File - Ken Richardson's BAC 131 Website

advertisement

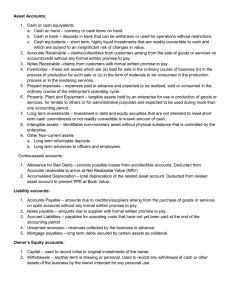

BAC 131 Chapters 7-9 Test Review Notes Chapter 7 Objectives of internal control. Internal controls are designed to safeguard assets from? From an internal control standpoint, what is the asset most susceptible to improper diversion and use? Define and identify examples of establishment of responsibility, segregation of duties, independent internal verification, and rotation of duties. Definition of cash and what is considered cash. What should happen to checks received in the mail? Entry to replenish petty cash. What are debit and credit memorandums? Examples of each. Calculating correct cash balance when given reconciliation information. Why should bank reconciliations be prepared? Define deposits in transit and outstanding checks. How are these handled on bank reconciliations? Define and give examples of cash equivalents. Chapter 8 Difference between accounts receivable and notes receivable. How trade accounts are receivable are valued and reported on the balance sheet? Calculating cash receipts with returns and discounts. Calculating the allowance for doubtful accounts using accounts receivable or sales. The percentage of sales basis of estimating expected uncollectibles emphasizes what? A debit balance in the Allowance for Doubtful Accounts indicates what? Retailers consider Visa and MasterCard sales as what? Calculating interest and maturity value on notes receivable. Calculate the average collection period for accounts receivable in days. Chapter 9 Calculating cost of fixed asset acquisition under the cost principle. When is interest included in the acquisition cost of a plant asset? The balance in the Accumulated Depreciation account represents? What is depreciation? How is the book value of an asset calculated? Which principle requires depreciation to be recorded? Calculating depreciation using the straight-line, units of production, and double-declining balance methods. How does the double-declining balance method work? What does it ignore that other methods do not? Which depreciation method is most used by business today? Calculation of gain or loss on fixed asset disposal. If a company incurs legal costs in successfully defending its patent, how are these costs recorded? How are research and development costs recorded? Ordinary repairs are considered to be what kind of expenditure? Problems: Prepare a bank reconciliation with adjusting journal entries (Chapter 7). Prepare entries related to a petty cash fund (Chapter 7). Record the adjusting entries to record bad debt expense using sales and accounts receivable estimates (Chapter 8) Record two years of depreciation expense using the straight-line, units-of-production, and double declining balance methods (Chapter 9).