Forecast - Amazon Web Services

Michigan’s

Financial Forecast

CorNet Michigan Chapter

January 14, 2010

Mark P. Haas

Chief Deputy Treasurer

Michigan Department of Treasury

Treasury Responsibilities

Tax Administration

Tax and Debt Collection

Financial Management

Local Government Services

Financing Higher Education

Investing All State Funds

1

Treasury Customers

Colleges and Universities

Hospitals

Public Schools

Local Government Units

Public Retirees

Higher Ed Students

Michigan Taxpayers

2

Treasury’s Commitment

Maintain the State’s financial integrity.

Fair and consistent administration of tax laws.

Provide efficient and effective professional services.

Provide access to financial resources for higher education, K-12, local government, and hospitals.

3

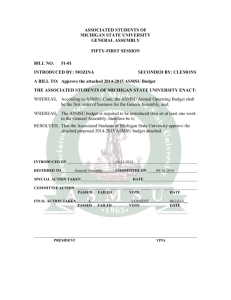

2010 Treasury Budget

All Funds $1,548,257.3 / General Fund (GF) $135,597.7

($s in millions)

Revenue Sharing

Grants

Debt Service

PILT

Operations

Pass Through Funds

Revenue Sharing $1,133.7

Grants $103.8

Debt Service

Payments in Lieu of Taxes

$82.2

$14.4

_________

$1,334.1

Operations Funding

Revenue Generation $120.6

Student Financial $37.5

Investments $16.7

Local Government $17.4

Customer Service $12.1

State Banking $7.1

Revenue Forecasting $1.5

Bond Finance $1.3

________

$214.2

4

Overview

How bad was the recession?

Is it over?

What about Michigan?

Real estate turn around?

How does the State budget look?

What does Michigan need to do?

5

How Bad is the Recession?

6

Current Recession Longest

Since Great Depression

Number of Months from Peak to Trough

U.S. Recessions

13

8

11

10

8

10

11

16

6

16

8 8

10

19

1937-

1938

1945 1948-

1949

1953-

1954

1957-

1958

1960-

1961

1969-

1970

1973-

1975

1980 1981-

1982

1990-

1991

2001 Avg.

Post

War

2007

Thru

Jun

09

Source: NBER, Assumes recession ends beginning of 3 rd quarter 2009 7

Current Recession GDP Decline

Steepest on Record

Percent Change, Economy Peak to Trough

0.7%

-0.5%

-0.2%

-1.6%

-2.5%

-3.1%

-3.2%

-2.2%

-2.6%

-1.4%

-1.7%

-3.7%

1948-

1949

1953-

1954

1957-

1958

1960-

1961

1969-

1970

1973-

1975

1980 1981-

1982

1990-

1991

2001 Avg.

Post

War

2007

To

09Q2

Source: Bureau of Economic Analysis, U.S. Department of Commerce.

Data not avail for 1937-38 and 1945 recessions.

8

U.S. Employment Decline

Third Steepest

Percent Change, Economy Peak to Trough

-5.0%

-3.1%

-4.0%

-2.3%

-1.2%

-1.6%

-1.1%

-3.1%

-1.1%-1.2%

-2.9%

-4.9%

-7.9%

1945 1948-

1949

1953-

1954

1957-

1958

1960-

1961

1969-

1970

1973-

1975

1980 1981-

1982

1990-

1991

2001 Avg.

Post

War

2007

Thru

Oct

09

Source: Bureau of Economic Analysis, U.S. Department of Commerce. Data not avail for 1937-38 recession.

9

Net Worth Drops

19 Percent From Peak

Net Worth Outstanding, Households and Nonprofit Organizations

(billions)

$70,000

$66,007

2007Q2

$60,000

$50,000

$40,000

$53,423

2009Q3

$30,000

$20,000

$10,000

$0

19

52

Q

1

19

54

Q

3

19

57

Q

1

19

59

Q

3

19

62

Q

1

19

64

Q

3

19

67

Q

1

19

69

Q

3

19

72

Q

1

19

74

Q

3

19

77

Q

1

19

79

Q

3

19

82

Q

1

19

84

Q

3

19

87

Q

1

19

89

Q

3

19

92

Q

1

19

94

Q

3

19

97

Q

1

19

99

Q

3

20

02

Q

1

20

04

Q

3

20

07

Q

1

20

09

Q

3

Source: freelunch.com (Federal Reserve Bank Flow of Funds).

10

One for the Record Books

Calendar 2009 Estimate

April

2008

Forecast

15.2

Light Vehicle Sales (millions)

Housing Starts (million units) 1.131

US Unemployment Rate 5.8%

US Payroll Employment (% chg) 0.4%

US Personal Income (% chg) 3.6%

Jan 2010

Forecast

10.3

0.558

9.3%

-3.7%

-1.4%

Comments

Lowest Since 1970

Lowest Back to 1959

Highest Since 1983

Lowest Back to 1940

Lowest Since 1938

Source: Estimates Compare April 2008 and January 2010 Global Insight Forecasts 11

Is the Recession over?

12

Leading Indicators Point to

National Recovery

Weekly Leading Index, Smoothed Annual Growth Rate

40.0%

30.0%

20.0%

10.0%

0.0%

-10.0%

-20.0%

-30.0%

-40.0%

1/

5/

20

07

4/

5/

20

07

7/

5/

20

07

10

/5

/2

00

7

1/

5/

20

08

4/

5/

20

08

7/

5/

20

08

10

/5

/2

00

8

1/

5/

20

09

4/

5/

20

09

7/

5/

20

09

10

/5

/2

00

9

Source: Economic Cycle Research Institute.

01/01/10

24.2%

13

Recovery Observed in 3rd

Quarter 2009

Real GDP Growth

2.7%

1.4%

3.5%

6.9%

3.0%

Growth

3.2%

1.6%

3.6%

0.1%

-1.3%

-1.1%

5.4%

3.5%

3.0%

4.1%

3.1%

2.1%

1.7%

1.5%

0.1%

3.0%

3.6%

3.2%

2.1%

1.2%

1.5%

-0.7%

-2.7%

2.2%

-1.0%

5.1%

2.5%

2.0%

2009Q3

-5.4%

-6.4%

2001 Q1 2002 Q1 2003 Q1 2004 Q1 2005 Q1 2006 Q1 2007 Q1 2008 Q1 2009 Q1 2010 Q1

Figures are annualized percent change from preceding quarter in 2005 chained dollars.

Source: Bureau of Economic Analysis. Forecast quarters in red are the December 2009 Global Insight forecast.

14

U.S. Has Lost 7.2 Million Jobs

Since December 2007

215

120

4

(72)

(122)

(160)

(85)

(128)

(175)

(321)

(380)

(303) (304)

(463)

(519)

(597)

(681)

(741)

Nov 07 Jan 08 Mar 08 May 08 Jul 08 Sep 08 Nov 08 Jan 09 Mar 09 May 09 Jul 09 Sep 09 Nov 09

Source: U.S. Bureau of Labor Statistics, U.S. Department of Labor 15

1400

1200

1000

800

1600

Stock Market Up 68 Percent

From March 9 th Low

S&P 500 Closing Level

1565

10/09/07

1136

01/12/10

677

03/09/09

600

1/

2/

20

01

7/

2/

20

01

1/

2/

20

02

7/

2/

20

02

1/

2/

20

03

7/

2/

20

03

1/

2/

20

04

7/

2/

20

04

1/

2/

20

05

7/

2/

20

05

1/

2/

20

06

7/

2/

20

06

1/

2/

20

07

7/

2/

20

07

1/

2/

20

08

7/

2/

20

08

1/

2/

20

09

7/

2/

20

09

Source: freelunch.com, reuters.com

16

Blue Chip Economists’

Take on the Recovery

Consensus predicts real GDP will grow slightly exceeding its trend rate (2.8% to 3.1%) over the next five quarters.

Although with growth better than predicted six months ago, the projected rate of growth still falls well short of that typically seen after steep recessions.

Labor markets are expected to improve, but modestly, keeping the unemployment rate from falling back below

10% on a sustained basis until the final quarter of this year.

Source: December 2009 Blue Chip Indicators.

17

GDP Generally Strong in Year After Recession

Recession

Trough

1949Q4

1954Q2

1958Q2

1961Q1

1970Q4

1975Q1

1980Q3

1982Q4

1991Q1

2001Q4

2009Q2

Peak to

Trough

Change

-1.6%

-2.5%

-3.1%

-0.5%

-0.2%

-3.2%

-2.2%

-2.6%

-1.4%

0.7%

-3.7%

Y-O-Y

GDP Growth

4 Qtrs

Later

13.4%

7.9%

9.5%

7.5%

4.5%

6.2%

4.4%

7.7%

2.6%

1.9%

??

Source: BEA and Dept. of Treasury calculations. Peaks and trough are as designated by NBER for economy .

18

Government

Federal Outlays and Receipts

(last obs. September 2009)

3500

Outlays

3000

Outlays are far outpacing receipts.

2500

2000

1500

1000

500

Jan-89 Jan-92 Jan-95 Jan-98 Jan-01 Jan-04

Receipts

Jan-07

Source: US Treasury; Encima Global 19

Government

U.S. Federal Government

Debt Outstanding

(last obs. 2009, projected by CBO 2010 to 2019)

20

Rise in national debt (marketable debt held by the public) is likely to be much higher than current estimates.

More likely

15

10 current law

5 debt held by public

0

21916 23377 24838 26299 27760 29221 30682 32143 33604 35065 36526 37987 39448 40912 42376

Source: Department of Treasury; CBO; Encima Global 20

Government

Federal Government Debt as % of GDP

(last obs. 2009, forecast 2010 to 2019)

80

70

Debt to GDP ratio heading toward

80% even with optimistic GDP growth assumptions.

OMB forecast of

President's FY2010 budget

60

50

40

CBO baseline

30

20

1950 1960 1970 1980 1990 2000 2010

21

Source: OMB; CBO; Encima Global

Government

Social Security and

Medicare/Medicaid Spending

12

10

8

6

4

2

0

1960

Medicare and Medicaid outlays much bigger than Social Security’s.

Medicare & Medicaid expenditures

1970

Social Security expenditures

1980 1990 2000 2010

2025

2015

CBO projections

2020 2030 2040 2050

Source: CBO; Encima Global 22

Prices and Markets

Volatility in Headline CPI

(-1.3 year-over-year for last obs. September 2009, projected to December 2009)

0

6%

5%

4%

3%

2%

1%

0%

-1%

-2%

-3%

Jan-95 Jan-97 Jan-99 Jan-01 Jan-03 Jan-05 Jan-07 Jan-09

Source: Bureau of Labor Statistics; Encima Global

23

What about Michigan?

24

Michigan Employment Never

Recovered in Past Expansion

8%

4%

0%

-4%

-8%

-12%

-16%

-20%

Jun

00

Jun

01

Jun

02

Jun

03

Jun

04

Jun

05

Jun

06

Jun

07

Jun

08

Note: Peak is calculated from Michigan’s June 2000 Peak.

Jun

09

U.S.

Indiana

Ohio

Michigan

Source: Bureau of Labor Statistics 25

Worst Michigan

Employment Drop on Record

Ten Year Change

50%

40%

30%

20%

10%

0%

-10%

Nov 1999 – Nov 2009

-20% -16.5%

Ja n-

66

Ja n-

68

Ja n-

70

Ja n-

72

Ja n-

74

Ja n-

76

Ja n-

78

Ja n-

80

Ja n-

82

Ja n-

84

Ja n-

86

Ja n-

88

Ja n-

90

Ja n-

92

Ja n-

94

Ja n-

96

Ja n-

98

Ja n-

00

Ja n-

02

Ja n-

04

Ja n-

06

Ja n-

08

Source: Bureau of Labor Statistics. Non-seasonally adjusted data.

26

Michigan Loses Nearly 1 Million Jobs

88.0

Michigan Wage and Salary Employment Y-O-Y Change

(In Thousands)

-112.7

-76.7

-71.0

-17.0

-9.2

-63.2

-58.7

-109.2

-85.0

-34.0

-283.0

91-

00

Avg.

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Forecast

Note: Bureau of Labor Statistics. 2009-2011 estimates are from the January 2010 Consensus forecast.

27

Michigan Unemployment Rate

To Rise Sharply

Michigan November Rate was 14.7%

14.1%

15.7% 15.3%

3.7%

5.2%

6.2%

7.1% 7.1% 6.8% 6.9% 7.1%

8.4%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Forecast

Source: Bureau of Labor Statistics and January 2010 Consensus Forecast 28

Michigan Personal Income

Falling Relative to U.S.

Michigan per Capita Income as a Percent of U.S. Per Capita Income

1.25

1.2

1.15

1.1

1.05

1

0.95

0.9

0.85

93%

122%

87%

19

29

19

33

19

37

19

41

19

45

19

49

19

53

19

57

19

61

19

65

19

69

19

73

19

77

19

81

19

85

19

89

19

93

19

97

20

01

20

05

Source: Department of Treasury calculations from Bureau of Economic Analysis data.

29

Forecast of Michigan Real Disposable

Income Growth

(1982 –1984 $), 2009–2011

2%

1%

0%

- 1%

0.2

- 2%

- 3%

2007

RSQE: January 2010

RSQE: January 2010

0.4

2008

1.3

2009

0.7

2010

– 1.9

2011

30

Wage and Personal Income Growth

2001– 2008

U.S.

Michigan

Total personal income

Per capita personal income

37.7%

29.1%

16.6%

16.6%

State rank, Michigan per capita income

2001

20

2008

37

RSQE: January 2010

31

Industry Restructuring

25-Year Recovery Cycle

1960

1980

2000

New England Textile Industry

Pittsburgh Steel Industry

Michigan Auto Industry

32

Real Estate Turnaround?

33

Home Prices Fall Sharply

U.S. Prices Fall After Sharp Run Up

30.00%

20.00%

10.00%

0.00%

-10.00%

U.S. 10 City

-20.00%

Detroit Area

-30.00%

Jan-92 Jan-94 Jan-96 Jan-98 Jan-00 Jan-02 Jan-04 Jan-06 Jan-08

Oct 09

-15.1%

Source: Case Shiller 10-Metro Area Home Price Index.

34

1.2

1.0

0.8

U.S. Home Sales Turning

Swung by Homebuyers’ Tax Credit

1.4

(Millions of units) (Millions of units)

7.5

7.0

6.5

6.0

0.6

0.4

0.2

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

5.5

5.0

4.5

New Home Sales (Left scale)

Source: Global Insight

Existing Home Sales (Right scale)

35

2500

Record Low U.S. Housing Starts

Down 75% from Peak

Jan 06

2,273

2000

1500

1000

500

0

Jan-90 Jan-92 Jan-94 Jan-96 Jan-98 Jan-00 Jan-02 Jan-04 Jan-06 Jan-08

Source: New Privately Owned Housing Units Started (thousands), U.S. Dept of Commerce

Nov 09

574

36

Michigan Home Building

Falls Precipitously

New Private Housing Units Authorized in Michigan

Year

2004

2005

2006

2007

2008

2009 YTD

Detroit

PMSA

22,990

17,326

9,592

4,325

2,590

1,223

Grand

Ann Arbor Rapids

2,708

1,676

6,886

5,826

775

565

347

187

4,278

1,866

1,064

721

Lansing

2,206

2,121

1,231

768

383

219

Total

54,721

45,328

29,191

17,767

10,911

6,503

Source: U.S. Department of Commerce. 2009YTD through November. 37

Overall Michigan Property

Value Growth Slowing

Yearly Percent Change

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010est

2011est

Multiplier for

Property

2.8%

2.7%

1.6%

1.9%

3.2%

3.2%

1.5%

2.3%

2.3%

3.3%

3.7%

2.3%

4.4%

-0.3%

2.5%

Source: State Tax Commission and January 2010 Consensus Conference .

Total SEV Taxable Value

Growth Growth

8.2% 5.7%

9.5%

9.9%

9.0%

10.0%

6.1%

6.0%

5.5%

7.1%

9.8%

7.5%

6.3%

5.9%

5.0%

3.8%

-1.3%

-5.4%

NA

NA

6.7%

4.8%

5.7%

5.6%

5.8%

5.2%

1.4%

-0.8%

-8.0%

-4.3%

38

Michigan Real Estate

Transfer Tax Falls

Year-over-Year Change in 6 Month Trailing Average

30.00%

20.00%

10.00%

0.00%

-10.00%

-20.00%

Sep 04

24.0%

Dec 09

-1.2%

-30.00%

-40.00%

Jan-

00

Aug-

00

Mar-

01

Oct-

01

May-

02

Dec-

02

Jul-

03

Feb-

04

Sep-

04

Apr-

05

Nov-

05

Jun-

06

Jan-

07

Aug-

07

Mar-

08

Oct-

08

May-

09

Dec-

09

Source: Michigan Department of Treasury

39

Michigan Building Permits

1963 – 2008 and Forecast 2009 – 2011

80,000

70,000

60,000

50,000

40,000

30,000

20,000

Forecast

10,000

0

'63 '67

'65 '69

'71 '75

'73

'79

'77 '81

'83 '87 '91 '95 '99

'85 '89 '93 '97

'03

'01 '05

'07

'09

'11

40

RSQE: January 2010

Mortgage Delinquency

Rates Double

Source: Economy.com using Mortgage Bankers Association Data 41

Real Estate Market Rebound

Depends on Interest Rates

8

Actual

6

6.2

4

4.3

3.4

5.9

4.9

Conv. Mortgage

10 Year T-Note

3-Month T-bill

5.6

3.9

3.5

Forecast

5.7

4.1

3.2

2

0

1.3

0.3

0.3

0.1

4 1 2 3 4 1 2 3 4 1 2 3 4 1 2 3 4

’07 2008 2009 2010 2011

RSQE: January 2010

42

How Do State

Revenues Look?

43

Difficult Economic Times

Reduce Revenue Growth

Cause

Recession

Housing Boom/Bust

Auto Industry/

Restructuring

Effect

Employment Loss and

Income Loss

Credit Crisis and

Consumption Drop

Relative Decline in

Personal Income

44

7.5%

GF-GP Revenues Drop Sharply in FY 2009 and FY 2010

GF-GP Revenues

Year-Over-Year Pct. Change

12.5%

3.0%

1.0%

3.3%

0.6% 1.0%

-0.5%

-8.2%

-6.3% -5.6% -6.3%

-21.3%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

45

State GF-GP Revenue at FY ‘91 Level

Down 19% Since 2000

Billions of Dollars

$12.0

$10.0

$8.0

$6.0

$4.0

$2.0

$0.0

1991

$6.9B

2000

$9.8B

2010

$6.9B

19

61

19

65

19

69

19

73

19

77

19

81

19

85

19

89

19

93

19

97

20

01

20

05

20

09

46 Note: GF-GP figures are presented on a Consensus basis. 2009 and 2010 are estimates.

GF-GP and School Aid Revenue

Baseline Growth Rates Before Tax Changes

8.0%

4.0%

0.0%

-4.0%

1.1%

-2.7%

2.9%

6.5%

8.3%

6.0%

6.1%

5.5%

5.9%

7.9%

6.1%

-1.7%

-1.3%

-0.9%

1.9%

3.8%

1.0%

2.6%

1.1%

-8.0%

-12.0%

1990 1993 1996 1999 2002 2005

0.9%

-4.7%

-10.5%

2008 2011

Average Agency

Forecasts

47

Balancing FY 2011 GF/GP

Will Be Difficult

Consensus Revenue Estimate

Other Resources

Total Estimated Resources

Expenditures: Current Services Estimate

Projected Year End Balance*

Billions

$7.0

$1.0

$8.0

$9.6

($1.6)

* ARRA funding available to offset GF expenditures will decline from $1.2 billion in FY10 to $0.2 billion in FY11.

Source: Michigan Department of Treasury 48

Balancing FY 2011 SAF Budget

Tough on Schools

Beginning Balance

Consensus Revenue Estimate

Fed Aid and GF Grant (assume FY 10 Amt)

ARRA Funds

Total Estimated Resources

Expenditures Current Services Estimate

Projected Year End Balance

FY 2011

(billions)

$0.1

$10.5

$1.6

$0.2

$12.4

$12.8

($0.4)

Source: Michigan Department of Treasury 49

What Does Michigan Need to Do?

Consolidate government services at both the state and local level.

Reform the state’s tax structure so that it will grow with the State’s economy and not discourage economic growth.

Slow the growth of government healthcare and tax expenditures.

Maintain or increase the investment in education.

Many Units of Government

Local Governments

83 Counties

275 Cities

258 Villages

1,240 Townships

K-12 Schools

551 Local School Districts

230 Charter Schools

57 Intermediate School Districts

Colleges and Universities

15 Public Universities

29 Community Colleges

51

Three Types of State Spending:

Grants, Services, and Tax Breaks

Grants - $15.3 Billion

Services - $13.1 Billion

Federal Funds - $14.9 Billion

Tax Expenditures - $35.8 Billion

_ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _ _

Pensions and Retirement Benefits

52

Tax Breaks / Expenditures

Larger Than Tax Credits

Tax Breaks

Tax

Collections

Lisa M Winans

Source: House Fiscal Agency 53

Conclusion

U.S. recession worst in decades.

Michigan has been in a recession since 2001 due to auto sector restructuring and U.S. recession.

Michigan recovery will require U.S. recovery, stability in the auto sector, and time.

Michigan real estate market likely at bottom but slow recovery ahead.

54