How Prices are Determined

advertisement

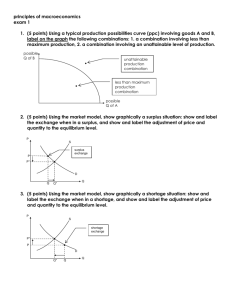

How Prices are Determined Prices play an important role in our economy. Everyone who participates in the economy jointly determines prices. Prices are considered neutral and impartial. The Adjustment Process Buyers and sellers have exactly the opposite hopes and intentions. Buyers want good buys at low prices. Sellers want high prices and profits. The Adjustment Process To understand how prices are set, we can look at a new product, called a gadget , being introduced. Because it’s new, producers can’t be sure what to charge for it. An adjustment process takes place. To demonstrate how prices are set, economists use an economic model, a set of assumptions listed as a table, graph, or equation. The Supply and Demand Schedule for Gadgets Market Equilibrium The adjustment process moves toward market equilibrium – a situation where prices are stable and the quantity supplied is equal to the quantity demanded. Market Equilibrium Why does the market find the equilibrium price of $5 on its own and why is the quantity supplied exactly equal to the quantity demanded at this price? Why did the price not reach equilibrium at $7, or $6, or at some other price? In order to answer these questions, we have to examine the reactions of the buyers and sellers to various market prices. Surplus If suppliers guess that the price will be $7, they will want to produce 1400 gadgets. However, consumers will only buy 990 units at at a price of $7, leaving a surplus of 410 gadgets. Surplus A Surplus is a situation in which the quantity supplied is greater than the quantity demanded at a given price. A surplus causes prices to go down, the quantity demanded to rise, and the quantity supplied to go down. As long as price is flexible, the surplus will only be temporary. Shortage If $7 is too high, producers might consider $4. At that price, the quantity supplied changes to 1,250 gadgets. However, at $4, consumers would buy 1,470 gadgets , resulting in a shortage of 220. Shortage A shortage is a situation in which the quantity demanded is greater than the quantity supplied at a given price. A shortage causes prices to go up and the quantity supplied to increase. Price Adjustment We can assume that the next price will be less than $7, which we already know is too high. If the new price is $6, a surplus of 210 will result. The surplus will cause the price to drop but probably not below $4 which already proved to be too low. Equilibrium Price When the price drops to $5, the market finds its equilibrium price. The equilibrium price is the price where quantity supplied equals the quantity demanded, - there is neither a surplus nor a shortage. The equilibrium price will maintain until something disturbs the market. Equilibrium Price This theory is set in ideal conditions. Price represents the balancing forces of demand and supply. The great advantage of competitive markets is that they allocate resources efficiently. As sellers compete to meet consumer demands, they are forced to lower costs and prices. At the same time, competition among buyers helps prevent prices from falling too far, and helps allocate goods and serves to those willing and able to pay. Price Adjustment Bookstores and other businesses often price certain goods below cost to attract customers. What may result if the price for a given product is set too low? Loss Leader Fixed Prices Up to now, we have assumed that the market was reasonably competitive, and that prices and quantities were allowed to fluctuate. What happens when government policies fix the prices people either receive or pay? Fixed Prices Some cities, especially New York City, have experimented with rent controls to make housing more affordable. When rents are capped at artificially low rates, housing shortages usually result. Fixed Prices Price ceilings set the maximum legal price that can be charged for a product. This often creates a shortage. Who would love the lower price? Who would not? Fixed Prices Occasionally, prices are considered too low, and some people believe they should be kept higher. The minimum wage, the lowest legal wage that can be paid to most workers, is a case in point. Fixed Prices Price floors set the lowest legal price that can be paid for a good or service. This often leads to a surplus. Is the current minimum wage higher or lower than the wage that would prevail in its absence? Do you think that your employer would pay you less if he or she were allowed to do so? Assignment!! Construct demand and supply schedules and an economic model for a brand of blue jeans, using the information below. Then show at what prices surpluses, shortages, and price equilibrium appear. Price Demand Supply $22 60,000 20,000 $24 50,000 28,000 $26 44,000 32,000 $28 36,000 36,000 $30 30,000 40,000 $32 24,000 46,000