Minnesota-110111 - Insurance Information Institute

advertisement

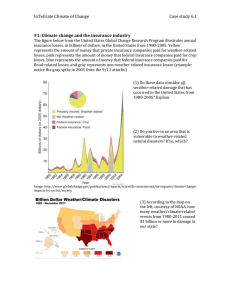

Homeowners Insurance: Is a Minnesota Meltdown Coming? Insurance Federation of Minnesota Minneapolis, MN November 1, 2011 Download at www.iii.org/presentations Robert P. Hartwig, Ph.D., CPCU, President & Economist Insurance Information Institute 110 William Street New York, NY 10038 Tel: 212.346.5520 Cell: 917.453.1885 bobh@iii.org www.iii.org What in the World Is Going On? Is the World (Including Minnesota) Becoming a Riskier Place? What Are the Implications for the Insurance Industry and Policyholders? 2 Uncertainty, Risk and Fear Abound ECONOMIC & POLITICAL CONCERNS Global Economic Slowdown European Sovereign Debt, Bank & Currency Crises US Debt and Budget Crisis and S&P Downgrade Echoes of the Financial Crisis Housing Crisis Persistently High Unemployment Inflation/Deflation Runaway Energy & Commodity Prices Political Upheaval in the Middle East 2012 US Elections CATASTROPHIC LOSS Japan, New Zealand, Turkey, Haiti, Chile Earthquakes Nuclear Fears US: Tornadoes, Flooding, Wildfires, Hurricanes, Winter Storms Manmade Disasters (e.g., Deepwater Horizon) Cyber Attacks Resurgent Terrorism Risk (e.g., Bin Laden, Gadhafi Killings) Are “Black Swans” everywhere or does it just seem that way? 3 Minnesota’s Homeowners Insurance Market Profitability and Growth in MN vs. Other Lines and States 4 Return of Net Worth, All Lines: MN vs. U.S., 2000-2009* (Percent) MN profitability is about average since 2000 but has lagged in recent years 20% 15% 10% 5% Average 2000-2009 0% US: 7.0% -5% MN: 6.8% -10% 00 01 02 US All Lines *Latest available. Sources: NAIC; Insurance Information Institute. 03 04 05 06 07 08 09 MN All Lines 5 Return on Net Worth, Homeowners: MN vs. U.S., 2000-2009* (Percent) Average 2000-2009 US: 4.7% 60% MN: -14.4% 40% 20% 0% MN profitability in the Homeowners line—at 14.4% on avg. since 2000, is far worse than the US average and is more like that of a coastal, hurricane-exposed state -20% -40% -60% -80% 00 01 02 US HO *Latest available. Sources: NAIC; Insurance Information Institute. 03 04 05 06 07 08 09 MN HO 6 Return on Net Worth, Pvt. Passenger Auto: MN vs. U.S., 2000-2009 MN profitability in the private passenger auto is above the US average, but in this era of direct auto-only marketers selling home as a loss leader won’t work 25% 20% 15% 10% Average 2000-2009 US: 7.2% 5% MN: 11.3% 0% 00 01 02 US PP Auto *Latest available. Sources: NAIC; Insurance Information Institute. 03 04 05 06 07 08 09 MN PP Auto 7 All Lines: 10-Year Average RNW MN & Nearby States 2000-2009 10.4% 8.2% Indiana 8.0% Wisconsin 7.6% 7.0% 6.8% 6.3% South Dakota North Dakota Minnesota All Lines profitability is below the US and regional average U.S. Minnesota Illinois 0% 2% 4% 6% Source: NAIC, Insurance Information Institute 8% 10% 12% Homeowners: 10-Year Average RNW MN & Nearby States 2000-2009 4.7% Minnesota Homeowners profitability is below the US average and the regional average U.S. 2.2% South Dakota 1.6% Illinois 0.4% Wisconsin -5.5% Indiana -10.8% North Dakota -14.4% Minnesota -20% -15% -10% -5% Source: NAIC, Insurance Information Institute 0% 5% 10% 715 721 749 788 788 789 791 814 842 845 845 856 862 897 911 926 980 980 1,026 916 808 800 MN ranks as the 14th most expensive state for homeowners insurance 983 1,000 1,048 1,200 1,155 1,400 1,390 1,600 1,460 Homeowners Average Expenditure by State, 2008: Highest 25 States 600 400 200 0 TX FL LA OK MA NY CT MS DC KS CA RI HI AK AL MN CO NE ND US SC AR MO GA MT MI Note: Average premium=Premiums/exposure per house years. A house year is equal to 365 days of insured coverage for a single dwelling. The NAIC does not rank State Average Expenditures and does not endorse any conclusions drawn from this data. Source: © 2010 National Association of Insurance Commissioners (NAIC). Reprinted with permission. Further reprint or distribution strictly prohibited without written permission of NAIC. 11 Homeowners Average Expenditure by State, 2008: Lowest 25 States 432 471 439 387 400 565 572 601 609 586 535 503 500 604 600 612 628 628 637 638 647 650 658 676 683 691 692 692 700 703 800 300 200 100 0 NM NV TN NJ NC WY IN VT NH WV MD AZ IL IA SD VA KY PA ME OH DE WI WA OR UT ID Note: Average premium=Premiums/exposure per house years. A house year is equal to 365 days of insured coverage for a single dwelling. The NAIC does not rank State Average Expenditures and does not endorse any conclusions drawn from this data. Source: © 2010 National Association of Insurance Commissioners (NAIC). Reprinted with permission. Further reprint or distribution strictly prohibited without written permission of NAIC. 12 MN Homeowners Average Expenditure, 1998-2008* $900 $800 The average expenditure on homeowners insurance in MN was $54 or 6.8% above the US avg. of $791 in 2008, 14thh highest in the country. $845 Avg. expenditure climbed 125% between 1998 and 2008. $767 $790 $788 $800 2005 2006 2007 $733 $700 $590 $600 $500 $400 $464 $375 $390 1998 1999 $420 $300 2000 2001 2002 2003 2004 2008 *Latest available. Note: Average premium=Premiums/exposure per house years. A house year is equal to 365 days of insured coverage for a single dwelling. The NAIC does not rank State Average Expenditures and does not endorse any conclusions drawn from this data. Source: © 2010 National Association of Insurance Commissioners (NAIC). Reprinted with permission. Further reprint or distribution strictly prohibited without written permission of NAIC. 13 PP Auto: 10-Year Average RNW MN & Nearby States 2000-2009 11.6% South Dakota 11.3% Minnesota 10.3% North Dakota 8.9% 8.7% 7.6% Wisconsin Minnesota PP Auto profitability is above the US and regional average 7.2% Indiana Illinois U.S. 0% 5% Source: NAIC, Insurance Information Institute 10% 15% All Lines DWP Growth: MN vs. U.S., 2001-2010 All Lines Direct Written Premium (DPW) growth in MN is little different from the US overall since over the past decade 1.5% -2.1% -0.3% -5% 0.5% 2.1% 3.4% -0.4% 0% 2.2% 3.9% 5% 0.0% -0.1% MN: 4.2% -3.3% -3.9% US: 4.4% 7.4% 10% Average 2001-2010 9.8% 11.4% 15% 12.0% 12.2% 20% 14.3% 15.4% (Percent) -10% 01 Source: SNL Financial. 02 03 US DWP: All Lines 04 05 06 07 08 MN DWP: All Lines 09 10 16 Personal Lines DWP Growth: MN vs. U.S., 2001-2010 (Percent) 2.5% 3.4% 09 10 -0.4% -5% -1.9% -1.2% 0% -0.1% 0.4% 1.2% 2.3% 5.4% 2.6% 5% 2.3% MN: 3.9% 1.1% 3.1% US: 4.3% 9.2% 9.8% 11.1% 13.5% 8.2% 9.4% 15% 10% Personal Lines DPW growth has been slower, on average, in MN relative to the US overall Average 2001-2010 20% -10% 01 02 03 04 US DWP: Personal Lines Source: SNL Financial. 05 06 07 08 MN DWP: Personal Lines 17 Homeowner’s MP DWP Growth: MN vs. U.S., 2001-2010 (Percent) Average 2001-2010 25.2% US: 9.7% 8.9% 3.9% 4.2% 3.5% 5% 0.8% 7.4% 3.0% 7.3% 13.5% 11.1% 8.1% 10% 8.3% 15% 14.4% 13.9% 20% 4.9% 7.7% Homeowners DPW growth has generally been higher in MN compared to the US overall MN: 7.6% 5.2% 20.5% 25% 0.5% 30% 0% 01 Source: SNL Financial. 02 03 04 US DWP: HO Lines 05 06 07 08 09 MN DWP: HO Lines 10 18 Private Passenger Auto DWP Growth: MN vs. U.S., 2001-2010 (Percent) Average 2001-2010 PP Auto DPW growth from 2001-2010 in MN was half the US average MN: 1.6% 01 Source: SNL Financial. 02 03 US DWP: PP Auto 04 05 -0.1% 0.3% 06 07 MN DWP: PP Auto -0.4% -1.9% -5% -3.2% -3.0% 0% -2.2% 0.0% 0.5% 0.6% 0.6% 3.6% 5% 1.5% 1.0% 10.2% 10.2% US: 3.2% 7.9% 6.3% 10% 8.2% 8.2% 15% 08 09 10 19 Minnesota’s Catastrophe Loss History It May Not Be a Coastal State, but MN is No Stranger to Catastrophe 22 Severe Weather Reports in Minnesota, January 1—October 25, 2011 There were 552 severe weather reports in MN through Oct. 25 MN Total Reports = 552 Tornadoes = 30 (Red) Hail Reports = 192 (Green) Wind Reports = 330 (Blue) Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2011_annual_summary.html# 23 States With Highest Insured Catastrophe Losses, 2007 ($ millions) State Estimated insured loss (1) California Minnesota Texas Georgia Illinois Oklahoma Kansas Missouri New York Colorado Alabama $1,427 747 677 320 272 270 262 223 202 200 200 (1) Does not include flood damage covered by the federally administered National Flood Insurance Program. Note: Catastrophes are assigned serial numbers by the Property Claim Services (PCS) unit of ISO when the insured loss to the industry resulting from an occurrence reaches at least $25 million and affects a significant number of policyholders and insurers. Source: ISO’s Property Claims Services (PCS) unit. 24 Top Ten States By Highest Insured Catastrophe Losses, 2008 ($ millions) Rank 1 2 3 4 5 6 7 8 9 10 State Estimated insured loss Texas Louisiana Minnesota Ohio Georgia Arkansas Indiana Kentucky Illinois Kansas $11,669.0 2,228.0 1,583.0 1,459.0 1,040.0 786.5 785.0 743.0 640.0 638.0 Note: Catastrophes are assigned serial numbers by the Property Claim Services (PCS) unit of ISO when the insured loss to the industry resulting from an occurrence reaches at least $25 million and affects a significant number of policyholders and insurers. Source: ISO's Property Claims Services (PCS) unit. 25 MN & U.S. Homeowners Loss Ratio, 2001-2010 40 157.3 75.3 60.6 71.0 50.4 53 59.3 127.9 83.7 47.8 34.6 60 59.2 80 74.8 65.9 100 77.2 120 76.5 75.6 140 31.8 143.2 160 66.4 Minnesota had some very bad years in the home insurance line, with loss ratios well over 100% 180 20 0 01 Source: SNL Financial. 02 03 MN 04 05 06 07 U.S. 08 09 10 26 158.4 Homeowners Insurance Combined Ratio: 1990–2011P 170 160 115.0 106.7 105.7 116.8 95.6 100.3 109.3 94.4 88.9 90 98.2 100 121.7 111.4 108.2 109.4 118.4 112.7 101.0 110 113.6 120 117.7 130 113.0 140 121.7 150 80 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11P Homeowners Line Could Deteriorate in 2011 Due to Large Cat Losses. Extreme Regional Variation Can Be Expected Due to Local Catastrophe Loss Activity Sources: A.M. Best (1990-2010); Insurance Information Institute (2011P). Number of Federal Disaster Declarations In Minnesota, 1953-2011* 2 3 3 4 2 2 2.0 2 2.5 2 3.0 2 3.5 3 federal disaster declarations were made through Oct. 31 in MN for severe storms, tornadoes and flooding between May and July. 2 4.0 There have been 48 federal disaster declarations in MN since 1953. The average number of declarations per year is 0.8 from 19532011, though the number has been higher in recent years 2 2 4.5 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1 1.0 1 1.5 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 0 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11* 0.0 0 0 0 0 0.5 The Number of Federal Disaster Declarations Spike in 2010 and 2011 with Three Events Each Year, Second Only to 1997 *Through October 31, 2011. Source: Federal Emergency Management Administration: http://www.fema.gov/news/disaster_totals_annual.fema ; Insurance Information Institute. Average Number of Tornadoes per Year, 2000-2010 Minnesota averaged 51 tornadoes per year from 2000-2010, but experiences only 30 in 2011 through Oct. 25 Source: NOAA at http://www.spc.noaa.gov/wcm/ustormaps/2001-2010-states.png 29 Tornado by County, 1952-2010 MN is on the northern edge of tornado alley Source: NOAA at http://www.spc.noaa.gov/wcm/ustormaps/tornadoes-by-county.png 30 Tornado Tracks by EF Scale, 1950-2010 Minnesota has experiences every strength of tornado, including EF-5 storms Source: NOAA at: http://www.spc.noaa.gov/gis/svrgis/images/EF_tracks.gif 31 2010 Tornado and Severe Thunderstorm Watches & Departure from Average MN tornado activity was well above average in 2010 Source: NOAA at http://www.spc.noaa.gov/wcm/2010-wbc-anoms.png 32 U.S. Insured Catastrophe Loss Update 2011 CAT Losses Already Greatly Exceed All of 2010 and Will Become One of the Most Expensive Years on Record 33 US Insured Catastrophe Losses ($ Billions) $120 $100 $80 Record Tornado Losses Caused 2011 CAT Losses to Surge $61.9 2000s: A Decade of Disaster 2000s: $193B (up 117%) 1990s: $89B $100.0 $100 Billion CAT Year is Coming Eventually $24.0 $13.6 $10.6 $6.7 $9.2 $27.1 $27.5 $12.9 $5.9 $26.5 $4.6 $8.3 $10.1 $2.6 $7.4 $8.3 $16.9 $4.7 $2.7 $20 $7.5 $40 $5.5 $22.9 $60 $0 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11*20?? First Half 2011 US CAT Losses Already Exceed Losses from All of 2010. Even Modest Hurricane Losses Will Make 2011 Among the Most Expensive Ever for CATs *Estimate through Sept. 30, 2011. Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01. Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B. Sources: Property Claims Service/ISO; Insurance Information Institute. 34 Top 12 (13?) Most Costly Disasters in U.S. History (Insured Losses, 2010 Dollars, $ Billions) $50 $45 $40 $35 $30 $25 $20 $15 $10 $5 $0 Taken as a single event, the Spring 2011 tornado season would likely become 5th costliest event in US insurance history $45.8 $22.6 $23.1 $17.5 $6.3 $6.7 Jeanne Frances Rita (2004) (2004) (2005) Hugo (1989) $4.3 $5.3 $8.2 $8.6 Ivan (2004) Charley (2004) $14.0 $11.5 $12.8 Wilma (2005) Ike Spring Northridge Andrew 9/11 Attack Katrina (2008) Tornadoes* (1994) (1992) (2001) (2005) (2011) *Losses will actually be broken down into several “events” as determined by PCS. Sources: PCS; Insurance Information Institute inflation adjustments. 35 Combined Ratio Points Associated with Catastrophe Losses: 1960 – 2011:H1* 5.0 2.6 3.3 2010E 2008 1.6 2.7 2006 1.6 2002 2004 1.6 2000 1998 1.0 1996 3.3 3.3 3.6 2.9 3.3 2.8 1994 5.0 5.4 5.9 8.1 8.8 1990 2.1 2.3 3.0 1.2 1988 1986 1984 1982 1980 1978 1976 1974 1972 1970 1968 1.2 0.4 0.8 1.3 0.3 0.4 0.7 1.5 1.0 0.4 0.4 0.7 1.8 1.1 0.6 1.4 2.0 1.3 2.0 0.5 0.5 0.7 0.4 1966 1962 1964 3.6 1960s: 1.04 1970s: 0.85 1980s: 1.31 1990s: 3.39 2000s: 3.52 2010s: 4.15* 0.8 1.1 1.1 0.1 0.9 1960 10 9 8 7 6 5 4 3 2 1 0 Avg. CAT Loss Component of the Combined Ratio by Decade 1992 Combined Ratio Points The Catastrophe Loss Component of Private Insurer Losses Has Increased Sharply in Recent Decades *Insurance Information Institute estimates for 2010 and 2011:H1 Notes: Private carrier losses only. Excludes loss adjustment expenses and reinsurance reinstatement premiums. Figures are adjusted for losses ultimately paid by foreign insurers and reinsurers. Source: ISO; Insurance Information Institute. 36 Natural Disasters in the United States, 1980 – 2011* Number of Events (Annual Totals 1980 – 2010 and First Half 2011) 300 There were 98 natural disaster events in the first half of 2011 250 Number 200 150 100 37 8 50 51 2 1980 1982 1984 1986 1988 Geophysical (earthquake, tsunami, volcanic activity) *Through June 30. Source: MR NatCatSERVICE 1990 1992 1994 1996 1998 Meteorological (storm) Hydrological (flood, mass movement) 2000 2002 2004 2006 2008 2010 Climatological (temperature extremes, drought, wildfire) 37 U.S. Thunderstorm Loss Trends, 1980 – 2011* Thunderstorm losses in the first half of 2011 totaled $16.4 billion, a new annual record through just 6 months Average thunderstorm losses are up more than 8 fold since the early 1980s *Through June 30, 2011. Source: Property Claims Service, MR NatCatSERVICE Hurricanes get all the headlines, but thunderstorms are consistent producers of large scale loss. 2008-2011 are the most expensive years on record. 38 U.S. Winter Storm Loss Trends, 1980 – 2010 (Annual Totals) vs. First Half 2011 Insured winter storm losses in 2011 totaled $1.4 billion and are up 50% since 1980. Source: Property Claims Service, MR NatCatSERVICE 39 U.S. Acreage Burned by Wildfires, 1980 – 2010 (Annual Totals) vs. First Half 2011 2011 could be a severe year for wildfire damage. Acres burned through June 30 already exceed all of 2010. Source: National Forest Service, MR NatCatSERVICE 40 Inflation Adjusted U.S. Catastrophe Losses by Cause of Loss, 1990–2011:H11 Wind/Hail/Flood (3), $12.7 Fires (4), $9.0 Other (5), $0.6 Geological Events, $18.5 2.4% 4.9% 3.4%0.2% Terrorism, $24.9 6.6% 42.7% Winter Storms, $30.0 8.0% Hurricanes & Tropical Storms, $160.5 Tornado share of CAT losses is rising 31.8% Tornadoes (2), $119.5 Wind losses are by far cause the most catastrophe losses, even if hurricanes/TS are excluded. 1. Catastrophes are defined as events causing direct insured losses to property of $25 million or more in 2009 dollars. 2. Excludes snow. 3. Does not include NFIP flood losses 4. Includes wildland fires 5. Includes civil disorders, water damage, utility disruptions and non-property losses such as those covered by workers compensation. Source: ISO’s Property Claim Services Unit. 41 Number of Federal Disaster Declarations, 1953-2011* 0 90 81 75 59 48 52 45 45 49 50 56 63 65 69 75 44 32 36 32 43 45 38 11 31 34 24 21 15 29 17 17 19 11 11 12 12 7 7 10 53 54 55 56 57 58 59 60 61 62 63 64 65 66 67 68 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11* 20 13 17 18 16 16 30 22 20 25 25 40 27 28 23 38 50 42 60 23 70 22 25 80 30 90 48 46 46 100 The number of federal disaster declarations set a new record in 2011, with 86 declarations through Sept. 30. It is no wonder that FEMA is broke! There have been 2,036 federal disaster declarations since 1953. The average number of declarations per year is 34 from 1953-2010, though that few haven’t been recorded since 1995. The Number of Federal Disaster Declarations Is Rising and Set a New Record in 2011 *Through October 31, 2011. Source: Federal Emergency Management Administration: http://www.fema.gov/news/disaster_totals_annual.fema ; Insurance Information Institute. Federal Disasters Declarations by State, 1953 – Oct. 31, 2011: Highest 25 States Over the past nearly 60 years, Texas has had the highest number of Federal Disaster Declarations 30 20 10 39 42 43 44 45 46 47 47 47 48 48 50 51 53 53 55 55 63 MN has had 48 federal disaster declarations since 1953, less than one per year, on average (1 declaration about every 1.2 years) 40 40 50 50 58 60 65 70 70 Disaster Declarations 80 78 90 86 100 0 TX CA OK NY FL LA AL KY AR MO IL MS TN IA MN KS NE PA WV OH WA VA ND NC IN Source: FEMA: http://www.fema.gov/news/disaster_totals_annual.fema; Insurance Information Institute. 43 Federal Disasters Declarations by State, 1953 – Oct. 31, 2011: Lowest 25 States* Over the past nearly 60 years, Wyoming, Utah and Rhode Island had the fewest number of Federal Disaster Declarations 9 9 10 9 10 14 15 16 16 17 23 23 25 25 26 27 26 24 22 20 20 27 30 32 32 35 35 39 36 Disaster Declarations 40 39 50 0 ME SD GA AK WI VT NJ NH OR MA PR HI MI AZ ID NM MD MT NV CO CT SC DE DC RI UT WY *Includes Puerto Rico and the District of Columbia. Source: FEMA: http://www.fema.gov/news/disaster_totals_annual.fema; Insurance Information Institute. 44 SPRING 2011 TORNADO & SEVERE STORM OUTBREAK 2011 Will Be Among the Most Deadly and Expensive for Tornadoes In History 45 Number of Tornadoes and Related Deaths, 1990 – 2011* 800 600 1,805 1,282 1,098 1,103 1,376 1,216 1,148 1,173 1,234 1,082 1,297 1,173 1,071 941 1,000 1,132 1,200 1,133 1,400 546 There were 1,805 tornadoes recorded in the US by Oct. 13 400 600 500 400 300 200 Number of Deaths Number of Tornadoes 1,600 1,345 1,424 Number of Deaths 1,800 1,692 1,819 1,156 Number of Tornadoes 1,264 2,000 Tornadoes have already claimed more than 500 lives 100 200 0 0 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11P Insurers Expect to Pay at Least $2 Billion Each for the April 2011 Tornadoes in Alabama and a Similar Amount for the May Storms in Joplin *2011 is preliminary data through October 13. Source: U.S. Department of Commerce, Storm Prediction Center, National Weather Service. 46 U.S. Tornado Count, 2005-2011* There were 1,819 tornadoes in the US in 2011 through Oct. 29, far above average, but well below 2008’srecord Deadly and costly April/ May spike Source: http://www.spc.noaa.gov/wcm/ *Through October 29. 47 Insurers Making a Difference in Impacted Communities Destroyed home in Tuscaloosa. Insurers will pay some 165,000 claims totaling $2 billion in the Tuscaloosa/ Birmingham areas alone. Presentation of a check to Tuscaloosa Mayor Walt Maddox to the Tuscaloosa Storm Recovery Fund Source: Insurance Information Institute 48 Location of Tornadoes in the US, January 1—October 13, 2011 1,805 tornadoes killed 546 people through Oct. 13, including at least 340 on April 26 mostly in the Tuscaloosa area, and 130 in Joplin on May 22 Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2011_annual_summary.html# 49 Location of Large Hail Reports in the US, January 1—October 13, 2011 There were 9,287 “Large Hail” reports through Oct. 13, causing extensive damage to homes, businesses and vehicles Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2011_annual_summary.html# 50 Location of Wind Damage Reports in the US, January 1—Oct. 13, 2011 There were 18,293 “Wind Damage” reports through Oct. 13, causing extensive damage to homes and, businesses Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2011_annual_summary.html# 51 Severe Weather Reports, January 1—October 13, 2011 There have been 29,385 severe weather reports through Oct. 13; including 1,805 tornadoes; 9,287 “Large Hail” reports and 18,293 high wind events Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2011_annual_summary.html# 52 Number of Severe Weather Reports in US, by Type: January 1—October 13, 2011 Tornadoes, 1,805 , 6% Large Hail, 9,287 , 32% Wind Damage, 18,293 , 62% Tornadoes accounted for just 6% of all Severe Weather Reports through October 13 but more than 500 deaths Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2011_annual_summary.html# Global Catastrophe Loss Developments and Trends 2011 and 2010 Are Rewriting Catastrophe Loss and Insurance History 54 Global Catastrophe Loss Summary: First Half 2011 2011 Is Already (as of June 30) the Highest Loss Year on Record Globally Extraordinary accumulation of severe natural catastrophe: Earthquakes, tsunami, floods and tornadoes are the primary causes of loss $260 Billion in Economic Losses Globally New record for the first six months, exceeding the previous record of $220B in 2005 Economy is more resilient than most pundits presume $55 Billion in Insured Losses Globally More than double the first half 2010 amount Over 4 times the 10-year average $27 Billion in Economic Losses in the US Represents a 129% increase over the $11.8 billion amount through the first half of 2010 $17.3 Billion in Insured Losses in the US Arising from 100 CAT Events Represents a 162% increase over the $6.6 billion amount through the first half of 2010 55 Natural Loss Events, January – September 2011 World Map Source: MR NatCatSERVICE 56 Worldwide Natural Disasters 2011 % Distribution of Insured Losses Per Continent (January – June only) Insured losses 2011 (January – June only): US$ 60bn 49% <1% 29% <1% <1% Continent Africa America Asia Australia/Oce ania Europe Source: MR NatCatSERVICE Insured losses [US$ m] in 2011 Jan - June minor 17,800 30,080 21% 12,900 100 58 US Second Quarter Insured Catastrophe Losses, 2000–2011 $ Billions $16 $14 $12 2011:Q2 CAT losses totaled $15.09 billion and are the highest on record Q2 CAT losses from 2000-2010 average $4.0 billion. 2011:Q2 CAT losses were nearly 4 times that amount at $15.09 billion $15.09 $10 $7.11 $8 $6 $5.05 $4 $2 $6.38 $6.24 $2.79 $5.04 $2.33 $1.46 $4.47 $2.30 $0.93 $0 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 Record Q2 (and First Half) CAT Losses Will Adversely Impact Insurer Results in 2011 Sources: ISO/PCS; Insurance Information Institute. 60 Top 16 Most Costly World Insurance Losses, 1970-2011* (Insured Losses, 2010 Dollars, $ Billions) $80 $70 $60 $50 $40 $30 $20 $10 Taken as a single event, the Spring 2011 tornado and thunderstorm season would likely become the 7th costliest event in global insurance history $11.3 $14.0 $10.0 $9.3 $9.0 $7.8 $8.0 $8.0 3 of the top 15 most expensive catastrophes in world history have occurred in the past 18 months $14.9 $16.3 $72.3 $35.0 $20.5 $20.8 $23.1 $24.9 $0 Winter Storm Daria (1991) Chile Hugo Typhoon Charley New Rita Quake (1989) Mirielle (2004) Zealand (2005) (2010) (1991) Quake (2011) Wilma (2005) Ivan Spring Ike Northridge WTC TerrorAndrew Japan Katrina (2004) Tornadoes/ (2008) (1994) Attack (1992) Quake, (2005) Storms (2001) Tsunami (2011) (2011)* *Through June 20, 2011. 2011 disaster figures are estimates; Figures include federally insured flood losses, where applicable. Sources: Swiss Re sigma 1/2011; AIR Worldwide, RMS, Eqecat; Insurance Information Institute. 62 Worldwide Natural Disasters, 1980 – 2011* Number of Events There were 355 events through the first 6 months of 2011 600 500 400 300 200 100 1980 1982 1984 1986 Geophysical events (Earthquake, tsunami, volcanic eruption) *2011 figure is through June 30. Source: MR NatCatSERVICE 1988 1990 1992 1994 Meteorological events (Storm) 1996 1998 2000 2002 Hydrological events (Flood, mass movement) 2004 2006 2008 2010 Climatological events (Extreme temperature, drought, forest fire) 63 Global Property Catastrophe Rate on Line Index, 1990-2011 YTD (6/1/11) A modest increase in global property catastrophe reinsurance pricing was evident in June 1 renewals in the wake of record global catastrophe losses. Larger increase could occur for the Jan.1, 2012 renewals Source: Guy Carpenter, GC Capital Ideas.com, September 26, 2011. P/C Insurance Industry Financial Overview Profit Recovery Will Be Set Back by High CATs, Low Interest Rates, Diminishing Reserve Releases 66 $3,043 $4,758 $28,672 $34,670 $65,777 $44,155 $38,501 $30,029 $20,559 $20,598 $10,870 $3,046 $10,000 $19,316 $20,000 $5,840 $30,000 $14,178 $40,000 $21,865 $50,000 $30,773 $60,000 2005 ROE*= 9.6% 2006 ROE = 12.7% 2007 ROE = 10.9% 2008 ROE = 0.3% 2009 ROAS1 = 5.9% 2010 ROAS = 6.5% 2011:H1 ROAS = 1.7% P-C Industry 2011:H1 profits were down 71.6% to $4.8B vs. 2010:H1, due to high catastrophe losses and as non-cat underwriting results deteriorated $36,819 $70,000 $24,404 $80,000 $62,496 P/C Net Income After Taxes 1991–2011:H1 ($ Millions) $0 -$10,000 -$6,970 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 * ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 2.3% ROAS for 2011:H1, 7.5% for 2010 and 7.4% for 2009. Sources: A.M. Best, ISO, Insurance Information Institute 10 11* A 100 Combined Ratio Isn’t What It Once Was: Investment Impact on ROEs A combined ratio of about 100 generated ~7.5% ROE in 2009/10, 10% in 2005 and 16% in 1979 Combined Ratio / ROE 15.9% 110 109.4 14.3% 100.6 100 15% 12.7% 105 100.1 97.5 95 101.0 100.7 9.6% 99.3 7.4% 92.6 8.9% 18% 100.8 12% 9% 7.5% 6% 90 2.3% 4.4% 85 3% 0% 80 1978 1979 2003 2005 2006 Combined Ratio 2008* 2009* 2010* 2011:H1* ROE* Combined Ratios Must Be Lower in Today’s Depressed Investment Environment to Generate Risk Appropriate ROEs * 2009 and 2010 figures are return on average statutory surplus. 2008 -2011 figures exclude mortgage and financial guaranty insurers. 2011H1 combined ratio including M&FG insurers is 110.5 , ROAS = 2.3%. Source: Insurance Information Institute from A.M. Best and ISO data. P/C Insurance Industry Combined Ratio, 2001–2011:H1* As Recently as 2001, Insurers Paid Out Nearly $1.16 for Every $1 in Earned Premiums Heavy Use of Reinsurance Lowered Net Losses Relatively Low CAT Losses, Reserve Releases Relatively Low CAT Losses, Reserve Releases 120 115.8 110 Cyclical Deterioration Best Combined Ratio Since 1949 (87.6) Higher CAT Losses, Shrinking Reserve Releases, Toll of Soft Market Avg. CAT Losses, More Reserve Releases 109.4 107.5 100.1 100 101.0 100.8 98.4 99.3 100.8 95.7 92.6 90 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011* * Excludes Mortgage & Financial Guaranty insurers 2008--2011. Including M&FG, 2008=105.1, 2009=100.7, 2010=102.4, 2011=110.5 Sources: A.M. Best, ISO.; III Estimated for 2011:H1 (Q1 actual ex-M&FG was 102.2). 69 Underwriting Gain (Loss) 1975–2011* Underwriting losses in 2011 will be much larger: $24.1B based on H1 data ($ Billions) $35 $25 Cumulative underwriting deficit from 1975 through 2010 is $455B $15 $5 -$5 -$15 -$25 -$35 -$45 -$55 The industry recorded a $10.4B underwriting loss in 2010 compared to $3.0B in 2009 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 1011* Large Underwriting Losses Are NOT Sustainable in Current Investment Environment * Includes mortgage and financial guaranty insurers in all years. 2011 figure is actual H1 underwriting losses of $24.098 billion. Sources: A.M. Best, ISO; Insurance Information Institute. Financial Strength & Underwriting Cyclical Pattern is P-C Impairment History is Directly Tied to Underwriting, Reserving & Pricing 71 P/C Insurer Impairments, 1969–2010 8 of the 18 in 2009 were small Florida carriers. Total also includes a few title insurers. 0 11 16 18 18 19 12 18 14 15 35 31 29 16 5 9 13 12 9 9 11 7 8 69 70 71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 10 15 12 20 16 14 13 19 30 31 34 34 40 36 41 50 49 50 47 49 50 48 55 60 60 58 70 The Number of Impairments Varies Significantly Over the P/C Insurance Cycle, With Peaks Occurring Well into Hard Markets Source: A.M. Best Special Report “1969-2010 Impairment Review,” June 21, 2010; Insurance Information Institute. Reasons for US P/C Insurer Impairments, 1969–2010 Historically, Deficient Loss Reserves and Inadequate Pricing Are By Far the Leading Cause of P-C Insurer Impairments. Investment and Catastrophe Losses Play a Much Smaller Role Reinsurance Failure Sig. Change in Business 3.6% 4.0% Misc. 8.6% Investment Problems (Overstatement of Assets) 7.3% 40.3% Affiliate Impairment Deficient Loss Reserves/ Inadequate Pricing 7.8% 7.1% Catastrophe Losses 7.8% Alleged Fraud 13.6% Rapid Growth Source: A.M. Best: 1969-2010 Impairment Review, Special Report, April 2011. 74 SURPLUS/CAPITAL/CAPACITY Have Large Global Catastrophe Losses Reduced Capacity in the Industry, Setting the Stage for a Market Turn? 76 Policyholder Surplus, 2006:Q4–2011:Q2 ($ Billions) 2007:Q3 Previous Surplus Peak $580 Surplus as of 6/30/11 fell by 1% below its all time record high of $564.7B set as of 3/31/11. Further declines are likely $559.1 $556.9 $544.8 $560 $540.7 $530.5 $540 $521.8$517.9 $515.6 $512.8 $520 $505.0 $496.6 $500 $487.1 $478.5 $511.5 $490.8 $480 $460 $440 The Industry now has $1 of surplus for every $0.78 of NPW—the strongest claimspaying status in its history. $455.6 $463.0 $437.1 $420 06:Q4 07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4 09:Q1 09:Q2 09:Q3 09:Q4 10:Q1 10:Q2 10:Q3 10:Q4 11:Q2 *Includes $22.5B of paid-in capital from a holding company parent for one insurer’s investment in a non-insurance business in early 2010. Sources: ISO, A.M .Best. Quarterly Surplus Changes Since 2007:Q3 Peak 09:Q1: -$84.7B (-16.2%) 09:Q2: -$58.8B (-11.2%) 09:Q3: -$31.0B (-5.9%) 09:Q4: -$10.3B (-2.0%) 10:Q1: +$18.9B (+3.6%) 10:Q2: +$8.7B (+1.7%) 10:Q3: +$23.0B (+4.4%) 10:Q4: +$35.1B (+6.7%) 11:Q1: +$42.9B (+8.2%) 11:Q2: +37.3B (+7.1%) 78 The Strength of the Economy Will Influence P/C Insurer Growth Opportunities Growth Would Also Help Absorb Excess Capital 79 2% 0.6% 4% 1.1% 1.8% 2.5% 3.6% 3.1% 2.7% 0.9% 3.2% 2.3% 2.9% 4.1% 6% 1.6% The Q4:2008 decline was the steepest since the Q1:1982 drop of 6.8% Real GDP Growth (%) 5.0% 3.9% 3.8% 2.5% 2.3% 0.4% 1.3% 2.5% 1.9% 1.9% 2.2% 2.5% 2.7% US Real GDP Growth* -0.7% 12:4Q 12:3Q 12:2Q 12:1Q 11:4Q 11:3Q 11:2Q 11:1Q 10:4Q 10:3Q 10:1Q 09:4Q 09:3Q 09:2Q 10:2Q 2011 got off to a sluggish start, but growth is expected to proceed at a more modest, though still relatively weak pace through 2012 -4.9% 09:1Q 08:4Q-6.8% -4.0% 08:3Q 08:2Q 08:1Q 07:4Q 07:3Q 07:2Q 07:1Q 2006 2005 2004 2000 -8% 2003 -6% 2002 -4% Recession began in Dec. 2007. Economic toll of credit crunch, housing slump, labor market contraction has been severe but modest recovery is underway 2001 -2% -0.7% 0% Demand for Insurance Continues To Be Impacted by Sluggish Economic Conditions, but the Benefits of Even Slow Growth Will Compound and Gradually Benefit the Economy Broadly * Estimates/Forecasts from Blue Chip Economic Indicators. Source: US Department of Commerce, Blue Economic Indicators 10/11; Insurance Information Institute. 80 Real GDP Growth: Minnesota vs. US, 1998-2010 8% 6% MN’s economy underperformed the US prior to the recession, in part because it did not experience a home building bubble 6.80% 5.30% 4.50% 4% 4.4% 4.10% 3.40% 4.8% 2.8% 4.2% 2.30% 3.4% 1.3% 2% 1.7% 0.80% 2.1% -2% -4% 99 00 1.9% 0.20% 0.30% 01 02 Minnesota GDP Growth US GDP Growth 03 1.40% 1.70% 0% 98 2.6% 3.20% 2.7% 04 05 06 MN’s economy has closely tracked the US economy overall in recent years 07 -0.3% 08 -2.5% 09 10 -2.90% Florida’s Dependence on the Construction Sector Will Cause it to Lag the Economic Recovery in the US Overall Source: Bureau of Economic Analysis; Insurance Information Institute. 81 1.9 1.7 1.5 1.3 1.1 0.9 0.7 0.5 The plunge and lack of recovery in homebuilding and in construction in general is holding back payroll exposure growth 0.55 0.59 0.59 0.70 0.91 2.1 New home starts plunged 72% from 2005-2009; A net annual decline of 1.49 million units, lowest since records began in 1959 1.19 1.01 1.20 1.29 1.46 1.35 1.48 1.47 1.62 1.64 1.57 1.60 1.71 1.85 1.96 2.07 1.80 1.36 0.91 (Millions of Units) 1.34 1.23 1.32 1.38 1.42 New Private Housing Starts, 1990-2022F Job growth, improved credit market conditions and demographics will eventually boost home construction 0.3 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11F12F13F14F15F16F17F1822F Little Exposure Growth Likely for Homeowners Insurers Until 2014. Also Affects Commercial Insurers with Construction Risk Exposure, Surety Source: U.S. Department of Commerce; Blue Chip Economic Indicators (10/11); Insurance Information Institute. 82 Labor Market Trends Massive Job Losses Sapped the Economy and Commercial/Personal Lines Exposure, But Trend is Improving 83 Unemployment and Underemployment Rates: Stubbornly High in 2011 January 2000 through September 2011, Seasonally Adjusted (%) 18 Traditional Unemployment Rate U-3 U-6 went from 8.0% in March 2007 to 17.5% in October 2009; Stood at 16.5% in Sept. 2011 Unemployment + Underemployment Rate U-6 16 Recession ended in November 2001 14 12 Unemployment kept rising for 19 more months Recession began in December 2007 Unemployment stood at 9.1% in September 10 Unemployment peaked at 10.1% in October 2009, highest monthly rate since 1983. 8 6 4 Sep 11 2 Jan 00 Jan 01 Jan 02 Jan 03 Jan 04 Jan 05 Jan 06 Jan 07 Jan 08 Jan 09 Jan 10 Peak rate in the last 30 years: 10.8% in November December 1982 Jan 11 Stubbornly high unemployment and underemployment will constrain overall economic growth Source: US Bureau of Labor Statistics; Insurance Information Institute. 84 Unemployment Rates by State, September 2011: Highest 25 States* 8.3 8.5 8.7 8.9 8.9 9.0 9.1 9.1 9.1 9.1 9.2 9.6 9.7 9.8 9.8 10.3 10.5 10.5 10.6 10.6 11.1 11.9 11.1 10.0 10 11.0 Unemployment Rate (%) 12 13.4 14 In September, 25 states reported overthe-month unemployment rate decreases, 14 had increases, and 11 and the District of Columbia had no change. 8 6 4 2 0 NV CA DC MI SC FL MS NC RI GA IL AL TN KY OR NJ AZ OH WA US ID CT IN MO TX AR *Provisional figures for September 2011, seasonally adjusted. Sources: US Bureau of Labor Statistics; Insurance Information Institute. 86 Unemployment Rates By State, September 2011: Lowest 25 States* The unemployment rate in MN at 6.9% is well below the 9.1% for the US overall 3.5 4 4.2 4.6 5.4 5.8 5.8 5.9 6.4 6.5 6.7 6.9 6.6 6.0 6 6.9 7.4 7.4 7.5 7.6 7.7 7.8 8.2 8.3 8.1 8 8.0 Unemployment Rate (%) 8.3 10 7.3 In September, 25 states reported overthe-month unemployment rate decreases, 14 had increases, and 11 and the District of Columbia had no change. 2 0 CO PA WV DE NY WI MT AK ME MD UT MA LA MN KS NM VA HI IA OK VT WY NH SD NE ND *Provisional figures for September 2011, seasonally adjusted. Sources: US Bureau of Labor Statistics; Insurance Information Institute. 87 Insurance Information Institute Online: www.iii.org Thank you for your time and your attention! Twitter: twitter.com/bob_hartwig Download at www.iii.org/presentations