legal entities for conducting business

advertisement

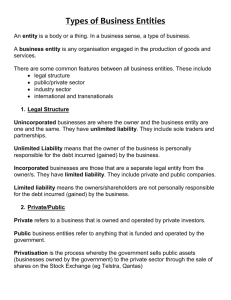

LEGAL ENTITIES FOR CONDUCTING BUSINESS JOHN S. HERBRAND, Esq. ONE CHASE SQUARE SUITE 1900 ROCHESTER, NEW YORK 14604 TEL: 585.295.1562 FAX: 585.325.6287 jsh@herbrandlaw.com The attached outline is a brief overview of certain business entities. In furnishing this outline, the author is providing information, not legal advice. Before choosing a business entity, you should seek advice from your attorney, accountant and other professionals. © 2004 John S. Herbrand, Esq. BUSINESS ENTITIES 1. 2. SOLE PROPRIETORSHIP PARTNERSHIP 3. CORPORATION 4. GENERAL LIMITED “C” corporation “S” corporation LIMITED LIABILITY COMPANY (LLC) © 2004 John S. Herbrand, Esq. FACTORS IN CHOOSING FORM OF BUSINESS ENTITY 1. 2. 3. 4. 5. 6. 7. 8. Liability of owners Number of owners Taxation of entity and owners Cost of formation of entity Cost of maintenance of entity Management and control of entity Financing of company Exit strategy Sale of business Retirement Estate issues © 2004 John S. Herbrand, Esq. SOLE PROPRIETORSHIP Single individual owning and operating a business ADVANTAGES: SIMPLE AND INEXPENSIVE TO FORM AND MAINTAIN PROFIT AND LOSSES PASS DIRECTLY TO OWNER DISADVANTAGES: UNLIMITED PERSONAL LIABILITY TERMINATION AT DEATH DIFFICULT TO TRANSFER INTEREST HOW TO START: OBTAIN ANY REQUIRED LICENSES FILE CERTIFICATE OF ASSUMED NAME IF NOT OPERATING UNDER OWN NAME FILE SS-4 WITH IRS FOR E.I.N. IF YOU WILL HAVE EMPLOYEES OBTAIN BUSINESS INSURANCES DESIRED © 2004 John S. Herbrand, Esq. GENERAL PARTNERSHIP A partnership is an association of two or more persons to carry on as co-owners a business for profit ADVANTAGES: FEW STATUTORY FORMALITIES INEXPENSIVE TO MAINTAIN PROFIT AND LOSSES PASS DIRECTLY TO OWNER DISADVANTAGES: WRITTEN AGREEMENT NOT NECESSARY ALL PARTNERS HAVE EQUAL VOICE AND ARE AGENTS OF THE PARTNERSHIP DIFFICULT TO TRANSFER INTEREST TERMINATION UPON DEATH OR WITHDRAWAL OF PARTNER UNLESS OTHERWISE PROVIDED IN PARTNERSHIP AGREEMENT UNLIMITED LIABILITY FOR ALL PARTNERS HOW TO START: ENTER INTO PARTNERSHIP AGREEMENT (NOT REQUIRED BUT STRONGLY ADVISED) FILE SS-4 WITH IRS FOR E.I.N. OBTAIN ANY REQUIRED LICENSES MUST FILE CERTIFICATE OF ASSUMED NAME OBTAIN BUSINESS INSURANCES DESIRED BEWARE of “CONSTRUCTIVE” PARTNERSHIPS! © 2004 John S. Herbrand, Esq. LIMITED PARTNERSHIP A limited partnership is a partnership formed by two or more persons under the provisions of the New York State Partnership Law, having as members one or more general partners and one or more limited partners. ADVANTAGES: FEW STATUTORY FORMALITIES INEXPENSIVE TO MAINTAIN PROFIT AND LOSSES PASS DIRECTLY TO OWNER LIMITED LIABILITY FOR LIMITED PARTNERS DISADVANTAGES: UNLIMITED LIABILITY FOR GENERAL PARTNERS LIMITED PARTNERS CANNOT TAKE PART IN MANAGEMENT OF BUSINESS EXPENSIVE TO FORM DIFFICULT TO TRANSFER INTEREST TERMINATION UPON DEATH OR WITHDRAWAL OF PARTNER UNLESS OTHERWISE PROVIDED IN PARTNERSHIP AGREEMENT UNLIMITED LIABILITY FOR ALL GENERAL PARTNERS HOW TO START: ENTER INTO LIMITED PARTNERSHIP AGREEMENT FILE CERTIFICATE OF LIMITED PARTNERSHIP PUBLISH NOTICE OF FORMATION CERTIFICATE OF ASSUMED NAME NOT REQUIRED UNLESS OPERATING UNDER DIFFERENT NAME FILE SS-4 WITH IRS FOR E.I.N. ESTABLISH SEPARATE BANKING AND ACCOUNTING OBTAIN ANY REQUIRED LICENSES OBTAIN BUSINESS INSURANCES DESIRED © 2004 John S. Herbrand, Esq. “C” CORPORATIONS A statutory legal entity which exists as a legal person separate and distinct from its shareholders ADVANTAGES: ENTITY SEPARATE AND DISTINCT FROM ITS SHAREHOLDERS PERPETUAL EXISTENCE LIMITED LIABILITY FOR SHAREHOLDERS EXCEPTIONS: PERSONAL GUARANTEES; 10 LARGEST SHAREHOLDERS LIABLE FOR UNPAID WAGES; RESPONSIBLE OFFICERS CAN BE LIABLE FOR UNPAID EMPLOYMENT AND SALES TAXES DIVISIBILITY AND TRANSFERABILITY OF INTERESTS FORMAL AND FAMILIAR STRUCTURE FOR BUSINESS OPERATIONS DISADVANTAGES: CORPORATE AND INDIVIDUAL LEVEL TAXES EXPENSIVE TO FORM AND MAINTAIN STATUTORY REQUIREMENTS MUST HONOR FORMALITIES ANNUAL STATE FRANCHISE TAX - $100 MINIMUM HOW TO START: FILE CERTIFICATE OF INCORPORATION OBTAIN CORPORATE “KIT” DRAFT AND ADOPT BY-LAWS ISSUE SHARES HOLD SHAREHOLDERS MEETING AND ELECT BOARD OF DIRECTORS HOLD DIRECTORS MEETING AND ELECT OFFICERS FILE SS-4 WITH IRS FOR E.I.N. ESTABLISH SEPARATE BANKING AND ACCOUNTING OBTAIN ANY REQUIRED LICENSES OBTAIN BUSINESS INSURANCES DESIRED © 2004 John S. Herbrand, Esq. “S” CORPORATIONS A statutory legal entity which exists as a legal person separate and distinct from its shareholders ADVANTAGES: SAME ADVANTAGES AS FOR “C” CORPORATIONS INDIVIDUAL LEVEL TAXES ONLY PROFIT AND LOSSES PASS DIRECTLY TO OWNER DISADVANTAGES: SAME DISADVANTAGES AS FOR “C” CORPORATIONS RESTRICTIONS ON TYPE AND NUMBER OF SHAREHOLDERS ONLY ONE CLASS OF SHAREHOLDER CANNOT HAVE ANOTHER CORPORATION AS SHAREHOLDER HOW TO START: SAME AS FOR “C” CORPORATIONS FILE FORM 2553 WITH IRS © 2004 John S. Herbrand, Esq. LIMITED LIABILITY COMPANIES An unincorporated statutory legal entity which exists as a legal person separate and distinct from its members ADVANTAGES: LIMITED LIABILITY FOR ALL MEMBER,INCLUDING MANAGERS PROFIT AND LOSSES PASS DIRECTLY TO OWNER IF SO ELECTED MULTIPLE CLASSES OF MEMBERSHIP PERMITTED NO RESTRICTIONS ON TYPES OR NUMBER OF MEMBERS PERPETUAL EXISTENCE UNLESS OTHERWISE AGREED DISADVANTAGES: EXPENSIVE TO FORM AND MAINTAIN NO EXTENSIVE BODY OF CASE LAW ANNUAL ASSESSMENT IN LIEU OF FRANCHISE TAX; MINIMUM $100 HOW TO START: FILE ARTICLES OF ORGANIZATION PUBLISH ARTICLES OF ORGANIZATION ENTER INTO OPERATING AGREEMENT OBTAIN LLC “KIT” FILE SS-4 WITH IRS FOR E.I.N. FILE FORM 8832 WITH IRS ESTABLISH SEPARATE BANKING AND ACCOUNTING OBTAIN ANY REQUIRED LICENSES OBTAIN BUSINESS INSURANCES DESIRED © 2004 John S. Herbrand, Esq. ALTERNATIVE TO STARTING A BUSINESS BUY A BUSINESS! ADVANTAGES: PROVEN TRACK RECORD EXISTING CUSTOMER BASE DISADVANTAGES: MORE COSTLY POTENTIAL ASSUMPTION OF UNKNOWN RISKS © 2004 John S. Herbrand, Esq. OTHER CONSIDERATIONS DOING BUSINESS IN OTHER STATES TRADE/SERVICE MARKS EMPLOYEE ISSUES © 2004 John S. Herbrand, Esq.