Fair Housing

Legal Update

Legal Update Learning Objectives

After study of this module you will be able to:

1. Identify current federal legislation affecting the real estate business.

2. Identify Virginia Assembly legislative updates.

3. Recognize recent changes to VREB Rules &

Regulations.

Federal Legislative Update

Lead-Based Paint Disclosure

1

Under direction of the Residential Lead-

Based Paint Hazard Reduction Act of

1992, HUD and EPA require disclosure of all available information on lead-based paint and lead-based paint hazards for the sale or lease of properties built prior to

1978.

Federal Legislative Update

Lead-Based Paint Disclosure

2

Effective December 1996, all purchasers and lessees of property built before 1978 must be given the pamphlet Protect Your Family from

Lead in Your Home , and sign the appropriate

“Purchase” or “Lease” disclosure forms, which should have been previously signed by the seller or landlord.

Federal Legislative Update

Lead-Based Paint Disclosure

3

Purchasers have the right to a 10-day inspection or risk assessment period. Although the seller is not required to remove lead-based paint, the purchaser may withdraw from the contract in the event lead-based paint is found.

Purchasers and sellers may negotiate possible methods of reducing leadbased paint hazards.

Federal Legislative Update

Lead-Based Paint Disclosure

4

The real estate agent is responsible for insuring that

• sellers and landlords are aware of their obligations

• sellers and landlords make the proper disclosures

• sellers give purchasers an opportunity for an inspection

• lease and sales contracts contain appropriate language

Federal Legislative Update

Lead-Based Paint Disclosure

5

EPA and HUD have recently begun inspecting broker files to verify that all appropriate disclosure forms are included in the pertinent company files.

Federal Legislative Update

Health Care Deduction for Self-employed

•

Current legislation allows a 100% deduction of allowable health-care expenditures

•

Under prior regulations, self-employed persons could deduct 45% of their health care insurance in 1998, 60% in 1999, 70% in

2002, and 100% in 2003.

Federal Legislative Update

RESPA Rules and Regulations

The rules and regulations of The Real Estate Settlement

Procedures Act have been under study for a number of years. The most current concern has been over the “onestop” shopping concept, wherein a real estate brokerage company also has affiliated companies for mortgage loans, title insurance, hazard insurance, escrow and settlement services, and/or other related services.

RESPA seeks to insure that brokerage companies are not receiving kickbacks for services not performed. After a survey of the public showed that “one stop” shopping is perceived favorably by the consumers, the regulations are under continuing review.

Federal Legislative Update

Tax Relief Act of 1997

1

•

The tax benefit for the sale of a personal residence was greatly enhanced with an exemption from capital gains tax on profit up to $500,000 for a married couple and $250,000 for a single person.

•

The former one-time exclusion of $125,000 for persons 55 years of age or older no longer applies.

•

The new exemption applies to all properties used as a primary residence for two years.

Federal Legislative Update

Tax Relief Act of 1997

2

• The two years may be an aggregate of any two of the previous five! [Actual time required is a total of 730 days!]

•

It does not matter if the property formerly was used as a rental property, as long as the two-year residence requirement is met.

• The exemption may be taken once every two years, and there are no “buy-up” requirements.

•

Special provisions have been made for widows and widowers or for others needing to sell due to extreme extenuating circumstances.

•

The new law affects all properties sold after May 7, 1997.

Federal Legislative Update

Other Tax Matters

The maximum capital gains tax rate on the sale of investment property was reduced from 28% to 20%.

For someone in the 15% bracket the reduction went from

15% to 10%.

The depreciation recapture rate will be 25% for property held for a minimum of twelve months, although investment property is usually depreciated over several years.

Proposed legislation might further reduce the depreciation recapture rate to 20%

Federal Legislative Update

Private Mortgage Insurance

1

Legislation effective July 29, 1999, mandated that for all new loans private mortgage insurance must be dropped when an equity position of 22% (Loan-to-Value of 78%) has been reached. The 22% equity position is derived from the original value of the property and does not allow for any appreciation ( or depreciation ) of the value. The borrower may request an elimination of the PMI with an equity position of 20%. ( This might require an appraisal.)

Federal Legislative Update

Private Mortgage Insurance

2

Fannie Mae and Freddie Mac have agreed to drop

•

•

•

•

PMI on all loans originated even before July 1999, if the properties have reached the 22% equity position, or the “half-life” of the term of the loan has arrived, the borrower is in good standing on the loan, and the borrower has not signed a previous agreement with regard to elimination of PMI.

Federal Legislative Update

Private Mortgage Insurance

3

FHA and VA loans are not affected by the new legislation.

Federal Legislative Update

Home Office Deduction

Under 1999 regulations, persons who perform administrative and ministerial tasks in their home office, but perform actual services that generate income outside the home office, are eligible for a home office deduction on their income tax. The prevailing tax requirements for claiming part of a residence for a business must be followed.

Federal Legislative Update

Effective October 1, 2000, for electronic transactions and

March 1, 2001, for electronic records.

Electronic Signatures – (H.R. 1714, S. 761, P.L. 106

229) This law simplifies the real estate transaction by allowing two parties to treat electronic signatures with the same legal standing as “pen and ink” versions. The

Electronic Signatures Law allows consumers and businesses to do all of the following procedures:

Federal Legislative Update

• Contract electronically for the purchase of goods and services

• Contract electronically for sale and lease of real estate

• Process mortgage loan transactions electronically

• Receive related state and federal disclosures online

• Transfer promissory notes electronically

• Notarize transactions electronically

• Obtain and maintain electronic records of transactions.

General Assembly Update

Information provided by Virginia Association of

REALTORS®. For more detail see www.varealtor.com/MembersOnly/Legislative Information .

Abbreviations used:

•

House Bill (HB)

•

Senate Bill (SB)

•

Property Owner Association (POA)

General Assembly Update

Licensee’s Ability to Prepare BPO’s/CMA’s

On a Fee for Service Basis

HB 2334 establishes that real estate licensees may provide evaluations of property ( as in a Broker Price

Opinion or Comparative Market Analysis ) and charge a fee for this service. The evaluation may not be referred to as an appraisal under any circumstances.

General Assembly Update

Property Management

(Landlord Tenant Act) Changes

1

HB 2276, SB 132 require that rent be placed in a court escrow account in a case where a tenant has requested a continuance or in the event of a contested trial date where the case involves an unlawful detainer action.

General Assembly Update

Property Management

(Landlord Tenant Act) Changes

2

HB 2302 provides that tenants must not remove or tamper with a properly working smoke detector.

General Assembly Update

Property Management

(Landlord Tenant Act) Changes

3

HB 2537, SB 1173 provide that a guest or invitee of a tenant may be barred from the premises for conduct violating the terms of the rental agreement, local ordinance, or state or federal law.

General Assembly Update

Property Management

(Landlord Tenant Act) Changes

4

HB 1862 authorizes localities to establish procedures permitting property owners to designate the local law-enforcement authority to enforce trespass violations.

General Assembly Update

Property Management

(Landlord Tenant Act) Changes

5

SB 933 requires that security deposits accrue interest at an annual rate equal to one percent below the Federal Reserve Discount rate as of

January 1 of each year

General Assembly Update

Property Owner’s Association and

Condominium Act Changes

1

HB 1369 requires posting of signs at least 48 hours before pesticides are applied to common areas.

General Assembly Update

Property Owners’ Association and

Condominium Act Changes

2

HB 1595 provides that meetings shall be held at least once a year in accordance with the bylaws of the association.

General Assembly Update

Property Owners’ Association and

Condominium Act Changes

3

HB 1632 requires that requests for records be made for a purpose related to the owner’s membership and clarifies the types of documents to which an association may deny access.

General Assembly Update

Property Owners’ Association and

Condominium Act Changes

4

SB 999 provides that a declaration may be amended by agreement of two-thirds of the owners of lots affected by the declaration.

General Assembly Update

Property Owners’ Association and

Condominium Act Changes

5

HB 2063 increases maximum charge to be assessed to a member of the association for a single offense or violation of the association’s rules from $50 to $100.

General Assembly Update

Property Owners’ Association and

Condominium Act Changes

6

HB 2534 conforms Condo Act and Real Estate Time

Share Act regarding conveyance of time-share interest in condominium that is not completed: developer must post completion bond for 100% of cost for completion and disclose status of uncompleted unit to purchaser.

General Assembly Update

Property Owners’ Association and

Condominium Act Changes

7

SB 1090 provides than when a contract is cancelled based on a seller failing to provide contract disclosures, or based on a purchaser’s right to cancellation, a deposit is to be returned within 30 days.

General Assembly Update

Property Owner’s Association and

Condominium Act Changes

8

SB 1138 provides that members of the association that have requested notice must be provided with time, date and place of all regular and special meetings.

General Assembly Update

Property Owner’s Association and

Condominium Act Changes

9

HB 2505 exempts persons engaged in property management from liability if a worker is injured while engaged in the maintenance or repair of real property managed by that person, as long as the property manager is not engaged in the same business as the injured worker and does not profit from the services of the injured worker.

General Assembly Update

Property Owner’s Association and

Condominium Act Changes

10

HB 2699 requires unit owners to disclose to purchaser all of the following:

•

The unit is subject to Condominium Act

•

The seller must provide resale certificate

•

The purchaser has the right to cancel within 3 days of receipt of resale certificate

•

The right to receive resale certificate and to cancel are waived conclusively if not exercised prior to settlement

( Conforms Condo Act to POA Act )

General Assembly Update

Real estate Closing and Settlements

(CRESPA)

1

SB 1278 establishes the Real Estate Settlement

Agent Registration Act, which governs qualifications and financial responsibility for persons conducting settlements not previously covered by Consumer Real Estate Settlement

Protection Act (CRESPA). All lay settlement agents must comply with CRESPA requirements.

General Assembly Update

Real estate Closing and Settlements

(CRESPA)

2

HB 2600 requires any person making referral to an affiliate settlement service provider to disclose in accordance with federal RESPA regulations and requires disclosure of ownership of even less than 1%

( currently exempt under RESPA ).

General Assembly Update

Occupational Regulation

1

HB 1861 increases the penalty for any board violation from $1000 to $2500 .

General Assembly Update

Occupational Regulation

2

HB 2503, SB 1330 authorizes a business entity salesperson where a single licensee is an owner or officer to be granted a license in a fictitious name.

General Assembly Update

Occupational Regulation

3

HB 2517 requires licensed and certified residential appraisers to authenticate all written appraisal reports by signature, license designation and license number only. No seal is required.

General Assembly Update

Occupational Regulation

4

HB 2246 increases the Real Estate Appraiser

Board from four to six licensed appraisers, and decreases to one mortgage lender, and from three to two citizens. Current members will not be affected.

General Assembly Update

Spot Blight Abatement Legislation

1

HB 2577 creates a fund to make loans to localities for acquisition, demolition, removal, rehabilitation or repair of derelict structures causing blight in the community.

General Assembly Update

Spot Blight Abatement Legislation

2

HB 1962 allows localities to impose a $25 annual registration fee on owners of vacant buildings with a $250 fine for failure to register.

General Assembly Update

Spot Blight Abatement Legislation

3

HB 2026, HB 2639, SB 1242 make the spot blight abatement law applicable statewide.

General Assembly Update

Spot Blight Abatement Legislation

4

HB 2630 allows localities to waive liens associated with weed or trash removal, property repair or demolition to facilitate sale of the property with such lien becoming a personal responsibility of the current owner.

General Assembly Update

Spot Blight Abatement Legislation

5

HB 2211 allows localities to streamline the tax delinquent sale process for properties assessed at

$20,000 or less in cases where

• tax is delinquent for three years: land is declared nuisance, notice has been given, liens placed on property have not been paid, or

• tax is delinquent for seven years.

General Assembly Update

Megan’s Law Disclosure

1

HB 1204 added a disclosure to the Virginia Residential

Property Disclosure/Disclaimer Form informing buyers that it is their responsibility to exercise whatever due diligence they feel is necessary to collect information regarding released sex offenders. That information is available on the internet at www.vsp.state.va.us/vsp.html

General Assembly Update

Megan’s Law Disclosure

2

HB 570 specifies that information regarding released sex offenders shall be made public on the

Internet and is to include name, address, picture and criminal record. The public may also request information from their local law enforcement office.

Schools, day care centers and child service groups will be notified through a proactive notice system.

General Assembly Update

CRESPA Bills

SB 281 and HB 1265 clarified that real estate licensees performing ministerial acts ( such as ordering a termite inspection ) do not have to register under the Consumer Real Estate

Settlement Protection Act.

General Assembly Update

Commercial Broker’s Lien Change

HB 1242 ensures that purchasers of a commercial building with actual knowledge of brokerage fees due to a broker will be liable for payment regardless of whether the broker has filed a lien.

General Assembly Update

Virginia Industrial Development Authority

Act Change

HB 1405 explicitly gives Industrial

Development Authorities the authority to pay commissions to real estate brokers, including buyer agents.

General Assembly Update

Calculation of Interest on Security Deposits

HB 1355 changes the law regarding calculation of interest on security deposits from six-month increments to an annual rate equal to the Federal Reserve Discount rate as of January 1 of each year.

General Assembly Update

Disposal of Abandoned Property

HB 1247 allows a landlord to dispose of abandoned property provided the landlord has given the tenant 10 days notice.

•

•

•

Virginia Real Estate Board

Regulations

Changes and Updates to Regulations

Summary of changes effective April 2003

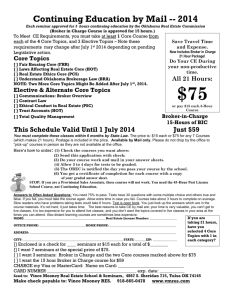

Increase in continuing education hours from 8 to 16 for licensees renewing after July 1, 2004

New 30-hour education requirement for all new licensees who receive their initial license after January 1, 2004

(Handouts Available Upon request)

Virginia Real Estate Board Rules and Regulations

Effective 01/01/99 and 04/01/03

Summary

A. Significant changes

1.

The numbering system has been changed to comply with the requirements of the Virginia Administrative Code

(VAC).

2.

The definition of “actively engaged” has been changed from an average of 20 to 40 hours per week. (18 VAC

135-20-10)

3.

Requirements for obtaining a salesperson’s or associate broker’s license as a business entity have been added. (18

VAC 135-20-45)

4.

Requires applicants for licensor by reciprocity to take and pass the Virginia portion of the licensing examination.

(18 VAC 135-20-60)

Virginia Real Estate Board Rules and Regulations

Effective 01/01/99 and 04/01/03

Summary

5. Requires a roster of every salesperson and broker assigned to a branch office to be posted in that office ( 18 VAC 135-20-160 )

6. Requires deposit of escrow funds by the end of the fifth business banking day following ratification ( sale ) or receipt ( lease ), unless otherwise agreed to in writing. ( 18 VAC 135-20-

180 )

7. Advertising requirements have changed to add the internet to the definition of advertising. ( 18

VAC 135-20-190 )

Virginia Real Estate Board Rules and Regulations

Effective 01/01/99 and 04/01/03

Summary

8. Disclosure of interest requirements were changed to incorporate agency law. ( 18 VAC 135-20-210 )

9. Record keeping provisions changed to require that a copy of each disclosure of a brokerage relationship, each executed contract, agreement and closing statement related to the real estate transaction in the broker’s control or possession be retained for three years. ( 18 VAC 135-20-320 )

Virginia Real Estate Board Rules and Regulations

Effective 01/01/99 and 04/01/03

Summary

10. Effective 07/01/04 , 16 hours of Continuing

Education must be completed for license renewal. You must have 8 hours in the mandatory topics which includes: 2 hours in Fair Housing and the remaining 6 hours must be a minimum of

1 hour in each of the following categories: Legal

Updates, Real Estate Agency, Real Estate

Contracts, and Ethics & Standards of Conduct.

The remaining hours may be real estate related or in the specific categories.

Virginia Real Estate Board Rules and Regulations

Effective 01/01/99 and 04/01/03

Summary

11. If you received a new salesperson license (active or inactive) after December 31, 2003, and this is your FIRST TIME RENEWAL , you will need to complete 30 hours of Post License Education instead of Continuing Education.

Current VREB Members

S. Ronald Owens, Chairman

R. Schaefer Oglesby, Vice Chair

Marjorie Clark

Florence Daniels

Gerald S. Divaris

Sharon Parker Johnson

Herman Key, Jr.

Frank J. Quayle

Bry Phillips Taylor

D.P.O.R

.

Department of Professional and

Occupational Regulation

3600 West Broad Street

Richmond, VA 23230-4917

804-367-8500

D.P.O.R

Contact Person: Christine Martine, 804-

367-8552 www.dpor.virginia.gov

Licensing Section: 804-367-8526 www.state.va.us/dpor/reb

Licensing Fees

APPLICATIONS

Salesperson by education and examination $75.00

Salesperson by reciprocity $64.00

Business entity $75.00

Broker by education and examination $85.00

Broker by reciprocity $85.00

Broker concurrent $65.00

Firm $125.00

Branch Office $65.00

Transfer $35.00

Activate $35.00

TELEMARKETING

COLD-CALLING

ISSUE: In December of 2002, the FTC finalized amendments to the Telemarketing Sales Rule.

At the center of the changes is the creation of a national "do-not-call" registry. Real estate professionals must now refer to this list before engaging in cold calling and refrain from calling anyone who has placed their number on the list.

TELEMARKETING

COLD-CALLING

The registry will supplement the current company specific "do-not-call" list requirement. In a separate but similar effort, on

June 26, 2003, the Federal Communications

Commission (FCC) announced final amendments to their Telemarketing Rules that would among other things extend the National

Do-Not-Call provisions of the FTC rule to intrastate calls.

TELEMARKETING

COLD-CALLING

This is a significant change and as a result, all real estate professionals making interstate as well as intrastate calls must comply with the requirements of the National Do-Not-Call registry, regardless of state law exemptions.

TELEMARKETING

COLD-CALLING

STATUS/OUTLOOK: On March 23, 2004, the FTC published a final rule requiring telemarketers to scrub their call lists no more than thirty-one (31) days prior to the date any call is made. This would replace the FTC's current requirement to scrub their lists every three months.

Problems with Homeowners

Insurance - Overview

Homeowners insurance is the foundation for homeownership. Most homebuyers require a mortgage to purchase a home and mortgage lenders will not grant a loan without property insurance.

Problems with Homeowners

Insurance - Overview

The booming housing market and historically low interest rates have recently spurred many potential homebuyers into action. However, upon entry into the market many are faced with the grim reality of the decreasing availability and affordability of homeowners insurance.

What is happening?

Current conditions are that prices are up and underwriting standards are tight. Fortunately, one of those - underwriting standards - can be addressed. Several scenarios are emerging throughout the country with Virginia being no exception.

What is happening?

•

Unavailability . A homebuyer is unable to obtain homeowners coverage through traditional lines of insurance.

•

No renewal of an existing homeowners policy . At the time the policy is set to expire, an insurance company refuses to renew it due to the homeowner's filing of too many claims.

What is happening?

Cancellation shortly after closing . An insurance company issues a policy, the real estate transaction closes and the company later revokes it within the allowable time under state law. In Virginia an insurance company may cancel a policy for almost any reason within the first 90 days so long as they give the consumer 30 days notice of the cancellation.

What is happening?

Claims of a previous owner . An insurance company will deny coverage on a property to be purchased due to claims filed by a previous owner. This scenario is usually because the insurance company finds derogatory information in an insurance claims database after the fact and decides that the level of risk is too high.

What is happening?

"Zero-dollar" claims . "Zero-dollar" claims refer to things that did not result in a loss for the insurer being listed as a claim in an insurance claim database. Most insurance companies consult claim databases when making underwriting decisions. For example, a person could call their insurance company about possibly filing a claim and have it later count against them - regardless of whether a claim was ever actually filed.

What is happening?

Limited coverage in specific geographical regions . In various regions of the country some major insurance carriers have decided not to write any new homeowners policies indefinitely, which only makes things worse.

Taking into account the fact that many of these carriers service a large percentage of the marketplace, this shift has created a very difficult environment for those seeking to obtain new coverage.

What is happening?

The end result is that homebuyers trying to insure their new property are forced into very expensive plans that offer minimal coverage all because of the insurance company's perceived risk of loss. Other homeowners find their insurance company refusing to renew their existing policy due to prior claims. They are then left with very little time to find another policy - especially in today's insurance environment.