Borrowing, Leasing, cont. Social Discount Rate Government BCA

advertisement

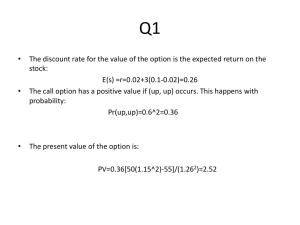

Borrowing, Depreciation, Taxes in Cash Flow Problems H. Scott Matthews 12-706 / 19-702 /73-359 Lecture 5 Admin Issues Who bought Boardman book? Can return. Campbell Textbook due today. First 20 names will be sent TA Office Hours in CEE Lounge (PH 118 hallway near my office) Joe and Paulina will swap coverage next week (i.e, go to office hours in lounge, but look for Joe instead) Notes on Tax deductibility Reason we care about financing and depreciation: they affect taxes owed For personal income taxes, we deduct items like IRA contributions, mortgage interest, etc. Private entities (eg businesses) have similar rules: pay tax on net income Income = Revenues - Expenses There are several types of expenses that we care about Interest expense of borrowing Depreciation (can only do if own the asset) These are also called ‘tax shields’ Goal: Find Cash Flows after taxes Master equation conceptually: CFAT = -equity financed investment + gross income operating expenses + salvage value - taxes + (debt financing receipts - disbursements) + equity financing receipts Where “taxes” = Tax Rate * Taxable Income Taxable Income = Gross Income - Operating Expenses Depreciation - Loan Interest - Bond Dividends After-tax cash flows Dt= Depreciation allowance in t It= Interest accrued in t + on unpaid balance, - overpayment Qt= available for reducing balance in t Wt= taxable income in t; Xt= tax rate Tt= income tax in t Yt= net after-tax cash flow Equations Dt= Depreciation allowance in t It= Interest accrued in t Qt= available for reducing balance in t So At = Qt - It Wt= At-Dt -It (Operating - expenses) Tt= Xt Wt Yt= A*t - Xt Wt (pre tax flow - tax) OR Yt= At + At - Xt (At-Dt -It) Simple example Firm: $500k revenues, $300k expense Depreciation on equipment $20k No financing, and tax rate = 50% Yt= At + At - Xt (At-Dt -It) Yt=($500k-$300k)+0-0.5 ($200k-$20k) Yt= $110k Notes Mixed funds problem - buy computer Below: Operating cash flows At Four financing options in At t 0 1 2 3 4 5 At (Operation) -22,000 6,0 00 6,0 00 6,0 00 6,0 00 6,0 00 2,0 00 10,000 -14,693 At (Fin ancing) 10,000 10,000 -2,5 05 -800 -2,5 05 -800 -2,5 05 -800 -2,5 05 -800 -2,5 05 -10,800 10,000 -2,8 00 -2,6 40 -2,4 80 -2,3 20 -2,1 60 Further Analysis (still no tax) t At 8% (Opera tion ) 0 -22 ,000 1 6,000 2 6,000 3 6,000 4 6,000 5 6,000 2,000 NPV 33 17.4 27 10 ,000 -14 ,693 0.1911 At (Fi nancing at 8%) 10 ,000 10 ,000 -2,505 -80 0 -2,505 -80 0 -2,505 -80 0 -2,505 -80 0 -2,505 -10 ,800 -1.7386 0 10 ,000 -2,800 -2,640 -2,480 -2,320 -2,160 1E-1 2 -12 ,000 6,000 6,000 6,000 6,000 -8,693 2,000 33 17.6 2 A* (To tal pre-ta x) -12 ,000 -12 ,000 3,495 5,200 3,495 5,200 3,495 5,200 3,495 5,200 3,495 -4,800 2,000 2,000 33 15.6 9 33 17.4 MARR (disc rate) equals borrowing rate, so financing plans equivalent. When wholly funded by borrowing, can set MARR to interest rate -12 ,000 3,200 3,360 3,520 3,680 3,840 2,000 33 17.4 3 Effect of other MARRs (e.g. 10%) t At 10 % (Opera tion ) 0 -22 ,000 1 6,000 2 6,000 3 6,000 4 6,000 5 6,000 2,000 NPV 19 86.5 63 10 ,000 -14 ,693 87 6.8 At (Fi nancing at 8%) 10 ,000 10 ,000 -2,505 -80 0 -2,505 -80 0 -2,505 -80 0 -2,505 -80 0 -2,505 -10 ,800 50 4.08 75 8.16 10 ,000 -2,800 -2,640 -2,480 -2,320 -2,160 48 3.69 -12 ,000 6,000 6,000 6,000 6,000 -8,693 2,000 28 63.3 7 A* (To tal pre-ta x) -12 ,000 -12 ,000 3,495 5,200 3,495 5,200 3,495 5,200 3,495 5,200 3,495 -4,800 2,000 2,000 24 90.6 4 27 44.7 ‘Total’ NPV higher than operation alone for all options All preferable to ‘internal funding’ (equity financing) Why? Internal funds could earn 10%, we’re only paying 8% First option ‘gets most of loan’, is best -12 ,000 3,200 3,360 3,520 3,680 3,840 2,000 24 70.2 5 Effect of other MARRs (e.g. 6%) t At 6% (Opera tion ) 0 -22 ,000 1 6,000 2 6,000 3 6,000 4 6,000 5 6,000 2,000 NPV 47 68.6 99 -14 ,693 At (Fi nancing at 8%) 10 ,000 10 ,000 -2,505 -80 0 -2,505 -80 0 -2,505 -80 0 -2,505 -80 0 -2,505 -10 ,800 10 ,000 -2,800 -2,640 -2,480 -2,320 -2,160 -97 9.46 -55 1.97 -52 5.1 10 ,000 -84 2.5 -12 ,000 6,000 6,000 6,000 6,000 -8,693 2,000 37 89.2 3 A* (To tal pre-ta x) -12 ,000 -12 ,000 3,495 5,200 3,495 5,200 3,495 5,200 3,495 5,200 3,495 -4,800 2,000 2,000 42 16.7 3 39 26.2 Now reverse is true Why? Internal funds only earn 6% ! First option now worst -12 ,000 3,200 3,360 3,520 3,680 3,840 2,000 42 43.6 1 First Complex Example Firm will buy $46k equipment Yr 1: Expects pre-tax benefit of $15k Yrs 2-6: $2k less per year ($13k..$5k) Salvage value $4k at end of 6 years No borrowing, tax=50%, MARR=6% Use SOYD and SL depreciation Results - SOYD t At 6% (Pre-ta x) 0 -46,000 1 15,000 2 13,000 3 11,000 4 9,0 00 5 7,0 00 6 5,0 00 4,0 00 NPV 766 1.00 4 SOYD Dt 12,000 10,000 8,0 00 6,0 00 4,0 00 2,0 00 Tax Inco me Wt 3,0 00 3,0 00 3,0 00 3,0 00 3,0 00 3,0 00 Inc Ta x Tt 1,5 00 1,5 00 1,5 00 1,5 00 1,5 00 1,5 00 Aft-Tax Yt -46,000 13,500 11,500 9,5 00 7,5 00 5,5 00 3,5 00 4,0 00 285 .02 D1=(6/21)*$42k = $12,000 SOYD really reduces taxable income! Results - Straight Line Dep. t At 6% (Pre-ta x) 0 -46,000 1 15,000 2 13,000 3 11,000 4 9,0 00 5 7,0 00 6 5,0 00 4,0 00 NPV 766 1.00 4 SL Dt 7,0 00 7,0 00 7,0 00 7,0 00 7,0 00 7,0 00 Tax Inco me Wt 8,0 00 6,0 00 4,0 00 2,0 00 0 -2,0 00 Inc Ta x Tt Aft-Tax Yt -46,000 4,0 00 11,000 3,0 00 10,000 2,0 00 9,0 00 1,0 00 8,0 00 0 7,0 00 -1,0 00 6,0 00 4,0 00 -548 .9 NPV negative - shows effect of depreciation (why lower?) Negative tax? Typically treat as credit not cash back Projects are usually small compared to overall size of company this project would “create tax benefits” Let’s Add in Interest - Computer Again Price $22k, $6k/yr benefits for 5 yrs, $2k salvage after year 5 Borrow $10k of the $22k price Consider single payment at end and uniform yearly repayments Depreciation: Double-declining balance Income tax rate=50% MARR 8% Single Repayment t At At 8% (Operation) (Loa n 8% ) 0 -22,000 10,000 1 6,0 00 2 6,0 00 3 6,0 00 4 6,0 00 5 6,0 00 -14,693 2,0 00 NPV 331 7.42 7 0.1 9109 Bt 22,000 13,200 7,9 20 4,7 52 2,8 51 2,0 00 Dt 8,8 00 5,2 80 3,1 68 1,9 01 851 Rt 100 00 108 00 116 64 125 97 136 05 146 93 It 800 864 933 1,0 08 1,0 88 Wt -3,6 00 -144 1,8 99 3,0 91 4,0 61 Tt -180 0 -72 949 .44 154 5.7 203 0.3 Yt -12,000 7,8 00 6,0 72 5,0 51 4,4 54 -10,723 2,0 00 177 4.38 Had to ‘manually adjust’ Dt in yr. 5 Note loan balance keeps increasing Only additional interest noted in It as interest expense Uniform payments t At At 8% (Operation) (Loa n 8% ) 0 -22,000 10,000 1 6,0 00 -2,5 05 2 6,0 00 -2,5 05 3 6,0 00 -2,5 05 4 6,0 00 -2,5 05 5 6,0 00 -2,5 05 2,0 00 NPV 331 7.42 7 -1.7 386 Bt 22,000 13,200 7,9 20 4,7 52 2,8 51 2,0 00 Dt 8,8 00 5,2 80 3,1 68 1,9 01 851 Rt 100 00 829 5 645 3.6 446 4.9 231 7.1 -2.5 55 It Wt 800 664 516 357 185 -3,6 00 56 2,3 16 3,7 42 4,9 64 Tt -180 0 28.2 115 7.9 187 1 248 1.8 Note loan balance keeps decreasing NPV of this option is lower - should choose previous (single repayment at end).. not a general result Yt -12,000 5,2 95 3,4 67 2,3 37 1,6 24 1,0 13 2,0 00 974 .707 Leasing ‘Make payments to owner’ instead of actually purchasing the asset Since you do not own it, you can not take depreciation expense Lease payments are just a standard expense (i.e., part of the Ct stream) At= Bt - Ct ; Yt= At - At Xt Tradeoff is lower expenses vs. loss of depreciation/interest tax benefits Social Discount Rate Rate used to make investment decisions for society Discounting rooted in consumer preference We tend to prefer current, rather than future, consumption Marginal rate of time preference (MRTP) Face opportunity cost (of foregone interest) when we spend not save Marginal rate of investment return Intergenerational effects We have tended to discuss only short term investment analyses (e.g. 5 yrs) What about effects in distant future? Called intergenerational effects Economists agree that discounting should be done for public projects Do not agree on positive discount rate Discounting handout How much do/should we care about people born after we die? Higher the discount rate, the less future values will count compared to today Ethically, no one’s interests should count more than another’s Implies there is no justification for discounting across long time periods Called ‘equal standing’ Climate Change Discussions ongoing about how best to manage global CO2 emissions to limit effects of global change Should we sacrifice short-run economic growth to do something to improve environment and leave resources for the future? Really asking 2 separate questions! Two Questions What duty do we have to make sacrifices for future generations? If we sacrifice, what is the optimal policy to maximize benefit? So we should compare global change proposals with alternatives Perhaps higher R&D spending on science or medicing would have higher benefits! Hume’s Law Thus discounting issues are normative vs. positive battles Hume noted that facts alone cannot tell us what we should do Any recommendation embodies ethics and judgment E.g. focusing on ‘highest NPV’ implies net benefits is only goal for society Some evidence Cropper et al surveyed 3000 homes Asked about saving lives in the future Found a 4% discount rate for lives 100 years per now Equal standing does not imply different generations have equal claims to present resources! Harsanyi says only do so if their marginal gain is higher than our loss More evidence If future generations will be better off than us anyway Then we might have no reason to make additional sacrifices There might be ‘special standing’ in addition to ‘equal standing’ Immediate relatives vs. distant relatives Different discount rates over time Why do we care so much about future and ignore some present needs (poverty) Based on these arguments, what discount rates should we use for policy problems (eg climate) Government Discount Rates US Government Office of Management and Budget (OMB) Circular A-94 http://www.whitehouse.gov/omb/circulars/a094/a094.html Discusses how to do BCA and related performance studies Match real values with real discount rates, etc How to do sensitivity analysis / which inputs to vary What discount, inflation, etc. rates to use Basically says “use this rate, but do sensitivity analysis with nearby rates” OMB Circular A-94, Appendix C Provides the current suggested values to use for federal government analyses http://www.whitehouse.gov/omb/circulars/a094/a94_appx-c.html Revised yearly, usually “good until January of the next year” How would the government decide its discount rates? What is the government’s MARR? Historic Nominal Interest Rates (from OMB A-94) Real Discount Rates (from A-94) Effect of these Discount Rates These are ‘effectively zero’ What does this mean for projects and project selection decisions? What does it say about intergenerational effects? What are implications of zero or negative discount rates? Next Up: Sensitivity Analysis Skim Clemen Chapter 5 Refers to decision/trees, etc that we have not done yet.