2-2 - United Nations Statistics Division

advertisement

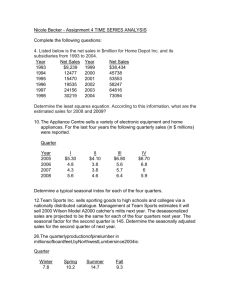

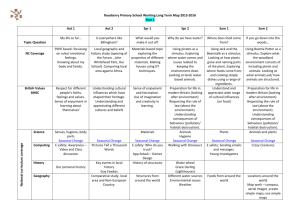

Seasonal adjustment Training Workshop on the Compilation of Quarterly National Accounts for Economic Cooperation Organization Member Countries 8-11 March 2015 Tehran, Islamic Republic of Iran United Nations Statistics Division Outline What is time series? Components of time series What is seasonal adjustment? Seasonal adjustment models Seasonal adjustment methods Issues in seasonal adjustment Conclusions Questions 2 What is time series? Is a series of data obtained through repeated measurement of the same concept over time that allows different periods to be compared Examples: • • • • QNA Monthly index of industrial production Monthly consumer price index Monthly retail sales Data which are collected only once or irregularly are not considered as time series 3 What is time series? Example of time series data Source: IMF QNA Manual (2001) 4 Components of time series Trend cycle component Captures long-term trend and business cycle movements in the data • Long-trend trend is associated with structural changes • Population growth Progress in technology and productivity Business cycle movements are related to periodic oscillations of different phases of the economy Recession Recovery Growth Decline 5 Components of time series Seasonal component Stable seasonal effects in terms of annual timing, direction and magnitude • Could be due to climatic factors, administrative or legal rules, social/cultural traditions and conventions, and calendar effects that are stable in annual timing Example: Public holidays such as Christmas Calendar-related systematic effects that are not stable in annual timing, and due to • • • Trading-day or working-day effect Moving holiday effect, for example, Ramadan, Chinese New Year Leap year effect 6 Components of time series Irregular component Captures effects that are unpredictable in terms of timing, impact and duration unless additional information is available Includes outlier effects which cause abrupt changes in the series, sometimes related to unexpected events such as • • • • Unseasonable weather Natural disasters Strikes Economic and financial crisis 7 What is seasonal adjustment? Seasonal adjustment means using analytical techniques to break down a series into its components The purpose is to identify the different components of the time series and thus provide a better understanding of the behaviour of the series to • • • Aid in short-term forecasting and modelling Remove regular within-a-year seasonal patterns to highlight the underlying trends and short-run movements in the series Allow series to be compared from quarter to quarter 8 Seasonal adjustment models Most common forms of decomposition • Additive: Yt = Tt + St + It • Multiplicative: Yt = Tt x St x It where Yt = Observed time series at time t Tt = Trend-cycle component at time t St = Seasonal component at time t It = Irregular component at time t 9 Seasonal adjustment models Additive model assumptions • • The components of the series are independent of each other The size of the seasonal oscillations is independent of the level of the series Multiplicative model assumptions • • The components of the series are dependent on each other The size of the seasonal oscillations increases and decreases with the level of the series 10 Seasonal adjustment methods Moving average-based methods Model-based methods Integrated methods 11 Seasonal adjustment methods Moving average-based methods Are based on the use of different kinds of moving average filter Best example is the X-11 family • • • US Bureau of Census developed X-11 in the 1960s Statistics Canada developed X-11-ARIMA US Bureau of Censes developed X-12-ARIMA in the 1980s All X-11 family involve repeated application of suitable moving average filters to decompose the time series into its trend-cycle, seasonal and irregular components 12 Seasonal adjustment methods Moving average-based methods Main steps of X-12-ARIMA program: • • • The series is pre-adjusted using the regARIMA model to detect and remove outliers and other distorting effects such as calendar effects and to extend the series with backcasts and forecasts to be used in the decomposition process The pre-adjusted series is then decomposed through three rounds of seasonal filtering and extreme value adjustments to produce the trend-cycle, seasonal and irregular components Various diagnostics and quality control statistics are computed, tabulated and graphed 13 Seasonal adjustment methods Moving average-based methods Main elements of X-12-ARIMA seasonal adjustment program 14 Seasonal adjustment methods Model-based methods Estimate the trend-cycle, seasonal and irregular components with signal extraction techniques applied to an ARIMA model fitted to the unadjusted data TRAMO/SEATS is most widely used • • Developed at the Bank of Spain Consists of two main programs • Time series regression with ARIMA noise, missing observations and outliers (TRAMO), a regARIMA modeling package with automatic identification of ARIMA models, outliers and other components Signal extraction in ARIMA time series (SEATS), which takes modeling results from TRAMO and performs a model-based signal extraction Both programs are structured to be used together TRAMO pre-adjusts the series before seasonal adjustment by 15 SEATS Seasonal adjustment methods Integrated methods X-13-ARIMA-SEATS • • • Was recently released by US Bureau of Census Implements the X-11 method and SEATS method Allows comparison of X-11 and SEATS seasonal adjustment using a common set of diagnostics DEMETRA+ • • • • Was developed by Eurostat Offers choice of X-12-ARIMA and TRAMO/SEATS Provides user-friendly tools to check quality of results Allows multi-processing 16 Seasonal adjustment methods Example of seasonally adjusted series, trend-cycle and irregular components Source: IMF QNA Manual (2001) 17 Issues in seasonal adjustment Direct vs indirect seasonal adjustment Relationship among price, volume and value Temporal consistency with annual accounts Length of series for seasonal adjustment Seasonal adjustment of indicators or QNA series Organizing seasonal adjustment in the QNA Presentation of seasonally-adjusted estimates 18 Issues in seasonal adjustment Direct vs indirect seasonal adjustment Seasonally adjusted series of aggregates can be derived by • • Directly adjusting the aggregates, or Indirectly by aggregating seasonally adjusted data of the components Both approaches have merits Direct approach • • May result in improved quality of seasonally adjusted series May give best results if the component series show similar seasonal patterns and trend cycles are highly correlated 19 Issues in seasonal adjustment Direct vs indirect seasonal adjustment Indirect approach • • • • May give best results when the component series show different seasonal patterns May make it easier to identify breaks, outliers, calendar effects, etc, in detailed series May give better results for balancing items (for example, value added) if component series are available May, however, leave residual seasonality in the aggregates Country practices vary Choice may be guided by expected uses of the seasonally adjusted data 20 Issues in seasonal adjustment Relationship among price, volume and value Seasonally adjusted price indices, volume measures and current price data can be derived • • Independently, or By seasonally adjusting 2 of them and deriving the third residually Either approach will give different results Choosing which series to derive residually should be determined on a case-by-case basis, depending on which approach produces the most reasonable results 21 Issues in seasonal adjustment Temporal consistency with annual accounts Annual totals based on seasonally adjusted data and unadjusted data will not be automatically equal due mainly to calendar effects and moving seasonality If effects are strong, seasonally adjusted data should be benchmarked to the calendar adjusted annual data 22 Issues in seasonal adjustment Length of series for seasonal adjustment Seasonal adjustment requires sufficiently long time series to ensure results with sufficient quality For QNA variables, at least 5 years (20 quarters) of data should be used When starting a new QNA system, unadjusted data should be reconstructed as far back as possible before doing seasonal adjustment 23 Issues in seasonal adjustment Length of series for seasonal adjustment Sometimes, seasonal adjustment may return questionable results for very long time series • Reasons • Discontinuities and structural breaks due to different economic conditions over a long period of time Solution Divide the series into 2 or more contiguous relatively stable periods Apply seasonal adjustment to each sub-period separately Link the resulting seasonally-adjusted series 24 Issues in seasonal adjustment Seasonal adjustment of indicators or QNA series Seasonally adjusted QNA can be obtained by • • Using seasonally adjusted indicators, or Applying the chosen seasonal adjustment method to the unadjusted QNA Both approaches have merits Applying seasonal adjustment directly to indicators • • Means correcting seasonal effects at the actual data sources May avoid artificial seasonality due to use of QNA techniques such as benchmarking 25 Issues in seasonal adjustment Seasonal adjustment of indicators or QNA series Seasonally adjusting the QNA • • Has the advantage of ensuring the unadjusted QNA is consistent with other variables Ensures high degree of consistency in the seasonality of production, expenditure and income components of GDP 26 Issues in seasonal adjustment Organizing seasonal adjustment in the QNA Seasonal adjustment programs offer automatic selection procedures that produce satisfactory results for most time series, with little intervention from users Some series may be problematic with substantial experience and expertise is needed to check whether seasonal adjustment is done properly or fine tune options General recommendation is for statisticians who compile the statistics to seasonally adjust the series, either solely or together with specialists A small unit of seasonal adjustment experts should also be set up to handle problematic series 27 Issues in seasonal adjustment Presentation of seasonally-adjusted estimates Seasonally-adjusted QNA estimates can be used to calculate • • Quarter-to-quarter rates of change Annualized quarterly rates of change Whatever growth rates that are published should be clearly indicated The levels of seasonally-adjusted QNA estimates can be annualized • Not recommended as presentation Seems artificial Is not easy to interpret 28 Conclusions Seasonally adjusted QNA estimates should be calculated to facilitate the analysis of current economic developments without the influence of seasonal and calendar effects Seasonally adjusted data should, however, not replace the unadjusted QNA data There are a number of methods to do seasonal adjustment The choice of which seasonal adjustment method to use can be based on past experience, subjective appreciation and characteristics of the time series A minimum of 5 years (20 quarters) data is needed to seasonally adjust QNA data. Metadata and methodological notes on seasonal adjustment methods should be made available for transparency 29 Questions Is your country compiling and publishing seasonally-adjusted QNA? • • If yes, what method and software are you using to do seasonal adjustment? If not, do you have plans to do so? Is there a specific unit doing seasonal adjustment or is it done by the unit compiling QNA? Is the method to do seasonal adjustment published in your national accounts methodological notes? 30 Thank you 31