Name Block ______ Date ______ Perfect competition scramble! AP

advertisement

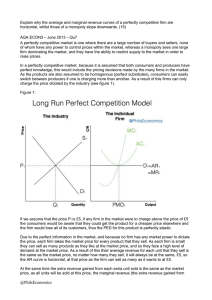

Name ______________________________________________________ Block ____________ Date ___________ Perfect competition scramble! AP Microeconomics / I meant to give you a review worksheet with a perfectly graphed model of a perfectly competitive market and firm in equilibrium (e.g., making zero economic profit), but as you can see, I jumbled it all up. Can you unscramble the labels and curves? Ignore average variable costs for now. Labels: P P Q Q Market MR ATC MC PM QM PF Firm S QF AR=P D D MC Curves: After you’re finished graphing, please answer: 1) Under perfect competition: How many markets are there? How many firms? 2) What is an example of a good that is typically produced under perfect competition? 3) Why do we graph the market and firm behavior separately? 4) What is always the relationship between PM and PF? 5) What is the profit maximizing rule (e.g., how do firms choose the quantity to produce)? 6) Why is demand in the market downward sloping, but for the firm it is the same at any quantity? 7) If demand in the market goes up, driving the market price up, what happens to the firm’s quantity produced? The firm’s profit? 8) Show the scenario in number 7 (increase in PM) on the graph, and shade in the profit rectangle. Monopoly Mayhem! 1. Under monopoly conditions, what do we know about… The number of firms? Product differentiation? Barriers to entry? Market power? 2. What is the relationship between the market and the firm? 3. Prove that MR is not equal to D anymore. Complete the chart below on a pure monopoly and graph it. Price Quantity 1 Total Revenue 60 Marginal Revenue 60 60 50 2 100 40 40 3 120 20 30 4 120 0 20 5 100 -20 10 6 60 -40 4. Complete the table below and add in the firm’s MC and ATC curves on the graph above: Quantity Total Cost 40 Marginal Cost 40 Average Total Cost 40 1 2 65 25 32.5 3 85 20 28.3 4 120 35 30 5 175 55 35 6 255 80 42.5 5. What profit-maximizing quantity should this pure monopolist produce? 6. What profit-maximizing price should the monopolist charge? 7. What is the firm’s profit or loss? 8. Do you think the monopolist’s profit or loss will change in the long run? Why or why not? 9. In a perfectly competitive market, equilibrium would be where supply (MC) is equal to demand (MB). In this case, P=MC, which is our definition of allocative efficiency. Sadly, an unregulated monopoly is not allocatively efficient, since the price is greater than MC. Show the market failure by identifying the area of deadweight loss on the graph above. Do your best to think it through. 10. In what way(s) do you anticipate the government could correct for market failure in this situation?