less8act16-Week_8

advertisement

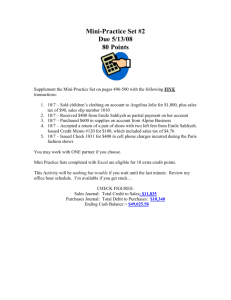

Week 8 Using an expanded journal is not practical or efficient as the amount of transactions grows. Special journals that capture a specific type of transaction can be used. The journalizing effort can be shared among multiple bookkeepers/accounting clerks. The posting effort can be shared among multiple bookkeepers/accounting clerks. There are several special journals, the business decides which it will use. Transaction: purchase by business of merchandise on account ONLY! Debit Purchases/Credit Accounts Payable Need to identify the vendor Purchase Requisition: submitted by business department “requesting” something. Usually sent to purchasing department. Purchase Order: prepared by purchasing department and sent to vendor. Purchase Invoice: prepared by vendor and sent to business. Identifies products, quantities, amount due, terms of sale. Packing Slip: accompanies shipment. Identifies contents shipped. Transaction: any cash payments made by business recorded in this journal. Source document is usually a check. Anytime business spends cash/money. Offered by vendor to encourage early payment of invoice. Terms: 2/10, n/30 translates to 2% off if paid within 10 days of invoice date otherwise net (full) amount due in 30 days. Business can reduce amount they have to pay on invoice. Amount of reduction known as a purchase discount. Amount is reflected in an account known as Purchases Discount. Purchases Discount has normal credit balance. It affects the Purchases account which has a normal debit balance. So, Purchases Discount reduces the account it affects, namely Purchases. So, Purchases Discount is referred to as a “contra” account since it runs contrary to or opposite the account if affects. Recall, the business has an accounts payable at the full amount that they owe however they end up paying less than they owe so Purchases Discount reflects that difference. Business purchases $2,000 worth of merchandise on account. Terms of sale are 2/10, n/30. Business pays within 10 days so they can take discount. $2,000 * .02 = $40 discount on purchase. Business pays $2,000 - $40 = $1,960 to vendor. How is this payment journalized? Debit Accounts Payable full amount $2,000 Credit Cash $1,960 to reflect payment Credit Purchases Discount $40 to reflect discount $2,000 debit = $1,960 credit + $40 credit Debits = Credits, which is what we want! Recognize that not all transactions can be entered in a special journal so the business will maintain a general journal to act as a catch all for transactions that can not be journalized in a special journal. Purchase Returns: business sends product back to the vendor. Purchase Allowance: business keeps shipment but vendor grants allowance so business pays less than invoice. Business will prepare a debit memorandum to send to vendor identifying the amount of the debit or reduction to their Accounts Payable. Debit memo will be source document for these return and allowance transactions. Business captures the return or allowance amount in an account known as Purchases Returns and Allowances As with Purchases Discounts this lets business track returns and allowances in place of crediting the Purchases account. Purchases Returns and Allowances (PRA) has normal credit balance. It affects the Purchases account which has a normal debit balance. So, PRA reduces the account it affects, namely Purchases. So, PRA is referred to as a “contra” account since it runs contrary to or opposite the account if affects. To journalize a return you DEBIT Accounts Payable/Vendor the amount of the return and CREDIT Purchases Returns and Allowances the amount of the return. To journalize an allowance you DEBIT Accounts Payable/Vendor the amount of the allowance and CREDIT Purchases Returns and Allowances the amount of the allowance. These contra accounts are used so the Purchases account is not affected with credits.