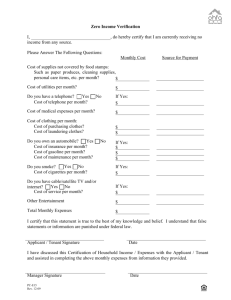

Checking_Account_files/Fiscal Fitness #1 Plan

advertisement

Capitate Your Kids Presents: Fiscal Fitness Program Families Learning About Money Together Mission Statement – Mission Statement: The Mission of the Fiscal Fitness Program is to create an integrated process of education about the use of money that involves young adults and parents. The goal will be to combine teaching sessions with hands-on practice using self-directed budgets, creating positive incentives for all parties. Becoming skillful at money is addressed so that we can get past money to what life is really about. Faithful use of our God-given resources will be our philosophical guide. What is the “Fiscal Fitness” Program About? 1. Learning about what it takes to make a plan for expenses. 2. Learning by doing in successive small steps. 3. Teaching sessions to go over core concepts like how to make a budget, how to balance a checkbook, where the best place is to get a loan, how to keep money safe……. 4. Writing an agreement, or a “contract” between parents and young adults to give control of personal budgets to young adults. 5. Young adults make their own choices and have control over their own decisions, retaining any leftovers when they do a good job. (Mistakes go away! They simply become decisions and consequences based on personal choices.) 6. And when young adults do a great job with money, they have resources from their budget for personal choices. 7. You will learn how to manage a checking account. Deposits, fees, balancing. The works. Your OWN checking account. 8. After learning budgets and contracts, we will move on to more complicated topics like credit ratings, and the hidden costs of bad credit…. 9. Each month, each young adult will review their budget with an adult who is not their parent. 10. And we don’t compare family to family: we’ll always respect each family’s privacy. Each person’s budget is private. 11. The purpose of getting good at money is to get PAST materialism to what life is really about: loving and lasting relationships, contributing meaningfully, giving something back to your community. Schedule: Goal: We will meet once a month for 90 minutes. Suggest: Third Sunday of each month: 530 pm. We will meet for 4 months. 1. Session One: ___________ 2. Session Two: ___________ 3. Session Three: ___________ 4. Session Four: ____________ A. Planning and Budgets “Most people don’t plan to fail, they just fail to plan.” Most millionaires in America spend more time thinking about and planning about money than people with no net worth. This comes down to simple consistent behaviors. Tracking expenses, balancing a checking account Measuring whether you are “gaining or losing” each month are the behaviors that result in knowing how you are doing. Want to be a millionaire? Start acting like one. Fiscal Fitness Rule #1. A rich life is a life of freedom to make your own choices. Happiness doesn’t necessarily come from being monetarily rich, but from being in control and knowing how to solve problems. Our materialistic society tempts you to get stuck on money, and life is about more than that. Let’s talk about Plans and Planning What are Your Plans? Do you plan to finish Marquette? Why? Do you plan to go to college?Why? (Hint: 70%) Have you thought about how you are going to pay for college? Have you ever thought of having your own plan? HOMEWORK: We want you to write down your plan for this year with your parents. 2. How do we all learn to plan? All learning has three components: a. Taking small steps b. Repeating the process frequently (Daily basis) c. Getting rewards for accomplishing the steps Examples of things that were hard that you have learned to do?….. Fiscal Fitness Rule #2. We all need to make plans our lives. It’s more than just money. Write down your plans. Save them. Pin them on your bulletin board or fridge Act on them Yes, you are planning to go to college.. 3. Solving Financial Problems What is the Difference Between Broke and Poor? They both sound the same but we are going to claim they aren’t. We will suggest: poor is a state of mind in which you have given up and have no plan to get out of it Being broke: state of mind in which you are determined to get out of being broke. Both situations have a lousy bank balance Someone who’s broke has a PLAN What will our lessons be? We are going to learn by doing. You figure out what challenges you want to address and to solve. We will show you tools on how to solve those challenges. We will teach you how to fix being broke: “If you’re broke, FIX IT” Fiscal Fitness Rule # 3 You must learn to solve money problems with as much seriousness as AP Chemistry To learn control over financial affairs, you need to have a chance to solve your own problems by yourself, and understand the steps you went through to create those solutions. What are the steps? What is a budget? A budget is a fixed amount of money assigned to a certain purpose. No one does this very well Your personal budget is what is already being spent on you Do you know how much your parents spend on your expenses? What is in your budget? First step is to break all your expenses in to categories For the sake of this lesson, let’s make the first category “Clothes” Let’s break down clothes to types of clothes Can you list 10 types of clothes? List of Types of Clothes 1. Pants 2. Shirts 3. Sweatshirts 4. Coats 5. Shoes 6. Boots 7. Dress up clothes 8. Swimming and summer wear 9. _______________ 10. ______________ How do you know how much these clothes cost? The same clothes can cost very different amounts? How much do jeans cost at Abercrombie? How much do jeans cost at Kohls? What do jeans cost at Walmart? Can you tell them apart at 20 yards? Does anyone of them last longer? How far are you in your budget? This is where most people break down because we don’t really know what we are spending…..we just sort of spend it A better way to make a budget? Track expenses That’s what we are going to do (Pass out Budget Books) Open the Budget Book On Page One write your name and put CLOTHES on the top of the main area Page Two: What’s another category that your parents are spending on you? Sports equipment Transportation School Supplies Holiday gifts Parties Pocket money or allowance? “Fiscally Fit Families are Fair” Yes, we really mean every penny your parents spend on your behalf. We want to keep track so that when you get your budget, it’s absolutely fair! You get to control what your parents would have spent on you anyways. That way both sides win. You get control and choices, and learn how Parents get to see you do a good job and don’t have to sweat the small details. And in the end, you get the leftovers when you do a good job To Review The Purpose of this course is to create a budget for you that is accurate and fair Teaching you how to run an adult budget starts with practicing on your own Planning and goal setting are partners to making a budget and living in it You are planning to succeed, we want to teach you the means by which you will A Plan to Get Ahead: Has to Include Learning now to…… Save money! Research shows that the most effective way to get people to save is to create a discipline about allocating your money. Whenever you get a paycheck, put 10% of it away and learn to live on the remainder For every dollar you save, you will be paid back a nickel (maybe more) every year for the rest of your life. That way, money works for you, not you for money. Why do we need to learn to save? It’s all tied up in how long you are going to live, and what you can expect to live on when you stop working? How long will you live? __________ And, when are you likely to retire from working? ________ Subtract: That’s how long you have to support yourself for. Fiscal Fitness Rule # 6 Pay yourself first. Fiscal Fitness Rule # 7 Make money work for you. Do not be a borrower. “Know the spread”. What’s the difference between borrowing and lending money When you borrow, you are paying someone else the interest…. About 6-12% When you are saving, or lending, you get paid the current rate of saving…. About 2-6% The Spread: Is the full difference between borrowing and lending Time Value of Money What do investments do over time? They grow by COMPOUNDING Compound interest, according to Einstein is, “one of the greatest Miracles of the Modern Age”. Pop Quiz on Saving Who makes more money? Someone who saves $ 1000 a year from age 16 to age 25 (Total $ 10,000). and then stops, or someone who saves $ 1000 a year from age 26 till age 50? Both saved $25,000 At 8% interest: $ 131.050 vs $ 84,701 Rule of 72: This is a simple rule to know and gives you a close guess to how fast money grows. Divide 72 by the interest rate you are getting, and it tells roughly how long it will take to double your money. If you are getting 2%, how many years to double? If you were getting 9% interest? How long to double? 8 years Saving vs Investing. Saving is usually short term, in a bank. Something you need soon. You usually save money in the form of CASH. You save money and set it aside for use in the near future It has a problem: INFLATION •What’s Inflation? Inflation is the gradual rise of prices Gradual Rise of Prices What does a gallon of gas cost today? What was it a year ago? $ 1.32 I don’t remember a $ 1.32 The lesson to be learned: Money has a time component to it. Inflation is the gradual rise of prices that shows just why money can’t stand still. Investing versus Saving Saving usually means placing cash in a bank: very secure, safe and proper for … SHORT TERM goals: like saving for college or something else you will need in the next three years. Just keeps pace with inflation Investing is riskier. You put your money into stocks. They go up and down. But on average, they return about 9 % a year Types of Saving Methods Savings account in a bank: 2 % A CD: A Certificate of Deposit. You promise the bank they can have your money for at least 6 months…… 3-4% Savings Bond: You give the government your money for 5 years…… 5% Money Market Account: riskier, rates go up and down Types of Investing Buy stocks - shares of a company and get a stock certificate. Put the certificate in your safety deposit box. Buy stocks but keep them at the broker in an account called a brokerage account Buy a mutual fund: a collection of stocks Tax Advantaged Investing You can get huge benefits by saving free of some taxes by.. Saving in an Individual Retirement Account: an IRA. The best deal on the planet. Make sure you save some money every year in your IRA Signing up for an account called a 401K when you get a job. Your employer will match your first couple of percent donations, but only if you save if out of your paycheck first. That means a 100% instant return on savings! Start the Savings Habit Lots of little ways to do it that add up to huge savings Pay Yourself First. (FF Rule #6) Catch Your Coins Bank Your Surprises Protect Yourself from Surprises Rainy day fund A couple months of living expenses Saves having to borrow at huge cost when your car transmission goes out or you get laid off, (Or break a leg) You will need this 3-4 times in your life and can’t imagine how much you appreciate it until you get there. Quiz for Success…. Do you have written goals? Do you save some money regularly? Do you have a budget? Do you pay what you owe promptly? Do you think ahead before you buy? Do you buy only what you need and will use? Do you P. Y. F.? Summary People who succeed, plan You can start learning to plan by making a plan for this year Learning about money is learning to plan your goals and activities Because you put your money where your values and goals are A budget is how you show your plan Learning to save is part of your plan Pay yourself first Homework Keep track of every expense you make this month Write it in your budget book Separate out categories from each other: clothes, sports equipment…… Write out a plan for this year for yourselves. Start with example in handout. Parents Homework See budget sheet for food expenses Write down your personal estimate of what you think you spend for your families food Keep track this month of every expense you incur for feeding your family Show your young adult that you are learning from this course too It’s in the journey together that we learn the most. The Savings Game Einstein Called the power of compound interest one of the miracles of our age. Start with one dollar in a jar Each day, calculate 10% return on your investment Write it down on the sheet Next month: 28 days from now, we will see what your money has grown to!