An Overview of Econometrics using B34S, MATLAB, Stata and SAS

advertisement

Econometric Notes

30 December 2014

Econometric Notes *

Houston H. Stokes

Department of Economics

University of Illinois in Chicago

hhstokes@uic.edu

An Overview of Econometrics * .......................................... 1

Objective of Notes .................................................. 1

1. Purpose of statistics................................................ 3

2. Role of statistics .................................................. 3

3. Basic Statistics ................................................... 4

4. More complex setup to illustrate B34S Matrix Approach..................... 11

5. Review of Linear Algebra and Introduction to Programming Regression Calculations 14

Figure 5.1 X'X for a random Matrix X ................................... 22

Figure 5.2 3D plot of 50 by 50 X'X matrix where X is a random matrix Error! Bookmark

not defined.

6. A Sample Multiple Input Regression Model Dataset ........................ 25

Figure 6.1 2 D Plots of Textile Data ..................................... 31

Figure 6.2 3-D Plot of Theil (1971) Textile Data ............................ 33

7. Advanced Regression analysis ....................................... 47

Figure 7.1 Analysis of residuals of the YMA model. .......................... 58

Figure 7.2 Recursively estimated X1 and X3 coefficients for X1 Sorted Data .......... 60

Figure 7.3 CUSUM test on Estimated with Sorted Data ........................ 61

Figure 7.4 CUMSQ Test of Model y model estimated with sorted data............... 63

Figure 7.5 Quandt Likelihood Ratio tests of y model estimated with sorted data. ....... 64

8. Advanced concepts ............................................. 64

9. Summary .................................................... 67

Objective of Notes

The objective of these notes is to introduce students to the basics of applied regression calculation

using STATA setups of a number of very simple models. Computer code is shown to allow students

to "get going" ASAP. More advanced sections show matlab code to made calculations. The notes are

1

Econometric Notes

organized around the estimation of regression models and the use of basic statistical concepts. The

textbooks Introduction to Econo metrics by Christopher Dougherty 4th Edition Oxford 2011 or

Introductory Econometrics: A Modern Approach by Jeffrey Wooldridge 5th Edition, South-Western

Cengage 2013 can be used to provide added information. A number of examples from this book will

be shown. Statistical analysis will be treated, both as a means by which the data can be summarized,

and as a means by which it is possible to accept or reject a specific hypothesis. Four simple datasets

are initially discussed:

-

The Price vs Age of Cars dataset illustrates a simple 2 variable OLS model where

graphics and correlation analysis can be used to detect relationships.

-

The Theil (1971) Textile deta set illustrates use of log transformations and contracts 2D

and 3D graphic analysis of data. A variable with a low correlation was show to enter an

OLS model only in the presence of another variable.

-

The Brownlee (1965) Stack Loss data set illustrates how in a multiple regression context,

variables with "significant" correlation may not enter a full model.

-

The Brownlee (1965) Stress data set illustrates the dangers of relying on correlation

analysis.

Finally a number of statistical problems and procedures that might be used are discussed.

2

Econometric Notes

1. Purpose of statistics

- Summarize data

- Test models

- Allow one to generalize from a sample to the wider population.

2. Role of statistics

Quote by Stanley (1856) in a presidential address to section F of the British Association for the

Advancement of Science.

"The axiom on which ....(statistics) is based may be stated thus: that the laws by which nature is

governed, and more especially those laws which operate on the moral and physical condition of the

human race, are consistent, and are, in all cases best discoverable - in some cases only discoverable by the investigation and comparison of phenomena extending over a very large number of individual

instances. In dealing with MAN in the aggregate, results may be calculated with precision and

accuracy of a mathematical problem... This then is the first characteristic of statistics as a science:

that it proceeds wholly by the accumulation and comparison of registered facts; - that from these

facts alone, properly classified, it seeks to deduce general principles, and that it rejects all a priori

reasoning, employing hypothesis, if at all, only in a tentative manner, and subject to future

verification"

3

Econometric Notes

(Note: underlining entered by H. H. Stokes)

3. Basic Statistics

Key concepts:

x x / N x

-Mean

-Median

-Mode

-Population Variance

=middle data value

= data value with most cases

= x2

-Sample Variance

-Population Standard Deviation

= s2

= x

-Sample Standard Deviation

-Confidence Interval with k%

-Correlation

= sx

=> a range of data values

= p xy

k

y i X i e

-Regression

i 1

Where X i = is a N by K matrix of explanatory variables.

-Percentile

-Quartile

-Z score

-t test

-SE of the mean

-Central Limit Theorem

Statistics attempts to generalize about a population from a sample. For the purposes of this

discussion assume the population of men in the US. A 1/1000 sample from this population would be

a randomly selected sample of men such that the sample contained only one male for every 1000 in

the population. The task of statistics is to be able to draw meaningful generalizations from the

sample about the population. It is costly, and often impossible, to examine all the measurements in

the population of interest. A sample must be selected in such a manner such that it is representative

of the population.

In a famous example of the potential for problems in sample selection, during the depression

in the 1932 presidential election the Literery Digest attempted to sample the electorate. A staff was

selected and numbers to call were randomly selected from the phone book in New York. In each

call the question was asked “Who will you vote for, Mr. Roosevelt or President Hoover?” Those

called, for the most part, supported President Hoover being relected. When Mr. Roosevelt won the

election, the question was asked? What went wrong in the sampling process? The assumption that

those who had phones was the correct characterization of poplution of the voters, was the problem.

4

Econometric Notes

Those without phones in that period disproportionally went for Mr. Roosevelt biasing the results of

the study.

In summary, statistics allows us to use the information contained in a representative sample

to correctly make inferences about the population. For example if one were interested in ascertaining

how long the light bulbs produced by a certain company last, one could hardly test them all.

Sampling would be necessary. The bootstrap can be used to test the distribution of statistics

estimated from a sample whose distribution is not known.

In addition to sampling correctly, it is important to be able to detect a shift in the underlying

population. The usual practice is to draw a sample from the population to be able to make inferences

about the underlying population. If the population is shifting, such samples will give biased

information. For example assume a reservoir. If a rain comes and adds to and stirs up the water in

the reservoir, samples of water would have to be taken more frequently than if there had been no rain

and there was no change in water usage. The interesting question is how do you know when to start

increasing the sampling rate? A possible approach would be to increase the sampling rate when the

water quality of previous samples begins to fall outside normal ranges for the focus variable. In this

example, it is not possible to use the population of all the water in the reservoir to test the water. A

number of key concepts are listed next.

Measures of Central Tendency. The mean is a measure of central tendency. Assume a vector

x containing N observations. The mean is defined as

N

x xi / N

(3-1)

i 1

Assuming xi = (1 2 3 4 5 6 7 8 9), then N=9, and x 5 . The mean is often written as x or E(x) or

the expected value of x. The problem with the mean as a measure of central tendency is that it is

affected by all observations. If instead of making x9 = 9, make x9 = 99. Here x (45 90) / 5 15

which is bigger than all xi values except x9. The median defined as the middle term of an odd

number of terms or the average of the two middle terms when the terms have been arranged in

increasing order is not affected by outlier terms. In the above example the median is 5 no matter

whether x9 = 9 or x9 = 99. The final measure of central tendency is the mode or value which has the

highest frequency. The mode may not be unique. In the above example, it does not exist.

Variation. It has been reported that a poor statistician once drowned in a stream with a mean

depth of 6 inches. How could this occur? To summarize the data, we also need to check on

variation, something that can be done by looking at the standard deviation and variance. The

population variance of a vector x is defined as

x2 i 1 ( xi x )2 / N

N

(3-2)

5

Econometric Notes

while the sample variance s x2 is

N

sx2 ( xi x ) 2 /( N 1)

(3-3)

i 1

The population standard deviation x is the square root of the population variance. For the purposes

of these notes, the standard deviation will mean the sample standard deviation. There are alternative

formulas for these values that may be easier to use. As an alternative to (3-2) and (3-3)

N

N

i 1

i 1

N

N

i 1

i 1

x2 ( N xi ( xi ) 2 ) / N 2

(3-4)

sx2 ( N xi ( xi ) 2 ) / N ( N 1)

(3-5)

For implementing the variance in a computer program, (3-2) is more accurate than (3-4)? Why is

this the case?

If sx is unbiased, a general rule is that xi will lie 99% of the time in + - 3 standard

deviations, 95% of the time in + - 2 standard deviations, and 68% of the time in + - 1 standard

deviations. Given a vector of numbers, it is important to determine where a certain number might lie.

There are 4 quartile positions of a series. Quartile 1 is the top of the lower 25%, quartile 2 the top of

the lower 50% or the median. Quartile 3 is the top of the 75%. The standard deviation gives

information concerning where observations lie. Assume x = 10, sx = 5 and N = 300. The question

asked is how likely will a value > 14 occur? To answer this question requires putting the data in Z

form where

Z ( xi x ) / sx

(3-6)

Think of Z as a normalized deviation. Once we get Z, we can enter tables and determine how likely

this will occur. In this case Z = (14-10)/5 = .8.

Distribution of the mean. It often is desirable to know how the sample mean x is

distributed. Assuming a vector has a finite distribution and that each xi value is mutually

independent, then the Central Limit Theorem states that if the vector ( x1 ,...., xN ) has any distribution

with mean and variance 2 , then the distribution of x approaches the normal distribution with

mean and variance 2 / N as sample size N increases. Note that the standard deviation of the mean

x defined as

6

Econometric Notes

x / N

(3-7)

Given x and x the 95% confidence interval around x is

x 2 x x x 2 x_

(3-8)

For small samples (<30) the formula is

x t.025 ( sx / N ) 2 x x t.025 ( sx / N ) 2

(3-9)

Tests of two means. Assume two vectors x and y where we know x , y , sx2 and s 2y . The simplest test

if the means differ is

Z ( x y ) /(( sx2 / N x ) ( s2y / N y )).5

(3-10)

where the small sample approximation assuming the two samples have the same population standard

deviation is

t ( x y ) /(( s2p / N x ) ( s2p / N y )).5

(3-11)

s2p (( N x 1)sx2 ( N y 1)s 2y ) /( N x N y 2)

(3-12)

Note that s 2p is an estimate of the population variance.

Correlation. If two variables are thought to be related, a possible summary measure would be

the correlation coefficient . Most calculators or statistical computer programs will make the

calculation. The standard error of is ( N 1) .5 for small samples and N .5 for large samples.

This means that p /( N 1).5 is distributed as a t statistic with asymptotic percentages as given above .

The correlation coefficient is defined as

( xy ( x y )) /( x y )

(3-13)

Perfect positive correlation is 1.0, perfect negative correlation is -1.0. The SE of is converges to

0.0 as N . If N was 101, the SE of r would be 1/10 or .1. | | must be .2 to be significant at or

better than the 95% level. Correlation is major tool of analysis that allows a person to formalize what

7

Econometric Notes

is shown in an x y plot of the data. A simple data set will be used to illustrates these concepts and

introduce OLS models as well as show the flaws of correlation analysis as a diagnostic tool.

Single Equation OLS Regression Model. Data was obtained on 6 observations on age and

value of cars (from Freund [1960] Modern Elementary Statistics, page 332), two variables that are

thought to be related. Table One lists this data and gives means, correlation between age and value

and a simple regression value=f(age). We expect the relationship to be negative and significant.

Table 1. Age of cars

Obs

1

2

3

4

5

6

Age

1

3

6

10

5

2

Mean

4.5

Variance

10.7

Correlation

Value

1995

875

695

345

595

1795

1050

461750

-0.85884

Next we show the Stata command files to obtain analysis of this data. Assume you have a file

car_age_data.do

input double

0.1E+01

0.3E+01

0.6E+01

0.1E+02

0.5E+01

0.2E+01

end

label variable x

input double

0.1995E+04

0.8750E+03

0.6950E+03

0.3450E+03

0.5950E+03

0.1795E+04

label variable y

//

x

"AGE OF CARS

"

"PRICE OF CARS

"

y

Comment

// run

car_age_data.do

describe

summarize

list

correlate (x y)

regress y x

twoway (scatter y x)

8

Econometric Notes

Edited output is:

clear

. run

car_age_data.do

.

describe

Contains data

obs:

6

vars:

2

size:

96

----------------------------------------------------------------------------------storage display

value

variable name

type

format

label

variable label

----------------------------------------------------------------------------------x

double %10.0g

AGE OF CARS

y

double %10.0g

PRICE OF CARS

----------------------------------------------------------------------------------Sorted by:

Note: dataset has changed since last saved

.

summarize

Variable |

Obs

Mean

Std. Dev.

Min

Max

-------------+-------------------------------------------------------x |

6

4.5

3.271085

1

10

y |

6

1050

679.5219

345

1995

.

list

1.

2.

3.

4.

5.

6.

+-----------+

| x

y |

|-----------|

| 1

1995 |

| 3

875 |

| 6

695 |

| 10

345 |

| 5

595 |

|-----------|

| 2

1795 |

+-----------+

.

(obs=6)

correlate (x y)

|

x

y

-------------+-----------------x |

1.0000

y | -0.8588

1.0000

.

regress y x

Source |

SS

df

MS

-------------+-----------------------------Model | 1702935.05

1 1702935.05

Residual | 605814.953

4 151453.738

-------------+-----------------------------Total |

2308750

5

461750

Number of obs

F( 1,

4)

Prob > F

R-squared

Adj R-squared

Root MSE

=

=

=

=

=

=

6

11.24

0.0285

0.7376

0.6720

389.17

-----------------------------------------------------------------------------y |

Coef.

Std. Err.

t

P>|t|

[95% Conf. Interval]

-------------+---------------------------------------------------------------x | -178.4112

53.20631

-3.35

0.028

-326.1356

-30.68683

_cons |

1852.85

287.3469

6.45

0.003

1055.048

2650.653

-----------------------------------------------------------------------------.

twoway (scatter y x)

.

end of do-file

9

0

500

1000

1500

2000

Econometric Notes

0

2

4

AGE OF CARS

6

8

10

From the plot we see that the ten year old car appears to have a larger that expected value for its age.

For this reason, more variables and observations are needed.

Remark: When there are two series correlation and plots can be used effectively to determine the

model. However when there are more that two series, plots and correlation analysis are less useful

and in may cases can give the wrong impression. This will be illustrated later. In cases where there

are more than one explanatory variable, regression is the appropriate approach, although this

approach has many problems.

A regression tries to write the dependent variable y as a linear function of the explanatory variables.

In this case we have estimated a model of the form

y xe

(3-14)

where y=value is the price of the car in period t, x=age is the age in period t and e is the error term.

Regression output produces

10

Econometric Notes

value = 1852.8505 - 178.41121*age

(6.45)

(-3.35)

(3-15)

R2 = .672, SEE = 389.17, e'e = 605814.953

which can be verified from the printout. Note that SEE= 605814.953 / 4 (e ' e) / n k .

The regression model suggests that every year older a car gets the value significantly drops

$178.41. A car one year old should have a value of 1852.8505 - (1)*178.41221 = 1674.4. In the

sample data set the one year old car in fact had a value of 1995. For this observation the error was

320.56. Using the estimated equation (3-14) we have

Age

1

3

6

10

5

2

Actual Value

1995

875

695

345.0

595

1795

Estimated Value

1674.4

1317.6

782.38

68.738

960.79

1496

Error

320.56

-442.62

-87.383

276.26

-365.79

298.97

t scores have been placed under the estimated coefficients. Since for both coefficients |t| > 2, we can

state that given the assumptions of the linear regression model, both coefficients are significant.

Before turning to an in-depth discussion of the regression model, we look at a few optional topics.

4. More complex setup to illustrate Matlab to estimate the Model. Optional Topic.

This optional topic implements the key ideas in Appendix E of Wooldridge (2013) that show how a

linear econometrioc model has be estimated by OLS. As discussed in the text, a linear OLS Model

selects the coefficients so as to minimize the sum of squared errors. Define X as an N by K matrix

where N is the number of observation of K series. The OLS coefficient vector ( X ' X ) 1 X ' y

where y is the right hand side vector. The error vector e X . Standard errors of the coefficients

can be obtained from the square root of diagonal elements of 2 ( X ' X ) 1 where 2 e ' e /( N K ) .

As an alternative to the Stata regress command that was shown above, the self contained MATLAB

program that is listed next can be used to estimate the model.

%% Cars Example using Matlab

% Load data

x=[1,1;

1,3;

1,6;

1,10;

1,5;

1,2];

y=[1995 875 695 345 595 1795];

11

Econometric Notes

y=y';

value=y;

disp('Mean of dependent (Age) and Independent Variable (Value)')

disp([mean(y),mean(x(:,2))])

age=x(:,2);

disp('Small and Large Variances for Age and Value')

disp([var(age,0),var(age,1),var(value,0),var(value,1)])

disp('Correlation using formula and built in function')

cor=(mean(age.*y)-(mean(age)*mean(y)))/(sqrt(var(age,1))*sqrt(var(value,1)))

% using built in function

cor=corr([age,value])

%% Estimate the model

% Logic works for any sized problem!!

% for large # of obs put ; at end of [y,yhat,res] line

beta=inv(x'*x)*x'*y;

yhat=x*beta;

res=y-yhat;

disp('

Value

Yhat

Res')

[y,yhat,res]

ssr=res'*res;

disp('Sum of squared residuals')

disp(ssr)

df=size(x,1)-size(x,2);

se=sqrt(diag((ssr/df)*inv(x'*x)));

disp('

Beta

se

t')

t=beta./se;

[beta,se,t]

plot(res)

% plot(age,y,age,yhat)

disp('Durbin Watson')

i=1:1:5;

dw=((res(i+1)-res(i))'*(res(i+1)-res(i)))/(res'*res);

disp(dw)

Which produces output:

Mean of dependent (Age) and Independent Variable (Value)

1050

4.5

Small and Large Variances for Age and Value

10.7

8.9167 4.6175e+005 3.8479e+005

Correlation using formula and built in function

cor =

-0.85884

cor =

1

-0.85884

-0.85884

1

Value

Yhat

Res

ans =

1995

1674.4

320.56

875

1317.6

-442.62

695

782.38

-87.383

345

68.738

276.26

595

960.79

-365.79

1795

1496

298.97

Sum of squared residuals

12

Econometric Notes

6.0581e+005

Beta

ans =

1852.9

-178.41

Durbin Watson

2.7979

se

t

287.35

53.206

6.4481

-3.3532

which matches what was produced by the Stata regress commands which can give the user the

impression of a "black box." Our findings indicate that for every year on average the car falls in

value $178.41.

Remark: Econometric calculations can easily be programmed using 4th generation languages

without detailed knowledge of Fortran or C. This allows new techniques to be implemented without

waiting for software developers to "hard wire" these procedures.

13

Econometric Notes

5. Review of Linear Algebra and Introduction to Programming Regression Calculations.

Optional Topic for those with right math background.

Assume a problem where there are multiple x variables, all possibly related to y, and there is

some relationship between the x variables (multicollinearity). The proposed solution is to fit a linear

model of the form:

k

y i xi e ,

(5-1)

i 1

where y, xi and e are N element column vectors, i is the coefficient of xi and is the intercept of

the equation. A linear model such as (5-1) can be estimated by OLS (ordinary least squares), which

will minimize e ' e which a good measure of the fit of the model. OLS is one of many methods to fit

a line, others discussed being L1 which minimizes | e | and minimax which minimizes the largest

element in e. After the coefficients are calculated, it is a good idea to estimate and report standard

errors, which allow significance tests on the estimates of the parameters. OLS models can be

estimated, using matrix algebra directly or using pre programmed procedures like the regression

command in Excel. There are however a number of ways to calculate the estimated parameters.

Before this occurs we first illustrate a number of Linear algebra calculations that include the LU

factorization, eigenvalue analysis, the Cholesky factorization, the QR factoprization, the Schur

factorization (that always works when eigen values may not work) and the SVD calculation.

The LU factorization ( LU Z ) is the appropriate way to invert a general matrix. Eigenvalue

analysis decomposes Z V V 1 where is a diagonal matrix and Z is a general matrix. For the

positive definite case Z V V ' since here V 1 V ' . Inspection of the diagonal elements of

indicates whether lim k Z k explodes if we note X k V kV 1 . The sum of the diagonal elements of

are the trace of Z while their product is | Z | . If Z is positive definite (all diagonal elements of

>0) the Cholesky factorization writes Z R ' R where R is upper triangular. The Schur factorization

writes Z USU ' where U is orthogonal UU ' I and S is block upper triangular. Unlike the

eigenvalue transformation, all elements of the Schur factorization are real for the general matrix.

The QR factorization writes X QR where Q is orthogonal and R is the Cholesky factorization

calculated accurately since it used X not X ' X .

The SVD calculates X U V ' where both U and V are orthogonal and N by K and K by K and

is a K by K diagonal matrtrix whose elements are the square roots of the eigenvalues of X ' X . The

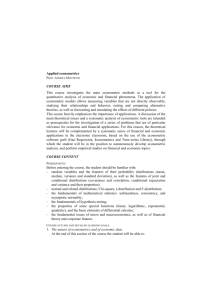

below listed Matlab script self documents these calculations and shows graphically X ' X where X

was 100 by 50. How would this graph look like if X was not a random matrix where by assumption

E ( X (, i ) X (, j )) 0 for i j ? How might it be used?

%% Linear Algebra Useful for Econometrics in Matlab

disp(' Short course in Math using Matlab(c)')

% 2 December 2006 Version

disp(' Houston H. Stokes')

14

Econometric Notes

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

All Matlab commands are indented. Cut and paste from this')

document into Matlab and execute.')

')

If ; is left off result will print.')

Define x as a n by n matrix of random numbers.')

x

= rand(n) ')

define x as a n by n matrix of random normal numbers')

xn

= randn(n)')

Do a LU factorization and test answer')

Inverse using LU

')

')

x

= rand(n)

')

[l u]

= lu(x)

')

test

= l*u

')

error

= l*u - x

')

ix

= inv(x)

')

ix2

= inv(u)*inv(l)

')

error

= ix - ix2

')

n=3

x

= rand(n)

[l u]

= lu(x)

test

= l*u

error

= l*u - x

ix

= inv(x)

ix2

= inv(u)*inv(l)

error

= ix - ix2

Form PD Matrix and look at it.

')

xx

= randn(100,10);

')

xpx

= xx`*xx

')

mesh(xpx)

')

xx

= randn(100,50);

xpx

= xx'*xx;

mesh(xpx)

Factor PD matrix into R(t)*R and test')

xx

= randn(100,n);

')

xpx

= xx(t)*xx

')

r

= chol(xpx)

')

test1

= r(t)*r

')

mesh(r)

')

error

= r(t)*r - xpx

')

xx

= randn(100,n);

xpx

= xx'*xx

r

= chol(xpx)

test1

= r'*r

error

= r'*r - xpx

disp(' Eigen and svd analysis. For pd matrix s = landa')

disp('

xx

= randn(100,n); ')

disp('

xpx

= xx(t)*xx

')

disp('

lamda

= eig(xpx)

')

xx

= randn(100,n);

xpx

= xx'*xx

lamda

= eig(xpx)

15

Econometric Notes

disp(' show trace = sum eigen')

disp('

det = prod(e) ')

disp('

trace1

= trace(xpx)

disp('

det1

= det(xpx)

disp('

trace2

= sum(lamda)

disp('

det2

= prod(lamda)

trace1

= trace(xpx)

det1

= det(xpx)

trace2

= sum(lamda)

det2

= prod(lamda)

')

')

')

')

disp(' Test SVD')

disp('

s

= svd(xpx) ')

disp('

[u ss v] = svd(xpx) ')

disp('

test

= u*ss*v(t)')

disp('

error

= xpx-test ')

s

= svd(xpx)

[u ss v] = svd(xpx)

test

= u*ss*v'

error

= xpx-test

disp(' Does X*V = V*Lamda')

disp('

xx

= randn(100,n); ')

disp('

xpx

= xx(t)*xx

')

disp('

[v lamda] = eig(xpx)

')

disp('

test

= v*lamda*inv(v)')

disp('

error

= xpx-test

')

disp('

vpv

= v(t)*v

')

disp('

s

= svd(xpx)

')

xx

= randn(100,n);

xpx

= xx'*xx

[v lamda] = eig(xpx)

test

= v*lamda*inv(v)

error

= xpx-test

vpv

= v'*v

s

= svd(xpx)

disp(' Schur Factorization X = U S U(t) where U is orthogonal and')

disp(' S is block upper triangural with 1 by 1 and 2 by 2 on the')

disp(' diagonal. All elements of a Schur factorization real')

disp('

xx

= randn(100,n); ')

disp('

xpx

= xx(t)*xx

')

disp('

[U,S]

= schur(xpx)

')

disp('

test

= U*S*U(t)

')

disp('

error

= xpx-test

')

xx

= randn(100,n);

xpx

= xx'*xx

[U,S]

= schur(xpx)

test

= U*S*U'

error

= xpx-test

disp(' Schur Factorization')

disp('

xx

= randn(n,n)

')

disp('

[U,S]

= schur(xx)

')

16

Econometric Notes

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

disp('

test

= U*S*U(t)

')

error

= xx-test

')

xx

= randn(n,n)

[U,S]

= schur(xx)

test

= U*S*U'

error

= xx-test

QR Factorization preserves length and angles and does not magnify')

errors. We express X = Q*R where Q is orthogonal and R is upper')

triangular

')

x

= randn(n,n) ')

[Q R]

= qr(x)

')

test1

= Q(t)*Q

')

test2

= Q*R

')

error

= x - test2

')

x

= randn(n,n)

[Q R]

= qr(x)

test1

= Q'*Q

test2

= Q*R

error

= x - test2

and produces output:

Short course in Math using Matlab(c)

Houston H. Stokes

All Matlab commands are indented. Cut and paste from this

document into Matlab and execute.

If ; is left off result will print.

Define x as a n by n matrix of random numbers.

x

= rand(n)

define x as a n by n matrix of random normal numbers

xn

= randn(n)

Do a LU factorization and test answer

Inverse using LU

x

[l u]

test

error

ix

ix2

error

= rand(n)

= lu(x)

= l*u

= l*u - x

= inv(x)

= inv(u)*inv(l)

= ix - ix2

n =

3

x =

0.84622

0.52515

0.20265

0.67214

0.83812

0.01964

0.68128

0.37948

0.8318

1

0.62059

0.23947

0

1

-0.33568

0

0

1

0.84622

0

0

0.67214

0.421

0

0.68128

-0.04331

0.65411

l =

u =

test =

17

Econometric Notes

0.84622

0.67214

0.68128

0.52515

0.83812

0.37948

0.20265

0.01964

0.8318

error =

0

0

0

0

0

0

0 -6.9389e-018

0

ix =

2.9596

-2.3417

-1.3557

-1.5445

2.4281

0.15727

-0.68458

0.51318

1.5288

ix2 =

2.9596

-2.3417

-1.3557

-1.5445

2.4281

0.15727

-0.68458

0.51318

1.5288

error =

0

0

0

0

0

0

-1.1102e-016

0

0

Form PD Matrix and look at it.

xx

= randn(100,10);

xpx

= xx`*xx

mesh(xpx)

Factor PD matrix into R(t)*R and test

xx

= randn(100,n);

xpx

= xx(t)*xx

r

= chol(xpx)

test1

= r(t)*r

mesh(r)

error

= r(t)*r - xpx

xpx =

98.02

17.334

0.14022

17.334

104.66

-7.2052

0.14022

-7.2052

114.22

r =

9.9005

1.7508

0.014163

0

10.08

-0.71729

0

0

10.663

test1 =

98.02

17.334

0.14022

17.334

104.66

-7.2052

0.14022

-7.2052

114.22

error =

1.4211e-014

0

0

0

0

0

0

0

0

Eigen and svd analysis. For pd matrix s = landa

xx

= randn(100,n);

xpx

= xx(t)*xx

lamda

= eig(xpx)

xpx =

95.217

-3.5453

12.006

-3.5453

96.003

-3.9312

12.006

-3.9312

92.989

lamda =

82.025

93.783

108.4

show trace = sum eigen

det = prod(e)

18

Econometric Notes

trace1

= trace(xpx)

det1

= det(xpx)

trace2

= sum(lamda)

det2

= prod(lamda)

trace1 =

284.21

det1 =

8.3388e+005

trace2 =

284.21

det2 =

8.3388e+005

Test SVD

s

= svd(xpx)

[u ss v] = svd(xpx)

test

= u*ss*v(t)

error

= xpx-test

s =

108.4

93.783

82.025

u =

-0.67492

0.3165

0.66657

0.39135

0.91936

-0.040277

-0.62557

0.23368

-0.74435

ss =

108.4

0

0

0

93.783

0

0

0

82.025

v =

-0.67492

0.3165

0.66657

0.39135

0.91936

-0.040277

-0.62557

0.23368

-0.74435

test =

95.217

-3.5453

12.006

-3.5453

96.003

-3.9312

12.006

-3.9312

92.989

error =

-2.8422e-014 -1.199e-014 -4.0856e-014

-9.3703e-014 -2.8422e-014 5.9064e-014

-4.7962e-014 -5.3291e-015 1.4211e-014

Does X*V = V*Lamda

xx

= randn(100,n);

xpx

= xx(t)*xx

[v lamda] = eig(xpx)

test

= v*lamda*inv(v)

error

= xpx-test

vpv

= v(t)*v

s

= svd(xpx)

xpx =

98.321

-0.36605

1.9557

-0.36605

127.52

-2.4594

1.9557

-2.4594

112.74

v =

0.99127

0.1298

0.022941

0.0013134

0.1643

-0.98641

-0.13181

0.97783

0.1627

lamda =

98.061

0

0

0

112.59

0

19

Econometric Notes

0

0

127.93

test =

98.321

-0.36605

1.9557

-0.36605

127.52

-2.4594

1.9557

-2.4594

112.74

error =

-1.4211e-014 2.7645e-014 2.2204e-015

2.9421e-014 -4.2633e-014 5.7732e-015

1.7764e-015 -1.3323e-015

0

vpv =

1 2.7756e-017 -2.0817e-017

2.7756e-017

1 -2.498e-016

-2.0817e-017 -2.498e-016

1

s =

127.93

112.59

98.061

Schur Factorization X = U S U(t) where U is orthogonal and

S is block upper triangural with 1 by 1 and 2 by 2 on the

diagonal. All elements of a Schur factorization real

xx

= randn(100,n);

xpx

= xx(t)*xx

[U,S]

= schur(xpx)

test

= U*S*U(t)

error

= xpx-test

xpx =

75.062

11.465

-4.6863

11.465

135.28

7.6196

-4.6863

7.6196

87.647

U =

-0.91599

-0.36457

-0.16747

0.20355

-0.062606

-0.97706

-0.34572

0.92907

-0.13156

S =

70.745

0

0

0

88.973

0

0

0

138.27

test =

75.062

11.465

-4.6863

11.465

135.28

7.6196

-4.6863

7.6196

87.647

error =

1.4211e-014 2.1316e-014 -1.4211e-014

2.4869e-014 -8.5265e-014 7.1054e-015

-1.0658e-014 5.3291e-015 1.4211e-014

Schur Factorization

xx

= randn(n,n)

[U,S]

= schur(xx)

test

= U*S*U(t)

error

= xx-test

xx =

2.095

0.93943

-0.45994

0.34979

-0.047081

0.64722

2.0142

-1.4799

-1.8411

U =

-0.89939

-0.19282

0.39233

-0.24726

-0.51574

-0.82029

-0.3605

0.83477

-0.41617

S =

2.1689

1.4404

-1.1939

20

Econometric Notes

0

0

-0.98103

-0.42339

2.3141

-0.98103

test =

2.095

0.93943

-0.45994

0.34979

-0.047081

0.64722

2.0142

-1.4799

-1.8411

error =

8.8818e-016 -2.2204e-016 -1.6653e-016

1.1102e-016

9.09e-016 8.8818e-016

4.4409e-016 3.3307e-015 8.8818e-016

QR Factorization preserves length and angles and does not magnify

errors. We express X = Q*R where Q is orthogonal and R is upper

triangular

x

= randn(n,n)

[Q R]

= qr(x)

test1

= Q(t)*Q

test2

= Q*R

error

= x - test2

x =

-0.9756

0.55997

0.88166

0.028304

0.62542

0.15174

-0.050706

0.53695

-0.017682

Q =

-0.99823

0.0094729

-0.058658

0.028961

-0.78444

-0.61953

-0.051883

-0.62013

0.78278

R =

0.97733

-0.56872

-0.87479

0

-0.81828

-0.099712

0

0

-0.15956

test1 =

1

0 6.9389e-018

0

1 -1.6653e-016

6.9389e-018 -1.6653e-016

1

test2 =

-0.9756

0.55997

0.88166

0.028304

0.62542

0.15174

-0.050706

0.53695

-0.017682

error =

0

0 -4.4409e-016

3.4694e-018 2.2204e-016 8.3267e-017

0

0 2.0817e-017

21

Econometric Notes

X'X Where X was 100 by 50

140

120

100

80

60

40

20

0

-20

-40

50

40

50

30

40

30

20

20

10

10

0

0

Figure 5.1 X'X for a random Matrix X

These ideas are illustrated using the Theil dataset discussed in more detail in the next section.

%% Use of Theil Data to Illustrate various ways to get Beta

% For more detail on these calculations see Stokes (200x) Chapter 10

disp('Theil (1971) data on Year CT RP Income')

data=[

1923

99.2

96.7

101.0;

1924

99.0

98.1

100.1;

1925

100.0

100.0

100.0;

1926

111.6

104.6

90.6;

1927

122.2

104.9

86.5;

1928

117.6

109.5

89.7;

1929

121.1

110.8

90.6;

1930

136.0

112.3

82.8;

1931

154.2

109.3

70.1;

1932

153.6

105.3

65.4;

1933

158.5

101.7

61.3;

22

Econometric Notes

1934

140.6

95.4

62.5;

1935

136.2

96.4

63.6;

1936

168.0

97.6

52.6;

1937

154.3

102.4

59.7;

1938

149.0

101.6

59.5;

1939

165.5

103.8

61.3]

y=data(:,2);

x=[ones(size(data,1),1),data(:,3),data(:,4)];

disp('Beta using Inverse')

beta1=inv(x'*x)*x'*y

%% QR

disp('Using QR approach')

[q,r]=qr(x,0)

disp('Testing q')

q'*q

beta2=inv(r)*q'*y

yhat=q*q'*y;

resid=y-yhat;

disp('Y

Yhat

Residual')

[y,yhat,resid]

%% Testing R from QR and R from Cholesky

disp('Inverse (xpx) = inv(r)*transpose(inv(r))')

inv(x'*x)

inv(r)*(inv(r))'

r

cholr=chol(x'*x)

%% SVD approach that includes PC Regression

disp('SVD approach')

[u,s,v]=svd(x,0)

pc_coef=u'*y

beta3=inv(v')*inv(s)*pc_coef

Output produced is:

Theil (1971) data on

data =

1923

1924

1925

1926

1927

1928

1929

1930

1931

1932

1933

1934

1935

1936

1937

1938

1939

Beta using Inverse

beta1 =

130.23

Year CT RP Income

99.2

99

100

111.6

122.2

117.6

121.1

136

154.2

153.6

158.5

140.6

136.2

168

154.3

149

165.5

96.7

98.1

100

104.6

104.9

109.5

110.8

112.3

109.3

105.3

101.7

95.4

96.4

97.6

102.4

101.6

103.8

101

100.1

100

90.6

86.5

89.7

90.6

82.8

70.1

65.4

61.3

62.5

63.6

52.6

59.7

59.5

61.3

23

Econometric Notes

1.0659

-1.3822

Using QR approach

q =

-0.24254

-0.2958

-0.42465

-0.24254

-0.2297

-0.39928

-0.24254

-0.13999

-0.38173

-0.24254

0.077214

-0.20134

-0.24254

0.091379

-0.13707

-0.24254

0.30858

-0.14641

-0.24254

0.36996

-0.14898

-0.24254

0.44079

-0.018862

-0.24254

0.29913

0.14704

-0.24254

0.11027

0.18403

-0.24254

-0.059716

0.21536

-0.24254

-0.35718

0.14409

-0.24254

-0.30997

0.13597

-0.24254

-0.25331

0.31174

-0.24254

-0.026664

0.24537

-0.24254

-0.064438

0.24162

-0.24254

0.03944

0.2331

r =

-4.1231

-424.53

-314.64

0

21.179

11.878

0

0

-66.411

Testing q

ans =

1 8.1532e-017 1.3878e-017

8.1532e-017

1 -1.1796e-016

1.3878e-017 -1.1796e-016

1

beta2 =

130.23

1.0659

-1.3822

Y

Yhat

Residual

ans =

99.2

93.704

5.4962

99

96.44

2.56

100

98.603

1.3965

111.6

116.5

-4.8995

122.2

122.49

-0.28637

117.6

122.97

-5.3664

121.1

123.11

-2.0081

136

135.49

0.51173

154.2

149.84

4.3553

153.6

152.08

1.5225

158.5

153.91

4.5927

140.6

145.53

-4.9335

136.2

145.08

-8.8789

168

161.56

6.4376

154.3

156.87

-2.565

149

156.29

-7.2887

165.5

156.15

9.3542

Inverse (xpx) = inv(r)*transpose(inv(r))

ans =

23.773

-0.2272

-0.0042094

-0.2272

0.0023008 -0.00012716

-0.0042094 -0.00012716

0.00022673

ans =

23.773

-0.2272

-0.0042094

24

Econometric Notes

-0.2272

-0.0042094

0.0023008

-0.00012716

-0.00012716

0.00022673

-4.1231

0

0

cholr =

4.1231

0

0

SVD approach

u =

0.26014

0.26123

0.26398

0.26026

0.25606

0.26662

0.26959

0.26301

0.2441

0.23275

0.22268

0.21455

0.2173

0.20664

0.22192

0.22049

0.22584

s =

530.48

0

0

v =

0.0077424

0.799

0.60128

pc_coef =

545.81

131.94

26.706

beta3 =

130.23

1.0659

-1.3822

-424.53

21.179

0

-314.64

11.878

-66.411

424.53

21.179

0

314.64

11.878

66.411

-0.42317

-0.39389

-0.37096

-0.17816

-0.11332

-0.1094

-0.10823

0.025612

0.18215

0.20748

0.22834

0.13929

0.13408

0.31251

0.26022

0.25419

0.25202

0.28267

0.21821

0.12977

-0.076467

-0.086908

-0.30402

-0.36537

-0.42853

-0.27778

-0.087337

0.08395

0.37648

0.32893

0.28251

0.052713

0.090163

-0.013903

0

53.304

0

0

0

0.20509

0.0056046

0.60125

-0.79904

0.99995

-0.0095564

-0.00017699

r =

Remark: This section shows how to implement the basic linear algebra relationships that are useful

in understanding modern econometric methods and calculations. In many cases these new

approaches are required to be used for complex and multi-collinear datasets.

6. A Sample Multiple Input Regression Model Dataset

In sections 3 and 4 we introduced a small (6 observation dataset) that relates age of cars to

their value. We observed that since there are so few observations in this example, the correlation

25

Econometric Notes

coefficient must be relatively large to be significant. The small sample standard error of the

correlation coefficient is calculated using (3.3) which is this case is .4472 1/ 5 . Since the absolute

value of the correlation coefficient (-.85884) is about 2 times the standard error, we can state that at

about the 95% level, the correlation coefficient is significant. The problem with correlation analysis

is that it is hard to make direct predictions. What is wanted is a relationship where, if given only the

age of a car, we can make some prediction on its price. To obtain an answer to the prediction

problem requires more advanced statistical techniques. Its solution will be discussed further below.

As discussed earlier, when more complicated models are deemed appropriate or when predictions

are required, the correlation coefficient statistical procedure, which restricts analysis to two

variables, is no longer the best way to proceed. In the highly unlikely situation where all the

variables influencing y (the x's) were unrelated among themselves (i. e., were orthogonal),

correlation analysis would give the correct sign of the relationship between each x variable and y.

This situation would occur if the x's were principal components. In a later example, using generated

data, some of these possibilities will be illustrated with further examples.

Table Two lists data on the consumption of textiles in the Netherlands from Theil( [1971]

Principles of Econometrics, page 102) which was used as an example in the Matlab code in section

5. This example will be shown to provide a better fit than the previous example and, in addition,

illustrates multiple input regression models. (It should be noted that not all economics examples

work this well.) Usually time series models have higher R 2 than cross section models, because of

the serial correlation (relationship between the error terms across time) implicit in most time series.

In this example from Theil (l971) the consumption of textiles in the Netherlands (CT) between 19231939 is modeled as a function of income (Y) and the relative price of textiles (RP). The maintained

hypothesis is that as income increases, the consumption of textiles should increase and as the relative

price of textiles increases, the consumption of textiles should decrease. Two models are tried, one

with the raw data and one with data logged to the base 10. The linear model asserts

Table Two

Consumption of Textiles in the Netherlands: 1923-1939

Year

1923

1924

1925

1926

1927

1928

1929

1930

1931

1932

1933

1934

1935

1936

CT

99.2

99.0

100.0

111.6

122.2

117.6

121.1

136.0

154.2

153.6

158.5

140.6

136.2

168.0

Y

96.7

98.1

100.0

104.6

104.9

109.5

110.8

112.3

109.3

105.3

101.7

95.4

96.4

97.6

RP

101.0

100.1

100.0

90.6

86.5

89.7

90.6

82.8

70.1

65.4

61.3

62.5

63.6

52.6

26

Econometric Notes

1937

1938

1939

154.3

149.0

165.5

102.4

101.6

103.8

59.7

59.5

61.3

CT = consumption of textiles.

Y = income.

RP = relative price of textiles.

CT 1 y 2 RP e

(6-1)

while the log form assumes the error is multiplicative or that

CT y 1 ( RP) 2 e

(6-2)

(6-2) can be estimated in log form as

log10(CT ) log10( ) 1 log10( y) 2 log( RP)

(6-3)

Actual estimates of the alternative models were

CT 130.7006 1.061710* y 1.382985* RP

(4.824)

( 16.50)

(3.981)

R 2 .94432 e ' e 433.3

log10(CT ) 1.373914 1.143156*log10( y ) .8288375*log( RP )

(4.4886) (7.3279)

( 22.952)

(6.4)

R 2 .97070 e ' e .002568

Prior to preliminary estimation, raw correlations and plots were performed. The log transformation

was attempted to make the time series data stationary. B34S and SAS commands to analyze this data

are shown next

Note that B34S requires the user to explicitly define variables to be built with the gen statements

with the build statement when using the B34S data step. This allows for checking of variable

names in the gen statements. For SAS the following commands would be used.

data theil;

INPUT CT Y RP

LABEL CT

LABEL LOG10CT

LABEL Y

LABEL LOG10Y

LABEL RP

LABEL LOG10RP

;

=

=

=

=

=

=

'CONSUMPTION OF TEXTILES'

;

'LOG10 OF CONSUMPTION'

;

'INCOME'

;

' LOG10 OF INCOME '

;

'RELATIVE PRICE OF TEXTILES';

'LOG10 OF RELATIVE PRICE'

;

27

Econometric Notes

LOG10CT = LOG10(CT)

LOG10RP = LOG10(RP)

LOG10Y = LOG10(Y)

CARDS;

99.2

96.7 101

99

98.1 100.1

100

100

100

111.6 104.9 90.6

122.2 104.9 86.5

117.6 109.5 89.7

121.1 110.8 90.6

136

112.3 82.8

154.2 109.3 70.1

153.6 105.3 65.4

158.5 101.7 61.3

140.6 95.4 62.5

136.2 96.4 63.6

168

97.6 52.6

154.3 102.4 59.7

149

101.6 59.5

165.5 103.8 61.3

;

proc reg;

MODEL

proc reg;

MODEL

proc autoreg; MODEL

proc autoreg; MODEL

;

;

;

CT = Y RP; run;

LOG10CT = LOG10Y LOG10RP; run;

LOG10CT = LOG10Y LOG10RP / nlag=1 method=ml; run;

LOG10CT = LOG10Y

/ nlag=1 method=ml; run;

Edited output from B34S discussed below is:

Variable

# Label

CT

Y

RP

LOG10CT

LOG10Y

LOG10RP

CONSTANT

1

2

3

4

5

6

7

Mean

CONSUMPTION OF TEXTILES

INCOME

RELATIVE PRICE OF TEXTILES

LOG10 OF CONSUMPTION

LOG10 OF INCOME

LOG10 OF RELATIVE PRICE

Std. Dev.

134.506

102.982

76.3118

2.12214

2.01222

1.87258

1.00000

Variance

23.5773

5.30097

16.8662

0.791131E-01

0.222587E-01

0.961571E-01

0.00000

555.891

28.1003

284.470

0.625889E-02

0.495451E-03

0.924619E-02

0.00000

Data file contains

17 observations on

7 variables. Current missing value code is

B34S Version 8.42e (D:M:Y) 04/01/99 (H:M:S) 16:14:15

DATA STEP

Maximum

168.000

112.300

101.000

2.22531

2.05038

2.00432

1.00000

1

0.61769E-01

Var

2

RP

Var

3

1

-0.94664

LOG10CT

Var

4

1

0.99744

2

0.93936E-01

LOG10Y

Var

5

1

0.66213E-01

2

0.99973

3

0.17511

LOG10RP

Var

6

1

-0.93820

2

0.22599

3

0.99750

4

-0.93596

5

0.22212

CONSTANT

Var

7

1

0.0000

2

0.0000

3

0.0000

4

0.0000

5

0.0000

2

0.17885

***************

Problem Number

Subproblem Number

F to enter

F to remove

Tolerance

Maximum no of steps

Dependent variable X( 1).

Standard Error of Y =

.............

Step Number 3

3

-0.94836

4

0.97862E-01

6

0.0000

4

1

0.99999998E-02

0.49999999E-02

0.10000000E-04

3

Variable Name CT

23.577332

for degrees of freedom

=

16.

Analysis of Variance for reduction in SS due to variable entering

28

99.0000

95.4000

52.6000

1.99564

1.97955

1.72099

1.00000

0.1000000000000000E+32

Correlation Matrix

Y

Minimum

PAGE

2

Econometric Notes

Variable Entering

2

Multiple R

0.975337

Std Error of Y.X

5.56336

R Square

0.951282

Source

Due Regression

Dev. from Reg.

Total

Multiple Regression Equation

Variable

Coefficient

Std. Error

CT

=

Y

X- 2

1.061710

0.2666740

RP

X- 3 -1.382985

0.8381426E-01

CONSTANT

X- 7

130.7066

27.09429

Adjusted R Square

-2 * ln(Maximum of Likelihood Function)

Akaike Information Criterion (AIC)

Scwartz Information Criterion (SIC)

Akaike (1970) Finite Prediction Error

Generalized Cross Validation

Hannan & Quinn (1979) HQ

Shibata (1981)

Rice (1984)

Residual Variance

T Val.

DF

2

14

16

SS

8460.9

433.31

8894.2

MS

4230.5

30.951

555.89

T Sig. P. Cor. Elasticity

3.981

-16.50

4.824

0.99863 0.7287

1.00000 -0.9752

0.99973

F

136.68

Partial Cor. for Var. not in equation

Variable

Coefficient

F for selection

0.8129

-0.7846

0.944321908495049

103.294108058298

111.294108058298

114.626961434523

36.4128553394184

37.5832685467569

36.8112662258895

34.4851159390962

39.3920889580981

30.9509270385056

Order of entrance (or deletion) of the variables =

7

3

2

Estimate of computational error in coefficients =

1 -0.1889E-13

2 -0.2396E-14

3 0.7430E-11

Covariance Matrix of Regression Coefficients

Row

Row

Row

1

Variable X- 2

0.71115004E-01

Y

2

Variable X- 3

RP

-0.39974169E-02 0.70248306E-02

3

Variable X- 7

CONSTANT

-7.0185405

-0.12441382

Program terminated.

734.10069

All variables put in.

Residual Statistics for...

Original Data

Von Neumann Ratio 1 ...

Von Neumann Ratio 2 ...

For D. F.

2.14471

2.14471

14 t(.9999)=

Infin

0

1.000

1.000

Cell No.

Interval

Act Per

2

1.000

1.000

2.01855

5.3624, t(.999)= 4.1403, t(.99)= 2.9768, t(.95)= 2.1448, t(.90)= 1.7613, t(.80)= 1.3450

Skewness test (Alpha 3) = -.232914E-01,

t Stat

Cell No.

Interval

Act Per

Durbin-Watson TEST.....

Peakedness test (Alpha 4)=

1.37826

Normality Test -- Extended grid cell size

1.761

1.345

1.076

0.868

0.692

0.537

2

2

4

2

0

2

0.900

0.800

0.700

0.600

0.500

0.400

1.000

0.882

0.765

0.529

0.412

0.412

=

0.393

2

0.300

0.294

Normality Test -- Small sample grid cell size =

6

2

4

0.800

0.600

0.400

0.882

0.529

0.412

1.70

0.258

0.128

1

2

0.200

0.100

0.176

0.118

3.40

3

0.200

0.176

Extended grid normality test - Prob of rejecting normality assumption

Chi=

7.118

Chi Prob= 0.4760

F(8,

14)= 0.889706

F Prob =0.450879

Small sample normality test - Large grid

Chi=

3.294

Chi Prob= 0.6515

F(3,

14)=

1.09804

F Prob =0.617396

Autocorrelation function of residuals

1) -0.1546

F(

6,

2) -0.2529

6)

=

0.3219

Sum of squared residuals

433.3

3)

0.2272

1/F =

3.106

4) -0.3925

Heteroskedasticity at

Mean squared residual

0.9032

25.49

Gen. Least Squares ended by satisfying tolerance.

***************

Problem Number

Subproblem Number

4

2

F to enter

F to remove

Tolerance

Maximum no of steps

Dependent variable X( 4).

Standard Error of Y =

0.99999998E-02

0.49999999E-02

0.10000000E-04

3

Variable Name LOG10CT

0.79113140E-01

for degrees of freedom

=

29

16.

F Sig.

1.000000

level

Econometric Notes

.............

Step Number 3

Variable Entering

5

Multiple R

0.987097

Std Error of Y.X 0.135425E-01

R Square

0.974361

Analysis of Variance

Source

Due Regression

Dev. from Reg.

Total

Multiple Regression Equation

Variable

Coefficient

Std. Error

LOG10CT =

LOG10Y

X- 5

1.143156

0.1560002

LOG10RP

X- 6 -0.8288375

0.3611136E-01

CONSTANT

X- 7

1.373914

0.3060903

Adjusted R Square

-2 * ln(Maximum of Likelihood Function)

Akaike Information Criterion (AIC)

Scwartz Information Criterion (SIC)

Akaike (1970) Finite Prediction Error

Generalized Cross Validation

Hannan & Quinn (1979) HQ

Shibata (1981)

Rice (1984)

Residual Variance

T Val.

for reduction in SS due to variable entering

DF

SS

MS

F

2

0.97575E-01

0.48787E-01

266.02

14

0.25676E-02

0.18340E-03

16

0.10014

0.62589E-02

T Sig. P. Cor. Elasticity

7.328

-22.95

4.489

1.00000 0.8906

1.00000 -0.9870

0.99949

Partial Cor. for Var. not in equation

Variable

Coefficient

F for selection

1.084

-0.7314

0.970697895872232

-101.322167384484

-93.3221673844844

-89.9893140082595

0.215763077505479D-003

0.222698319282440D-003

0.218123847024249D-003

0.204340326343424D-003

0.233416420210472D-003

0.183398615879657D-003

Order of entrance (or deletion) of the variables =

7

6

5

Estimate of computational error in coefficients =

1 0.5793E-11

2 0.2356E-12

3 0.2547E-11

Covariance Matrix of Regression Coefficients

Row

1

Variable X- 5

0.24336056E-01

LOG10Y

Row

2

Variable X- 6

LOG10RP

-0.12513115E-02 0.13040301E-02

Row

3

Variable X- 7

CONSTANT

-0.46626424E-01 0.76017246E-04

Program terminated.

0.93691270E-01

All variables put in.

Residual Statistics for...

Original Data

Von Neumann Ratio 1 ...

Von Neumann Ratio 2 ...

For D. F.

14 t(.9999)=

2.04710

2.04710

Infin

1

1.000

1.000

Cell No.

Interval

Act Per

2

1.000

1.000

1.92669

5.3624, t(.999)= 4.1403, t(.99)= 2.9768, t(.95)= 2.1448, t(.90)= 1.7613, t(.80)= 1.3450

Skewness test (Alpha 3) = -.159503

t Stat

Cell No.

Interval

Act Per

Durbin-Watson TEST.....

,

Peakedness test (Alpha 4)=

1.44345

Normality Test -- Extended grid cell size

1.761

1.345

1.076

0.868

0.692

0.537

1

1

5

1

1

3

0.900

0.800

0.700

0.600

0.500

0.400

0.941

0.882

0.824

0.529

0.471

0.412

=

0.393

1

0.300

0.235

Normality Test -- Small sample grid cell size =

6

2

4

0.800

0.600

0.400

0.882

0.529

0.412

1.70

0.258

0.128

2

1

0.200

0.100

0.176

0.059

3.40

3

0.200

0.176

Extended grid normality test - Prob of rejecting normality assumption

Chi=

9.471

Chi Prob= 0.6958

F(8,

14)= 1.18382

F Prob =0.626481

Small sample normality test - Large grid

Chi=

3.294

Chi Prob= 0.6515

F(3,

14)=

1.09804

F Prob =0.617396

Autocorrelation function of residuals

1) -0.0990

F(

6,

2) -0.1061

6)

=

Sum of squared residuals

0.5544

3)

0.0862

1/F =

1.804

4) -0.3157

Heteroskedasticity at

0.2568E-02 Mean squared residual

0.1510E-03

Gen. Least Squares ended by satisfying tolerance.

We first show plots of the data.

30

0.7544

F Sig.

1.000000

level

Econometric Notes

Log Theil Data

LOG10CT

2.20

2.15

2.10

2.05

LOG10Y

2.00

1.95

1.90

1.85

1.80

LOG10RP

1.75

2

4

6

8

10

12

14

16

OBS

Linear Theil Data

CT

160

150

140

130

120

110

Y

100

90

80

70

RP

60

2

4

6

8

10

OBS

Figure 6.1 2 D Plots of Textile Data

31

12

14

16

Econometric Notes

Two dimensional plots of this dataset do not capture the full relationships. From the plots in Figure

6.1 it appears that the consumption of textiles increases when the relative price of textiles falls and

that RI has little effect. Figure 6.2, which is based on a three dimensional extrapolation about each

point, gives a better picture of the true relationship. This figure clearly shows that LOG10RP, has the

most effect on LOG10CT, which is on the Z axis, but that LOG10RI does have a positive effect. The

OLS regression model attempts to capture this surface.

Remark: A 2-D plot may lead one to drop a variable that is in fact significant in a multi-dimensional

context. A 3-D plot can help in cases where K=3, but may be less useful for larger problems.

The plots of CT against RP and LOG10CT against LOG10RP suggest a negative relationship, which

is consistent with the economic theory that quantity demanded of a good will increase as its relative

price falls. The correlations between these two sets of variables are negative (-.94664 and -.93596)

and highly significant (at the .0001 level for both correlations). The plot between CT and Y and the

plot between LOG10CT and LOG10Y do not show much of a relationship. The raw correlations are

small (.06177 and .09786, respectively) and not significant. The preliminary finding might be that Y

was not a good variable to use on the right-hand side of a model predicting CT. It will be shown later

that such a conclusion would be wrong.

32

Econometric Notes

Log Theil Textile Data

2.18

l

o

g

1

0

c

t

2.16

2.14

2.12

2.10

2.08

2.06

2.04

2.050

2.040

2.030

2.020

log

1.80

2.010

2.000

1.90

1.990

1.980

10y

2.00

log

10rp

Figure 6.2 3-D Plot of Theil (1971) Textile Data

Remark: The preliminary estimation of a model CT = f(constant, Y, RP) indicates that the

coefficients are 1.0617 (t = 3.98) and -1.383 (t = -16.5), respectively. The results support the

maintained hypothesis that CT is positively related to income and negatively related to relative price.

The Y variable, which was not significantly correlated with CT, was found to be significant when

included in a regression controlling for RP. This demonstrates that it is important to go beyond just

raw cross correlation analysis. If proposed variables are "prescreened out" by correlation analysis and

not tried in regression models, many important variables may be incorrectly dropped from the analysis.

It is important not to prematurely drop a proposed, theoretically plausible, variable from a regression

model specification, even if in preliminary specifications it does not enter significantly. Later in the

paper an example will be presented that illustrates that if other important variables are omitted from

an equation, a significant variable that is in the equation may not show up as significant when other

variables enter the equation omitted variable bias). The preceding discussion suggests that regression

analysis requires careful use of diagnostic tests before the results are to be used in a production

environment.

A possible problem with the above formulation is that the error process might potentially have

heteroskedasticity or nonconstant variance due to the fact that the time series values for CT are

33

Econometric Notes

increasing over time. If all the variables in the model are transformed into logs (to the base 10), some

of the potential for difficulty may be avoided. If heteroskedasticity were to be present, the estimated

standard errors of the coefficients would be biased. In addition, the estimated standard error of the

model, 5.5634 (433.31298/(17.3) from equation (6-4), would be misleading, since it would be

an average, and, assuming the variance of the error was increasing, would overstate the error at the

beginning of the data set and understate the error at the end of the data set.

Log transforms to the base 10 are made and the model is estimated again and reported in the

bottom equation (6-4). The results indicate the log linear form of the model fits better (the adjusted

R 2 now is .9707) and all coefficients, except for the constant, are more significant. Comparison of the

estimated values with the actual values shows surprisingly good results, considering there are only

two explanatory variables in the model.

One of the assumptions of an OLS regression is that the error process follows a random normal

distribution with no serial correlation or heteroskedasticity (nonconstant variance). If the error process

is only normal, the estimated coefficients will be unbiased and the standard errors of the estimated

coefficients will be biased.

Another important assumption of OLS is that the error terms are not related. If et is the error

term of the estimated model, ut is a random error and the model

p

et i et i ut

(6-5)

i 1

is estimated, no autocorrelation up to order K implies that for K , 1, , k are not significant.

First-order serial correlation can be tested by the Durbin-Watson test statistic. If the Durbin Watson

statistic is around 2.0, there is no problem. If it is substantially below (above) 2.0 there is positive

(negative) autocorrelation. This can be seen since the formula for the Durbin Watson is

T

T

t 2

t 1

d (et et 1 ) 2 / et2

(6-6)

If serial correlation is found, the appropriate procedure is generalized least squares, which involves a

transformation of the data. If heteroskedasticity is found, there are other procedures that can be used

to remove the problem. To illustrate GLS, assume

yt xt et

(6-7)

where t refers to the time period of the observation. If 1 and model (6-5) is estimated for the

residuals for (6-7) and 1 is significant, the appropriate procedure is to lag the original equation and

34

Econometric Notes

multiply through by 1 and then subtract from the original equation. This would give

( yt 1 yt 1 ) (1 1 ) ( xt 1 xt 1 ) (et 1et 1 )

(6-9)

which will give unbiased estimates of and and their standard errors, since from (6-5)

ut et 1et 1 and by assumption ut does not contain serial correlation.

As a test a misspecified model (to induce serial correlation) containing only LOG10Y is run in

SAS. This model will find LOG10Y not significant and evidence of serial correlation in the model as

measured by the low Durbin-Watson test statistic (.241). In the presence of serial correlation, the best

course of action is to attempt to add new variables to explain the serial correlation. The B34S reg

command output is shown first and next the SAS autoreg command

REG Command. Version

1 February 1997

Real*8 space available

Real*8 space used

9000000

43

OLS Estimation

Dependent variable

Adjusted R**2

Standard Error of Estimate

Sum of Squared Residuals

Model Sum of Squares

Total Sum of Squares

F( 1,

15)

F Significance

1/Condition of XPX

Number of Observations

Durbin-Watson

Variable

LOG10Y

{

CONSTANT {

0}

0}

LOG10CT

-5.645122564288263E-02

8.131550225838252E-02

9.918316361299519E-02

9.590596648930139E-04

0.1001422232778882

0.1450437196128150

0.2913428904662156

1.523468705487359E-05

17

0.2414802718079813

Coefficient

0.34782649

1.4222303

Std. Error

0.91329943

1.8378693

t

0.38084606

0.77384737

SAS output next:

The AUTOREG Procedure

Dependent Variable

LOG10CT

LOG10 OF CONSUMPTION

Ordinary Least Squares Estimates

SSE

MSE

SBC

Regress R-Square

Durbin-Watson

0.00256758

0.0001834

-92.822527

0.9744

1.9267

DFE

Root MSE

AIC

Total R-Square

Variable

DF

Estimate

Standard

Error

t Value

Approx

Pr > |t|

Intercept

LOG10Y

LOG10RP

1

1

1

1.3739

1.1432

-0.8288

0.3061

0.1560

0.0361

4.49

7.33

-22.95

0.0005

<.0001

<.0001

35

14

0.01354

-95.322167

0.9744

Variable Label

LOG10 OF INCOME

LOG10 OF RELATIVE PRICE

Econometric Notes

Estimates of Autocorrelations

Lag

Covariance

Correlation

0

1

0.000151

-0.00001

1.000000

-0.093221

-1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

|

|

|********************|

**|

|

Preliminary MSE

0.000150

Estimates of Autoregressive Parameters

Lag

Coefficient

Standard

Error

t Value

1

0.093221

0.276142

0.34

Algorithm converged.

The SAS System

10:37 Wednesday, December 6, 2006

4

The AUTOREG Procedure

Maximum Likelihood Estimates

SSE

MSE

SBC

Regress R-Square

Durbin-Watson

0.0025352

0.0001950

-90.189374

0.9789

1.7932

DFE

Root MSE

AIC

Total R-Square

Variable

DF

Estimate

Standard

Error

t Value

Approx

Pr > |t|

Intercept

LOG10Y

LOG10RP

AR1

1

1

1

1

1.3592

1.1487

-0.8271

0.1248

0.2941

0.1516

0.0343

0.3186

4.62

7.58

-24.09

0.39

0.0005

<.0001

<.0001

0.7017

13

0.01396

-93.522227

0.9747

Variable Label

LOG10 OF INCOME

LOG10 OF RELATIVE PRICE

Autoregressive parameters assumed given.

Variable

DF

Estimate

Standard

Error

t Value

Approx

Pr > |t|

Intercept

LOG10Y

LOG10RP

1

1

1

1.3592

1.1487

-0.8271

0.2875

0.1471

0.0338

4.73

7.81

-24.47

0.0004

<.0001

<.0001

The SAS System

Variable Label

LOG10 OF INCOME

LOG10 OF RELATIVE PRICE

10:37 Wednesday, December 6, 2006

The AUTOREG Procedure

Dependent Variable

LOG10CT

LOG10 OF CONSUMPTION

Ordinary Least Squares Estimates

SSE

MSE

SBC

0.09918316

0.00661

-33.537669

DFE

Root MSE

AIC

36

15

0.08132

-35.204096

5

Econometric Notes

Regress R-Square

Durbin-Watson

0.0096

0.2415

Total R-Square

0.0096

Variable

DF

Estimate

Standard

Error

t Value

Approx

Pr > |t|

Intercept

LOG10Y

1

1

1.4222

0.3478

1.8379

0.9133

0.77

0.38

0.4510

0.7087

Variable Label

LOG10 OF INCOME

Estimates of Autocorrelations

Lag

Covariance

Correlation

0

1

0.00583

0.00447

1.000000

0.765305

-1 9 8 7 6 5 4 3 2 1 0 1 2 3 4 5 6 7 8 9 1

|

|

|********************|

|***************

|

Preliminary MSE

0.00242

Estimates of Autoregressive Parameters

Lag

Coefficient

Standard

Error

t Value

1

-0.765305

0.172027

-4.45

Algorithm converged.

The SAS System

10:37 Wednesday, December 6, 2006

6

The AUTOREG Procedure

Maximum Likelihood Estimates

SSE

MSE

SBC

Regress R-Square

Durbin-Watson

0.02423721

0.00173

-53.034484

0.0564

1.6157

DFE

Root MSE

AIC

Total R-Square

14

0.04161

-55.534124

0.7580

Variable

DF

Estimate

Standard

Error

t Value

Approx

Pr > |t|

Intercept

LOG10Y

AR1

1

1

1

0.6643

0.7229

-0.8961

1.6320

0.8167

0.1312

0.41

0.89

-6.83

0.6901

0.3910

<.0001

Variable Label

LOG10 OF INCOME