File

advertisement

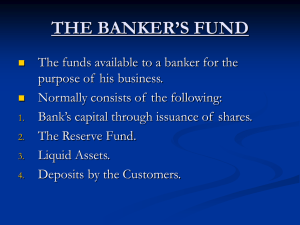

Types of Banker’s Funds & Banker Customer Relationship Learning Objectives Students will be able to: Understand forms of bank capital Know the different types of accounts a bank can offer. Understand how banks maintain relationship with its customers. Comprehend duties & responsibilities of bank and customers Describe termination conditions of bank and customer. Banker’s Funds Bank’s Capital The Reserve Fund Liquid Assets Current Deposits Fixed & Term Deposits Saving Deposits Bank’s Capital Nominal & Authorized Capital Paid Up Capital Subscribed Capital The Reserve Fund Section 21 of the Banking Companies Ordinance, 1962, has made it obligatory for every banking incorporation in Pakistan in Pakistan to create a reserve fund in the following manner: At least 20% of the balance of Profit in each year Liquid Assets According to the section 29(1) of the Banking Companies Ordinance, 1962, every bank in Pakistan is under legal obligation to maintain liquid assets in Pakistan. This amount should be such percentage of the total demand & time liabilities of the bank as may be notified by the State Bank of Pakistan from time to time. Liquid assets are all cash on hand & balances. According to State Bank of Pakistan the liquid asset requirement should be maintain at 15%. Nature of Deposits Fixed & Term Deposits Savings Deposits Current Deposits Current Deposits Current account is a running account which is continuously in operation. Who is interested to open Current account? Wish to have working capital in their custody Interested in keeping their money liquid & safe Like to receive & make payment usually through cheque Utilize the agency services of banks frequently Take full advantage of other services provided by the bank Facilities provided to the current account holder The bank collects properly indorsed cheque, bills etc on behalf of the current account holders. The bank may allow the facility of overdraft on prior arrangements to the trustworthy customers. Loans & advances may be sanctioned to the credit worthy current account holders with ease. A depositor can withdraw sums from the account by means of cheque and ATM cards supplied by the Bank. Current account is opened with a minimum initial deposit as prescribed by the bank from time to time. Fixed & Term Deposits The deposits that can be withdrawn after a specified period of time are referred to a fixed or term deposits. Period for which bank kept money is three months to five years. Payment of Fixed/Term deposits before maturity Law of Limitation Attachment by Court Term Deposits account in Joint Names Saving Deposits Introduced In England In Pakistan Saving Deposit account with very small amount & issued a cheque book. No restrictions on withdrawals Profit & Loss Sharing Account Rules for Profit and Opened by sharing account Opened with initial minimum deposit It may be opened in the name of individual or jointly in the names two or more persons All money to be deposited that should be accompanied by a pay-inslip showing the name and the number of account Withdrawal from the account by cheque Application for cheque book should be made on printed requisition book Bank have right to make investment of credit balances and deposited Profit payable and loss recoverable on PLS The joint account may be operated singly by anyone of them Accountholder wishing to close the account must be present pass book and unused cheque Foreign currency account Salient features Only designated branches authorized to deal Foreign currency can be accepted Deposit can be accepted from residence and non residence Minimum requirements 1000 US dollars Monthly rate of return given It enjoy protection of economic reform act 1992 Foreign currency or Pakistan rupee at the discretion of the depositor Exemption from the account as levy of wealth tax for 6 years, income tax, dedication of zakat Gov. of Pakistan will not make inquiries about there sources Use of Funds The bankers in Pakistan use their funds profitably in the following categories: Short Term loans repayable at short notice Investment in Government & other stock exchange securities Loans & advance to trade, commerce and industry Purchase & Discounting of Bills Financing imports & Exports trade Opening a Bank Account Formal Application Introductory Reference Specimen Signature Opening the Account Closing of the Account Banker-Customer Relationship Meaning of Banker Dealer in Capital Dealer in Money Intermediary party b/w Borrower & Lender According to the Banking ordinance 1962, Banking has been defined as “ Accepting Deposits for the purpose of lending or investment of deposits of money from the public, repayable on demand or otherwise & withdrawals by Cheque, Draft, Order or otherwise.” Meaning of Customer Should have an account with the Bank Deal with the bank in its nature Deal with the bank without consideration of the duration & Frequency of operation of his account A customer is a person who maintains an account with the bank without consideration of the duration & frequency of operation of his account. Relationship Between Banker & Customer General Relationship Special Relationship Principle & Agent Debtor & Creditor Bailer & Bailment Pawner & Pawnee Trustee & Agent Mortgager & Mortgagee Executor, Attorney & Guarantor Rights & Duties of a Customer to Towards Banker Rights a customer Duties of a customer Rights & Duties of a Banker to Towards Customer Duties or obligation of a banker towards customer Rights of banker Termination of Contract Between a Customer & a Banker Termination of relationship by a customer Change of Place Not satisfied with operations Death of Customer Termination of relationship by a Banker If customer Repeatedly present s cheque after the business hours Intimation of the death of a customer Insanity of Customer On receipt of notice of insolvency Company is wound up by the order of the Court Assigns his total credit balance to third party Garnishee order for the whole account Changes in constitution of the Firm Reasons for Dishonoring a Cheque by a Bank A cheque is not in Proper Form When a Banker is Justified in refusing Payments Thanks