BankReconciliation

advertisement

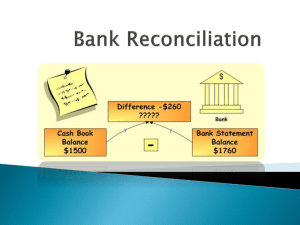

CHAPTER 11 Bank Reconciliation Statement LEARNING OBJECTIVES • Distinguish and explain items appearing in the Bank Statement and Bank account • Explain the need and the purpose of preparing the Bank Reconciliation Statement • Prepare the Bank Reconciliation Statement INTRODUCTION Every month, individuals and businesses maintaining a #Current Account” with a bank will receive a Bank Statement from the bank. Upon receiving the bank statement, the focus is normally on the ending balance besides the transactions on whatever deposits and payments made. The business expects the ending balance appearing in the bank statement is the same as the amount in the Cash Book (bank column).. Thus, the purpose of Bank Reconciliation is to do necessary adjustments to our records in the cash book and come up with the same ending balance as recorded by the bank. It is an analysis explaining the difference between a business’s book balance of cash and its bank statement balance. The Bank Reconciliation Statement must be prepared monthly to justify amounts reported in the Bank Statement and the Bank account kept by the business. BANK STATEMENT Bank Statement is normally debited for payments or charges, and credited for receipts by the business. i. Examples of payments and charges: cheques drawn in favour of creditors or suppliers, bank charges, direct debits and standing order/instructions. ii. Examples of receipts: deposits of cash or cheques, dividend, interest on current account and bank GIRO credits or credit transfer. Sample Bank Statement UITM BANK Shah Alam Statement of Account Account No. 654321 Date Date: 30April 2007 Particulars Debit Credit Balance April 1 Balance b/f 800.50 Cr April 3 Cash deposit 7,000.00 7,800.50 Cr April 4 Transfer from branch 2,500.00 10,300.50 Cr April 6 Cheque book April 8 5.00 10,295.50 Cr 70010 550.00 9,745.50 Cr April 10 70011 700.00 9,045.50Cr April 12 70012 430.00 8,615.50 Cr April 15 Bank GIRO Credit April 20 Direct Debit April 25 Interest April 28 Bank Charges 645.00 574.00 8,686.50 Cr 166.70 10.00 9,260.50 Cr 8,853.20 Cr 8,843.20 Cr CASK BOOK (BANK COLUMN) Cash book or bank account is normally debited with receipts (deposits of cash or cheques) credited with payments (cheques drawn in favour of creditors or suppliers) of the business. Sample Bank account Bank account Balance bId Cash deposit Credit Transfer Intan Brothers 800.50 7,000.00 2,500.00 200.00 ________ 10,500.50 Bank charges -cheque 5.00 book AB Trading – 70010 550.00 Maju Bhd - 700011 700.00 Arif -70012 430.00 Sam-70013 350.00 Balance c/d 8,465.50 10,500.50 Differences between Bank Statement Balance and Bank Account Balance. a) Items recorded in the Bank account but not recorded by the bank: i. Uncredited lodgement or deposits not yet credited. This happens when a business deposits money or cheques but the amount does not appear in the bank statement since the deposits has not yet been processed by the bank; but has already been recorded by the business. Ii. Unpresented cheques. Cheques drawn for payment to creditors or others have not been cashed or banked, i.e., when cheques are drawn for payment and sent to creditors, the record in the business books has been made, but for some reasons the creditor is still carrying the cheque around and have not presented it to the bank for clearance. Differences between Bank Statement Balance and Bank Account Balance. (b) Items recorded in the Bank Statement but not recorded by the business: i. Direct debit. The bank debited the account of the business for payments such as insurance premiums, rates, fees, subscriptions etc. ii. Standing instructions order. This is quite similar to the direct debit in that the bank will debit the account of the business for payments such as insurance premiums, rates, subscriptions, etc. iii. Bank service charge. This is a fee charged by the bank for operating the account for the business andlor issuing the cheque book. iv. Bank GIRO credit or credit transfer. The business account is credited with amount paid by creditor or other organisation direct into the business bank account. v. Interest revenue on current account This interest is credited to the account of the business and is paid by certain bank based on large enough balance of cash in the account. vi. Dishonoured cheques. A cheque, that the bank will not honour upon presentation by the business for clearance. However, the business has already accepted the cheque for the cash book settlement of a debt. Differences between Bank Statement Balance and Bank Account Balance. (c). Errors I. Errors made by the bank - a cheque payment by a debtor had been debited to the business account by the bank, or a bank may make an error in recording the amount to be debited or credited. II. Errors made by the business - error in recording the amount to be debited or credited, or transactions are being debited to the cash book instead of being credited. PREPARATION OF ADJUSTED BANK/CASH BOOK ACCOUNT i. ii. iii. iv. v. Updating the Bank account Matching of entries on the bank statement with those in the bank account. This is done by ticking items that appear both in the bank statement and in the bank account. Items appearing in the bank statement but not in the bank account are transferred to the bank account. There would still be items in the bank account left unticked and they would be treated as either uncredited lodgement (if it is a debit item) or as unpresented cheques (if it is a credit item) and these items would be dealt with in the bank reconciliation statement later on. Any errors relating to the bank account would be dealt with at this stage. Complete the necessary double entry and carry down the balance of the bank account. PREPARATION OF BANK RECONCILIATION STATEMENT b. Preparing the Bank Reconciliation Statement i. Start with balance as per updated bank account balance Bank Reconciliation Statement as at ….. Balance as per updated bank account xx Add: Unpresented cheques xx Less: Uncredited lodgements (xx) Balance as per bank statement xxx ii. Start with balance as per bank statement Bank Reconciliation Statement as at…. Balance as per bank statement xx Add: Uncredited lodgements xx Less: Unpresented cheques (xx) Balance as per updated bank account xxx TREATMENT OF ERRORS, OVERDRAFT AND OPENING BALANCE DISAGREEMENTS The explanation below are meant for bank reconciliation statement that starts with the updated bank account balance: I. Opening balance disagreements: the normal procedure is to account for the opening difference, i.e. by matching and ticking against the entries in the previous period’s bank account. II. Errors made by the bank: if as a result of the error, the bank balance has been understated, for example, if the bank had wrongly debited the bank statement, subtract the amount, The reverse treatment is necessary if the bank had wrongly credited the bank statement and as a result the bank statement balance had been overstated. III.Overdraft for such cases the uncredited lodgement will be added whilst the unpresented cheques subtracted. Example Bank account Balance b/d 8465.50 Direct debit Bank GIRO Credit 645.00 Bank charges Interest 166.70 Balance c/d 9,277.20 574.00 10.00 8,693.20 9,277.20 Bank Reconciliation Statement as at 30 April 2007 Balance as per bank account (updated) 8,693.20 Add: Unpresented cheques 350.00 9,043.20 Less: Uncredited lodgments 200.00 Balance as per bank statement 8,843.20