Managerial Accounting

by James Jiambalvo

Chapter 3:

Process Costing

Slides Prepared by:

Scott Peterson

Northern State

University

Objectives

1. Describe how products flow through

departments and how costs flow

through accounts.

2. Discuss the concept of an equivalent

unit.

3. Calculate the cost per equivalent unit.

4. Calculate the cost of goods completed

and the ending Work in Process

balance in a processing department.

5. Describe a production cost report.

Difference Between Job-Order

and Process Costing Systems

Job-Order Costing Systems assign costs

to heterogeneous jobs.

Process Costing Systems spread total

manufacturing costs over total,

homogenous, units produced.

Difference Between Job-Order

and Process Costing Systems

Product and Cost Flows

1. Product Flows Through Departments

2. Cost Flows Through Accounts

3. Conversion Costs

Product Flows Through

Departments

Cost Flows Through Accounts

Calculating Unit Cost

To compute unit costs it is first necessary

to compute Equivalent Units.

How Equivalent Units are

Calculated

Cost Per Equivalent Unit

Average unit cost in a Process Costing

System is calculated as follows:

Cost Per Equivalent Unit =

Cost in BWIP + Costs incurred currently

Units completed + Equivalent units in EWIP

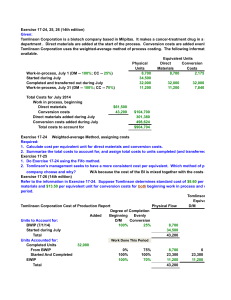

Calculating and Applying Cost

Per Equivalent Unit: Mixing

Department Example

Units:

BWIP:10,000 gallons, 80% complete labor/overhead

Started:70,000 gallons, 60,000 completed

EWIP:20,000 gallons, 50% complete.

Costs:

BWIP:$18,000 material, $7,800 labor, $23,400 overhead

Added:$142,000 of material, $62,200 labor

Overhead: applied at a predetermined rate of $3 per

dollar of labor or $186,600.

Calculating and Applying Cost

Per Equivalent Unit: Mixing

Department Example

Calculate: Cost per equivalent unit.

Answer: $6

Solution:

Material: $160,000/80,000=$2

Labor:

$ 70,000/70,000=$1

Overhead: $210,000/70,000=$2

Total Costs/Unit:

=$6

Calculating and Applying Cost

Per Equivalent Unit: Mixing

Department Example

Calculating and Applying Cost

Per Equivalent Unit: Mixing

Department Example

Calculating and Applying Cost

Per Equivalent Unit: Mixing

Department Example

Production Cost Report

Production Cost Report Contains:

1. Reconciliation of units.

2. Reconciliation of costs.

3. Details of the cost per equivalent unit

calculations.

Reconciliation of Units

BWIP + the number of units started = the

number of units completed EWIP.

Reconciliation of Costs

BWIP + costs added = costs transferred

out + EWIP.

Basic Steps in Process

Costing: A Summary

1. Account for the number of physical

units.

2. Calculate the cost per equivalent unit

for material, labor and overhead.

3. Assign cost to items completed and

items in EWIP.

4. Account for the amount of product

cost.

Dealing With Transferred-In

Costs

1. Process Costing Systems generally

use several processes; not just one.

2. Transferred-In costs are treated just

like other product costs (l.e. material,

labor and overhead).

3. Ultimately all costs, including those

transferred in, are transferred to

Finished Goods.

Process Costing and

Incremental Analysis

1. Decisions are based on costing

information obtained through Process

Costing Systems.

2. Incremental Analysis is frequently

used to make these decisions.

3. Be wary and recall that Process

Costing Systems capture both fixed

and variable costs.

Quick Review Question #1

1. The best example of a business

requiring a process costing system

would be a(n);

a. Soap manufacturer.

b. Automobile repair shop.

c. Custom cabinet shop.

d. Antique furniture restorer.

Quick Review Answer #1

1. The best example of a business

requiring a process costing system

would be a(n);

a. Soap manufacturer.

b. Automobile repair shop.

c. Custom cabinet shop.

d. Antique furniture restorer.

Quick Review Question #2

2. Costs in a process costing system are

ultimately traced to

a. Specific processes.

b. Specific customers.

c. Specific jobs.

d. Specific production personnel.

Quick Review Answer #2

2. Costs in a process costing system are

ultimately traced to

a. Specific processes.

b. Specific customers.

c. Specific jobs.

d. Specific production personnel.

Quick Review Question #3

3. BWIP consisted of 2,500 units, 100%

complete for materials and 60% for

conversion costs. 8,000 additional

units were started. 9,000 units were

completed and transferred out. How

many physical units are in EWIP?

a. 1,500.

b. 10,500.

c. 14,500.

d. 0.

Quick Review Answer #3

3. BWIP consisted of 2,500 units, 100%

complete for materials and 60% for

conversion costs. 8,000 additional

units were started. 9,000 units were

completed and transferred out. How

many physical units are in EWIP?

a. 1,500.

b. 10,500.

c. 14,500.

d. 0.

Quick Review Question #4

4. Using question #3 data, assume

ending inventory was 100% complete

for materials and 80% complete for

conversion costs? Calculate

equivalent units of production for

materials and conversion costs.

a. 6,500 & 6,500

b. 8,000 & 6,500

c. 8,000 & 8,700

d. 9,000 & 8,700

Quick Review Answer #4

4. Using question #3 data, assume

ending inventory was 100% complete

for materials and 80% complete for

conversion costs? Calculate

equivalent units of production for

materials and conversion costs.

a. 6,500 & 6,500

b. 8,000 & 6,500

c. 8,000 & 8,700

d. 9,000 & 8,700

Copyright

© 2004 John Wiley & Sons, Inc. All rights reserved.

Reproduction or translation of this work beyond that

permitted in Section 117 of the 1976 United States

Copyright Act without the express written permission of the

copyright owner is unlawful. Request for further information

should be addressed to the Permissions Department, John

Wiley & Sons, Inc. The purchaser may make back-up

copies for his/her own use only and not for distribution or

resale. The Publisher assumes no responsibility for errors,

omissions, or damages, caused by the use of these

programs or from the use of the information contained

herein.