July and August jobs reports remain weak. Issues within the Euro zone continue to confound the markets; fears seemingly arise and abate quickly as European leaders continue to work towards a solution for the broad issues that face the region. Strong words from European Central Bank President Mario Draghi sent equity markets higher to end July, as he said he was “prepared to do whatever it takes to preserve the euro.” July QuantShares Commentary Low beta names continued higher in July, as evidenced by QuantShares Market Neutral Anti-Beta Fund (BTAL) finishing the month up 1.22%. Low-beta names have outpaced their high beta peers, for much of the year as the market has struggled to find leadership. QuantShares BTAL has posted strong results over the last 3 and 6 months, up 9.41% and 10.42% respectively. QuantShares BTAL provides a diversified hedge that allows investors to target low-beta names without taking on any additional sector bias (QuantShares BTAL is long the lowest beta names in each sector and short the highest beta names in each sector). Momentum strategies picked up some of the steam they lost in June, as QuantShares Market Neutral Momentum Fund (MOM) posted gains of 3.86% for the month of July. Twelve month price momentum continues to be the top performing factor for calendar year 2012. QuantShares MOM performance has been persistent in 2012, up 10.39% for the year through July, with strong 3 and 6 month returns up 7.25% and 12.61%. QuantShares MOM currently favors lower volatility/higher growth stocks. Small Cap strategies and Value strategies have spent much of 2012 out of favor. After a return to positive territory in June, value and small cap reverted back to underperformance in July as evidenced by the QuantShares Market Neutral Value Fund (CHEP) finishing the month down -0.67% and the QuantShares Market Neutral Size Fund (SIZ) down -1.93%. Performance as of 07/31/2012 Strategic ETFs Month-End as of 07/31/2012 NAV 1-Mo 3-Mo Value (CHEP) Quality (QLT) -0.67% -0.64% Size (SIZ) HFRI: Fund Weighted Composite Index Russell 1000 Index*** 3 Month T-Bill*** Tactical ETFs Month-End as of 07/31/2012 Market Price (MP) 1-Mo 3-Mo -1.61% -2.39% Since Inception* -2.36% -6.22% -0.79% -0.68% -1.93% -2.67% -1.65% 1.05% 1.19% 0.00% -1.24% -1.40% 0.02% NA 19.91% 0.03% -2.26% -3.36% Since Inception* -2.48% -6.26% Annualized Volatility 7.32% 5.92% -1.70% -5.62% -1.70% -5.62% 2.50/.99 2.50/.99 -1.97% -2.87% -1.69% 7.83% 0.28% 0.28% 2.97/.99 1.05% 1.19% 0.00% -1.24% -1.40% 0.02% NA 19.91% 0.03% 19.56% - - - - Month-End as of 07/31/2012 NAV 1-Mo 3-Mo Anti-Beta (BTAL) Momentum (MOM) High Beta (BTAH) Anti-Momentum (NOMO) 1.22% 3.86% -1.91% -4.34% HFRI: Fund Weighted Composite Index Russell 1000 Index*** 3 Month T-Bill*** Quarter End as of 06/30/2012 Since Inception* NAV MP Month-End as of 07/31/2012 Market Price 1-Mo 3-Mo 9.41% 7.25% -11.40% -8.47% Since Inception* -2.03% 8.06% -6.92% -12.44% 1.05% 3.86% -0.80% -4.38% 1.05% 1.19% -1.24% -1.40% NA 19.91% 0.00% 0.02% 0.03% Quarter End as of 06/30/2012 Since Inception* NAV MP Gross**/Net 9.82% 7.71% -10.17% -8.55% Since Inception* -2.11% 8.30% -5.63% -12.52% Annualized Volatility 18.22% 9.21% 17.85% 9.59% Gross**/Net -3.21% 4.04% 5.11% -8.47% -3.13% 4.28% -4.87% -8.52% 1.92/.99 2.79/.99 3.27/.99 2.07/.99 1.05% 1.19% -1.24% -1.40% NA 19.91% 19.56% - - - 0.00% 0.02% 0.03% - - - - *= Inception 9/7/11 for (MOM, NOMO, QLT, SIZ); Inception 9/13/11 for (BTAH, BTAL, CHEP) **= Gross expense ratio includes dividend expense on short positions. Dividend income earned on long positions and interest earned on cash collateral are not reflected in the ratio. This income serves to offset the dividend expense on short positions. ***= Performance starting 9/7/2011 Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Returns less than one year are not annualized. Since the Funds are new, the Operating expenses are based on first year anticipated Assets Under Management growth. FFCM has contractually agreed to waive fees and expenses to limit net expenses from exceeding 0.99% until August 31, 2012. Company Overview: QuantShares designs and manages Market Neutral ETFs to provide exposure to well-known equity factors such as Momentum, Value, Quality, Beta and Size. QuantShares Market Neutral ETFs are the first ETFs that have the capability to short physical stocks (as opposed to derivatives) that passively track indexes. Our ETFs offer investors a diversifying asset that is both highly liquid and fully transparent. The ETFs are designed to generate spread returns, diversify risk and reduce volatility. Value, Size and Quality tend to be more strategic in nature and provide strong risk-adjusted returns; Beta and Momentum are more tactical and allows investors to hedge or express short term investment convictions. QuantShares Market Neutral ETFs provide a liquid alternative to help dampen volatility and enhance the risk return profile of an investment portfolio. Disclosures: Before investing you should carefully consider the Fund’s investment objectives, risks, charges, and expenses. This and other information is in the prospectus, a copy of which can be obtained by visiting the Fund’s website at www.quant-shares.com. Please read the prospectus carefully before you invest. Foreside Fund Service, LLC, Distributor. Shares are not individually redeemable and can be redeemed only in Creation Units. The market price of shares can be at, below or above the NAV. Market Price returns are based upon the midpoint of the bid/ask spread at 4:00PM Eastern time (when NAV is normally determined), and do not represent the returns you would receive if you traded shares at other times. Fund returns assume that dividends and capital gains distributions have been reinvested in the Fund at NAV. Some performance results reflect expense subsidies and waivers in effect during certain periods. Absent these waivers, results would have been less favorable. Risks: There is no guarantee that the funds will reach their objective. An investment in the Funds is subject to risk including the possible loss of principal amount invested. See prospectus for specific risks regarding each Fund. There is a risk that during a “bull” market, when most equity securities and long only ETFs are increasing in value, the Funds’ short positions will likely cause the Fund to underperform the overall U.S. equity market and such ETFs. The Funds may not be suitable for all investors. Short selling could cause unlimited losses, derivatives could result in losses beyond the amount invested, and the value of an investment in the Fund may fall sharply. Beta is a measure of an asset’s sensitivity to an underlying index. Long is purchasing a stock with the expectation that it is going to rise in value. Short is selling stock with the expectation of profiting by buying it back later at a lower price. HFRI Fund Weighted Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to Hedge Fund Research Database. Negative correlation is a relationship between two variables in which one variable increases as the other decreases. Russell 1000 Index measures the performance of approximately 1000 of the largest companies in the U.S. equity market. DJIA – Dow Jones Industrial Average is a price weighted average of 30 significant stocks traded on the NYSE and NASDAQ. S&P 500 is an index of 500 large cap common stocks actively traded on the NYSE and NASDAQ. One cannot invest directly in an index.