The basics of credit reporting

© 2011 Experian Information Solutions, Inc. All rights reserved. Experian and the marks used herein are service marks or registered trademarks of Experian Information Solutions, Inc.

Other product and company names mentioned herein are the trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified,

or distributed in any form or manner without the prior written permission of Experian.

© 2011 Experian Information Solutions, Inc. All rights reserved.

2

The Fair Credit Reporting Act

Credit reporting companies are governed by the

Fair Credit Reporting Act (FCRA) enacted in 1970,

revised effective October 1997, amended December

2003 by the Fair and Accurate Credit Transaction Act

(FACT Act)

© 2011 Experian Information Solutions, Inc. All rights reserved.

3

The benefits of credit reporting

Credit reporting companies serve consumers

and businesses by making possible:

►

Instant credit

►

Lower-cost credit

►

Nationwide credit

►

Widespread availability

►

Account management

© 2011 Experian Information Solutions, Inc. All rights reserved.

4

The three national credit reporting companies

Experian

Equifax

Trans Union

There are some independent

local or regional credit bureaus

that provide direct consumer

assistance but whose data

resides with one of the national

credit reporting companies

© 2011 Experian Information Solutions, Inc. All rights reserved.

6

Requesting your personal report

Experian

1 888 397 3742

www.experian.com

Equifax

P.O. Box 740241

Atlanta, GA 30374-0241

1 800 685 1111

Trans Union

P.O. Box 1000

Chester, PA 19022

1 800 888 4213

© 2011 Experian Information Solutions, Inc. All rights reserved.

7

Sources of reports for consumers

Consumer reporting companies

►

Referred by adverse action notices

►

Fraud

►

Unemployed and seeking employment

►

Receiving welfare assistance

►

Free reports under some state laws

►

Purchase additional reports

FACT Act Centralized Source

Consumer direct services

© 2011 Experian Information Solutions, Inc. All rights reserved.

8

Centralized source for free reports

www.annualcreditreport.com

One every twelve months

Single contact point

►

Telephone - 877 322 8228

►

Mail

►

Internet

Fee for credit score disclosure

© 2011 Experian Information Solutions, Inc. All rights reserved.

9

The credit cycle

You pay lender

Credit

reporting

companies

share

with new

lenders

Lender

updates

records

Lender shares history with

credit reporting companies

© 2011 Experian Information Solutions, Inc. All rights reserved.

10

Credit reporting companies are like libraries

Credit reporting company clients check out information …

… If they have a permissible purpose under the law

© 2011 Experian Information Solutions, Inc. All rights reserved.

11

The Fair Credit Reporting Act

Permissible purposes

Open or manage credit accounts

Offers of credit

Employment purposes

Underwrite insurance

A business transaction initiated by the consumer

Court order or federal jury subpoena

Valuation of risk of an investor

Eligibility for government license

Disclosure to consumer

© 2011 Experian Information Solutions, Inc. All rights reserved.

12

The players in the credit cycle

You

Credit reporting companies

Lenders

Risk score modelers

The government

© 2011 Experian Information Solutions, Inc. All rights reserved.

13

Information comes from you

Credit Application

Jonathan Q. Consumer

999-99-9990

10655 Birch St.

Burbank CA 91502

Information you provide in an

application for credit, housing, or

insurance is reported to credit

reporting companies

© 2011 Experian Information Solutions, Inc. All rights reserved.

14

Information comes from you

© 2011 Experian Information Solutions, Inc. All rights reserved.

15

What’s in a credit report?

Identifying information

Account information

Public record information

Inquiries

Dispute instructions

© 2011 Experian Information Solutions, Inc. All rights reserved.

16

© 2011 Experian Information Solutions, Inc. All rights reserved.

17

An important note about inquiries

There are two different types of inquires:

►

Inquiries shown to potential creditors

►

Inquiries shown only to the consumer

© 2011 Experian Information Solutions, Inc. All rights reserved.

18

How long is information retained?

Open accounts in good standing

Closed accounts in good standing

Indefinitely

10 years

Late or missed payments

7 years

Collection accounts

7 years

Civil judgments

7 years

Chapter 7 bankruptcy

10 years

Chapter 13 bankruptcy

7 years

Unpaid tax liens

10 years

Paid tax liens

7 years

Credit inquiries

2 years

© 2011 Experian Information Solutions, Inc. All rights reserved.

19

What’s NOT in a credit report?

Credit reporting companies do not store:

►

Criminal background

►

Medical information

►

Buying habits / transaction data

►

Bank account information

►

Credit risk scores

© 2011 Experian Information Solutions, Inc. All rights reserved.

20

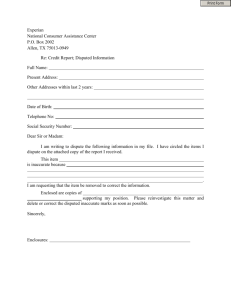

Initiating a dispute

Must get report directly from Experian

►

►

►

Toll-free number on report gives you access

to customer service

Report number identifies you and your record

You and customer service representative

will be looking at the same information

in the same order

Can dispute online, by telephone or by mail

Dispute must be specific

© 2011 Experian Information Solutions, Inc. All rights reserved.

21

Processing a dispute

Credit reporting company verifies with the source of the information (creditor

or court)

Must allow up to 30 days for processing

Source verifies, corrects or updates

Secure electronic mail system is used

Creditors required to report corrections

to all databases

Consumer can add statement of dispute

if issue is not resolved with source

© 2011 Experian Information Solutions, Inc. All rights reserved.

22

Beware of credit repair companies

Can’t legally do anything you can do for free

Can’t legally collect fee before delivering the promised service

Can’t legally advise you to lie about your accounts or about your identifying

information

© 2011 Experian Information Solutions, Inc. All rights reserved.

23

Common myths about credit reporting

When paid, the bad debt will go away

The credit reporting company denied me credit

I’m not responsible for those charges on our account

A divorce decree separates joint accounts

Consumers must give their permission for a report to be issued (employment

is the exception)

Requesting your own report and preapproved offers harm

your credit history

There is only one credit risk score and it is on every report

© 2011 Experian Information Solutions, Inc. All rights reserved.

24

Automated credit risk scoring

Used instead of a manual “score sheet”

Valuable risk management tool

Many different models available from many

different sources

Credit reporting companies often apply the model

selected by the creditor when delivering the

credit report; however, the credit scoring model,

or formula, is proprietary to the developer and

is not known by the credit reporting company

© 2011 Experian Information Solutions, Inc. All rights reserved.

25

Risk factors are the key

Generated when a risk score is calculated

Tell the consumer what to address in their

credit history to become more creditworthy

Are largely consistent from model to model

Are usually included in or described

in an adverse action notice

Experian provides both positive and

negative factors to consumers with

scores it provides through its

direct-to-consumer services

© 2011 Experian Information Solutions, Inc. All rights reserved.

26

Mortgage and auto loan inquiries

Credit scoring systems recognize multiple

inquiries may be made for a single mortgage

or auto loan and adjust for that type activity

For example, in many models inquiries

for those purposes are counted as a single

inquiry within any rolling 14-day period,

minimizing or eliminating any impact

on credit scores

© 2011 Experian Information Solutions, Inc. All rights reserved.

27

There is no silver bullet

You can’t “fix” the number

Address the risk factors in your

credit management and every

risk score will improve

Time is the key

© 2011 Experian Information Solutions, Inc. All rights reserved.

28

Resources

Free annual FACT Act credit report

www.AnnualCreditReport.com

Access to free report from each of the three credit reporting

companies

Experian

www.Experian.com credit education

Ask Max advice column, sample consumer report, frequently asked

questions

Experian Credit Educator: 877-901-6909

Personalized review and guidance about your credit report and score

by an Experian professional for a nominal fee.

www.FreeCreditScore.com

Access to credit monitoring and unlimited Experian credit reports and

scores

www.VantageScore.experian.com

Purchase a scored report and learn about scores

www.LowerMyBills.com

Free online service for consumers to compare low rates on monthly

bills and reduce the cost of living

www.PriceGrabber.com

Free online comparison shopping service to help consumers find

lowest prices for goods and services

www.ClassesUSA.com

Assistance in locating college education resources

www.AutoCheck.com

Vehicle history reports to help consumers ensure they make good preowned auto purchasing decisions

© 2011 Experian Information Solutions, Inc. All rights reserved.

Education partners

►

www.lifesmarts.org

►

www.jumpstart.org

29

© 2011 Experian Information Solutions, Inc. All rights reserved.