Chapter 2

STATEMENT OF CASH FLOWS

THE CONTENT AND VALUE OF THE STATEMENT OF CASH FLOWS

The cash flow statement reconciles beginning and ending cash by presenting the cash

receipts and cash disbursements of an enterprise for an accounting period. The receipts and

disbursements are segregated into three classes of activities. Cash receipts and disbursements

from operating activities report on the cash flows of the enterprise related to its business

operations. Cash receipts and disbursements from investing activities report on the cash flows of

the enterprise related to the acquisition and disposition of noncurrent assets. Cash receipts and

disbursements from financing activities report on the cash flows of the enterprise related to the

acquisition and repayment of debt and equity. The information contained in the statement is

useful to creditors and investors for the following reasons:

1. To assess the entity’s ability to generate cash flows in the future

2. The ability of the entity to pay dividends and meet its obligations

3. Reconciliation between net income in the income statement as net cash flow from

operating activities in the statement of cash flows.

4. To assess cash and noncash investing and financing activities of the entity during the

accounting period.

Classification of Cash Flows - There are three classifications of cash flows:

1. OPERATING ACTIVITIES

Cash receipts and disbursements are transactions that relate to net income. More

specifically these transactions relate to operating income. They include cash receipts from the

sale of products or services, the payment to vendors for inventory and the payment of salaries

and wages to employees.

2. INVESTING ACTIVITIES

Cash receipts and disbursements are transactions that relate to noncurrent assets. They

include the purchase and disposition of investments and long-lived assets and loans and

collection of loans to outside parties.

3. FINANCING ACTIVITIES

Cash receipts and disbursements are transactions that relate to long-term debt and

stockholders’ equity. They include borrowing cash from creditors and repayment of such loans

and the sale of capital stock and the payment of dividends and return of capital to equity

investors.

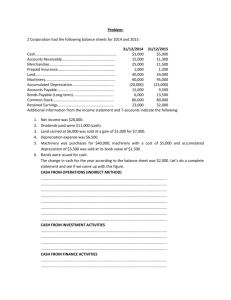

Exercise 1

Using the information below, to prepare a statement of cash flows for the December 31, 2012.

Cash

Accounts Receivables

Inventory

Prepaid expenses

Long-Term Investments

Land

Buildings and Equipment

Accumulated Depreciation

Accounts payable

Accrued Liabilities

Bonds Payable

Long-Term Note Payable

Common Share, RO.2 per share

Paid-in capital in Excess of Par value

Retained Earnings

2012 (RO.)

30,000

410,000

300,000

20,000

50,000

560,000

2,000,000

(800,000)

300,000

40,000

500,000

150,000

200,000

710,000

670,000

2011(RO.)

50,000

460,000

320,000

15,000

25,000

300,000

1,900,000

(770,000)

120,000

50,000

800,000

160,000

550,000

620,000

Additional Information about 2012 transactions:

1. Net income was RO. 110,000

2. Depreciation expense on buildings and equipment was RO.60,000

3. Sold equipment with a cost of RO. 50,000 and accumulated depreciation of RO.30,000

for cash of RO.17,000

4. Declared and paid cash dividends of RO.60,000

5. Issued a RO.150,000 long-term note payable for buildings and equipment.

6. Purchased long-term investments for RO.25,000

7. Paid RO.300,000 on the bonds payable

8. Issued 20,000 shares of RO.2 per value common share for RO.200,000

9. Purchased land for RO.260,000.

Exercise 2

Mars super market to find the cash flows for the year 31 December 2012 from following

information and the company have the cash balance for the year 2012 RO.33,750.

1. The company to purchase a machinery RO. 15,000 and the depreciation charged for six

months each are RO. 4,125 and RO.4,500.

2. The company to sale the old machinery RO.2,200 the original cost of the machinery is

RO.3,000.

3. The company paid dividend to the shareholders RO.21,125 for cash.

4. Purchases of buildings for office purpose RO.11,250 for cash.

5. Company to repay the long-term note RO.10,000.

6. Company to make a profit RO.3,750 for sale the investments worth RO.28,750.

Information below for current assets and liabilities,

Accounts receivable for the year 2011 RO.58,500 and 2012 RO.68250

Accrued payable for the year 2012 RO.3,375 and RO.2625 for 2011.

Inventory for the year 2012 and 2011 are RO.30,000 and 24,000 respectively.

Accounts payable for the year 2012 RO.35,000 and 2011 RO.24,750

During the year 2012 company earn RO.42,500 as a net profit.

Exercise 3

1. ABC Ltd cash flows for the year 31 December 2005 from following information and the

company have the cash balance for the year 2005 RO.25300.

Particulars

Accounts receivable

Accrued payable

Inventory

Accounts payable

Profit & Loss A/C

Additional information:

2004

43900

1900

22500

26000

25000

2005

51100

2500

18000

18500

31900

1. The company to purchase a machinery RO. 11,250 and the depreciation charged for six

months each are RO. 3,100 and RO.3,400.

2. The company decide to purchase of investments RO.6,500

3. The company to sale the old machinery RO.1,650 the original cost of the machinery is

RO.2,250 and purchase of machinery cost RO. 11,250

4. The company paid dividend to the shareholders RO.15,850 for cash.

5. Purchases of buildings for office purpose RO.8,500 for cash.

6. Company to repay the long-term note RO.7,500.

7. Company to make a profit RO.3,000 for sale the investments worth RO.21,500.

Exercise 4

Towell company cash flows for the year 31 December 2015 from following information and the

company have the cash balance for the year 2015 RO.1,100 and net income during the year RO.

810.

Particulars

Accounts receivable

Accrued liabilities

Inventory

Accounts payable

2014

1300

250

1900

800

2015

1750

200

1600

1200

Additional information:

1.

2.

3.

4.

5.

6.

Depreciation as on 31 December 2015 RO.30

To repay on bonds payable RO.250

Sale of investments RO.170 and RO.80 and gain from investments RO.80

Shareholders to get the dividends for investment RO.260

Purchase plant assets during the year 2015 RO.130

Company issue of shares RO.130 for improve the working capital.

0

0