Document

advertisement

Chapter 9

Policy Tools for

Macroeconomic Analysis

© Pierre-Richard Agénor

The World Bank

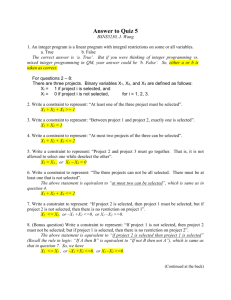

1

Assessing Business Cycle Regularities

Assessing the Effects of External Shocks

Financial Programming

The Polak Model

An Extended Framework

The World Bank RMSM Model

The Merged Model and RMSM-X

Three-Gap Models

Lags and Behavioral Functions

2

Assessing Business Cycle

Regularities

3

Little attention paid to developing countries in recent

past:

Why?

Limited data quality and frequency.

Cycle-spotting problematic; prone to sudden

crises.

4

Analysis of macroeconomic fluctuations beneficial:

Helps specify applied macroeconomic models that

capture some of the most important correlations.

Unconditional correlations can provide insight to

the type of shocks that dominate fluctuations in

some macroeconomic aggregates

Design of stabilization programs; insight gained in

assessing pattern of leads and lags between

aggregate time series and economic activity.

5

Four Step Process

Step 1: choose a measure of real activity

Step 2: decompose all series into trend and cyclical

components.

Step 3: assess comovement of series with

measure of real activity (output).

Step 4: determine phase shift of series with respect

to output.

6

Step 1: choosing a measure of real activity

Real GDP often chosen.

Can be inappropriate:

Agricultural output, frequently contingent on nonmacroeconomic variables (e.g. weather

conditions) comprises a large percentage of

GDP.

Nonagricultural output may be a preferable

measure in select developing countries.

Figure 9.1.

7

F

i

g

u

r

e

9

.

1

a

S

t

r

u

c

t

u

r

e

o

f

O

u

t

p

u

t

(

V

a

l

u

e

a

d

d

e

d

,

i

n

p

e

r

c

e

n

t

o

f

G

D

P

)

A

g

r

i

c

u

l

t

u

r

e

I

n

d

u

s

t

r

y

S

e

r

v

i

c

e

s

Af

Beni n

1

9

8

0

Bang

1

9

9

5

1

9

8

0

Bur undi

1

9

9

5

1

9

8

0

l ade

Indi a

1

9

9

5

1

9

8

0

1

9

9

5

9

8

0

C amer1

oon

1

9

9

5 Indones

1

9

8

0 i

1

9

9

5

9

8

0

C ôte

d'1

Iv

oi r e

1

9

9

5

9

8

0

Kor ea 1

1

9

8

0

Ethi opi

a

1

9

9

5

1

9

9

5

1

9

8

0

s

ia

1

9

8

0 M al ay

G hana

1

9

9

5

1

9

9

5

Keny

a

1

9

8

0

1

9

9

5

N epal

1

9

8

0

1

9

9

5

1

9

8

0

M al aw

i

1

9

8

0

i s tan

1

9

9

5 Pak

1

9

9

5

1

9

8

0

N i g er i

a

1

9

9

5

1

9

8

0

Phi l i ppi

n

1

9

9

5

1

9

8

0

T anz ani

a

1

9

9

5

1

9

8

0

Lank

a

1

9

8

0 Sr i

1

9

9

5

Z ambi a

1

9

9

5

1

9

8

0

1

9

8

0 T hai l and

Z i mbabw

e

1

9

9

5

1

9

9

5

0

24

0

6

0

8

0

1

0

0

0

24

0

6

0

8

0

1

0

00

S

o

u

r

c

e

:

W

o

r

l

d

B

a

n

k

.

8

F

i

g

u

r

e

9

.

1

b

S

t

r

u

c

t

u

r

e

o

f

O

u

t

p

u

t

(

V

a

l

u

e

a

d

d

e

d

,

i

n

p

e

r

c

e

n

t

o

f

G

D

P

)

A

g

r

i

c

u

l

t

u

r

e

I

n

d

u

s

t

r

y

L

a

t

i

n

A

m

e

r

i

c

a

S

e

r

v

i

c

e

s

M

i

d

d

l

e

E

a

s

t

a

n

d

N

o

r

t

h

A

f

r

i

c

a

A

r

g

e

n

t

i

n

a

1

9

8

0

1

9

9

5

A

l

g

e

r

i

a

1

9

8

0

1

9

9

5

B

o

l

i

v

i

a

1

9

8

0

1

9

9

5

E

g

y

p

t

1

9

8

0

1

9

9

5

B

r

a

z

i

l

1

9

8

0

1

9

9

5

J

o

r

d

a

n

C

h

i

l

e

1

9

8

0

1

9

9

5

1

9

8

0

1

9

9

5

M

a

u

r

i

t

a

n

i

a

1

9

8

0

1

9

9

5

1

9

8

0

1

9

9

5

1

9

8

0M

o

r

o

c

c

o

1

9

9

5

1

9

8

0

1

9

9

5

E

c

u

a

d

o

r

1

9

8

0

1

9

9

5

O

m

a

n

1

9

8

0

1

9

9

5

J

a

m

a

i

c

a

1

9

8

0

1

9

9

5

S

y

r

i

a

M

e

x

i

c

o

1

9

8

0

1

9

9

5

1

9

8

0

1

9

9

5

1

9

8

0

1

9

9

5

T

u

n

i

s

i

a

P

e

r

u

1

9

8

0

1

9

9

5

T

u

r

k

e

y

1

9

8

0

1

9

9

5

Y

e

m

e

n

1

9

8

0

1

9

9

5

C

o

l

o

m

b

i

a

C

o

s

t

a

R

i

c

a

U

r

u

g

u

a

y

1

9

8

0

1

9

9

5

V

e

n

e

z

u

e

l

a

1

9

8

0

1

9

9

5

02

04

06

08

01

0

0

S

o

u

r

c

e

:

W

o

r

l

d

B

a

n

k

.

02

04

06

08

01

0

0

9

Step 2: nonstationary and stationary components

Augmented Dickey-Fuller (ADF) test

Most techniques rely on stationary (cyclical)

data.

ADF: test for unit roots.

xt = + t + ( - 1)xt-1 + h xt-h + ut

ut : error term;

k 0;

For xt to be stationary, - 1 should be negative

and significantly different from zero.

10

Step 2: nonstationary and stationary components.

Given

xt = xt* + xtc,

xt* : trend component

xtc : cyclical component

Hodrick-Prescott (HP) filter can be used to

estimate and filter the trend component, xt*.

Criticism of HP filter:

removes potentially valuable information and

may impart spurious cyclical patterns to data;

assumes independent relationship between

trend and cyclical components.

11

Step 3: assessing the comovements

Contemporaneous correlation coefficient, (0),

between filtered components of yt (series) and xt

(output):

Procyclical if (0) is positive.

Countercyclical if (0) is negative.

Acyclical if (0) is zero.

With 10% significance threshold, series yt is;

Strongly contemporaneously correlated:

.3 (0)< 1.

Weakly contemporaneously correlated:

.1 (0)< .3.

12

Contemporaneously uncorrelated:

0 (0)< .1.

Step 4: determining the phase shift

Phase shift of yt relative to output: crosscorrelation coefficients, (j), j {+/-1,+-2,…}:

yt leads the cycle by j period(s) if (j)is

maximum for a negative j;

yt lags the cycle if (j) is maximum for a

positive j;

yt is synchronous if (j) is maximum for j = 0.

13

Table 9.1: results for Kenya and Venezuela,

private consumption, investment and private sector

credit are procyclical but less volatile than output;

fiscal stance is countercyclical in Kenya,

procyclical in Venezuela;

trade ratio is countercyclical in Venezuela;

broad money seems to lag movements in activity;

terms of trade is countercyclical in Venezuela;

inflation is countercyclical.

14

Assessing the Effects of

External Shocks

15

McCarthy, Neary, and Zanalda (1994)

Step 1: estimate impact of three components on BOP,

expressed as a percentage of output.

Terms of trade, interest rate effect, changes in

global demand.

Terms of trade shock: measured as the market

value of the net import effect.

Interest rate effect: change in world interest

rates multiplied by stock of interest rate sensitive

external debt.

Changes in global demand: deviation of growth

of world export volumes from estimated trend

multiplied by initial export volume.

16

McCarthy, Neary, and Zanalda (1994)

Step 2: estimate economy’s response to shocks.

Level of demand: adjustment in imports from

reduction in aggregate demand; difference

between expected import volumes using

historical import elasticity of GDP using trend

growth versus actual GDP growth.

Expenditure-switching measures: captured by

changes in export performance and the degree

of import intensity.

Step 3: calculate additional net external financing

as the difference between the effect of all shocks

and the economy’s responses.

17

Financial

Programming

The Polak Model

An Extended Framework

18

The Polak Model

19

Considers small open economy, with fixed exchange

rate.

Four Equations:

Ms = L + R (4)

Ms: money supply, L: domestic credit, R :

official foreign exchange reserves

R = X - Y + F, 0 < < 1, (5)

F: capital inflows

Md = v-1Y, v > 0, (6)

20

v: income velocity of money

Ms = Md (7)

Polak focus:

Determine effects of changes in domestic credit on

foreign exchange reserves.

Using (4), (6), and (7),

R = v-1Y - L .

Reserves will only increase when nominal money

demanded exceeds change in domestic credit.

21

Polak model structure:

Target Variables: R.

Endogenous Variables: M, Y, J = Y.

Exogenous Variables: X, F.

Policy Instruments: L.

Parameters: v, .

22

Polak example:

Consider increase in L at period t = 0, by L0 ,

s

M rises by L0, by (4),

d

M rises by L0 , by (7),

nominal income, Y, must rise, by vL0, by (6),

thus, imports rise by Y = vL0,

reserves fall -vL0 on impact,

s

M then increases only (1 - v)L0 .

23

Consider increase in L at period t = 0 by L0 ,

cumulated fall in reserves at end of period 1:

Rt=1 = -vL0 - v(1 - v)L0,

over an infinite time horizon (t ):

Rt = -L0 ,

in long run, initial expansion in money supply via

increase in domestic credit is completely offset by

the reduction in official reserves.

24

Domestic credit expansion levels crucial in

obtaining BOP objective:

note: exports, capital flows and income velocity

of money treated as exogenous variables.

Given a targeted level of reserves,

L =

v-1Yp

~

- R

R: targeted reserves,

Yp: projected level of nominal income

L: required change in credit, allows policy makers

to estimate a credit ceiling.

25

Monetary Approach to the Balance of Payments

(MABP):

Assumptions:

stable demand for money,

purchasing power parity,

continuous stock equilibrium in money markets

Results in an instantaneous absorption by reserves

of credit change, unlike Polak which assumes a more

gradual absorption.

26

Limitations of the Polak Model:

Assumes that changes in domestic credit have no

effect on domestic money demand; in many

developing countries the bank credit-supply side link

is a critical feature of the economy.

Assumes a stable money demand function; in

practice money demand tends to be unstable as a

result of volatile inflation expectations.

27

An Extended Framework

28

Khan, Haque, and Montiel (1990)

Distinguishes between real and nominal output and

the sources of credit growth.

Extended framework equations:

Consider single good economy where,

Y = Py

Y: nominal income, P: overall price index, and

y: real output.

Y = Py-1 + P-1y

29

Price changes: function of domestic price changes,

PD and exchange rate adjusted foreign prices

changes by,

P = PD + (1 - )(E + P*), 0 < <1

Domestic credit

L = Lp + Lg,

Lp : private sector credit

Lg : government credit

Lp : f(demand for working capital), proportional to

changes in nominal output:

Lp =

Y;

30

Money supply identity:

M = L + R;

with

R = ER*

R = X - J + F

X: Exports (exogenous); J: Imports in nominal terms,

J = EQJ,

QJ : import volume; E : nominal exchange rate

31

Changes in import volume, related to the change in

output and the relative price of foreign goods,

QJ = y + [PD - (E + P*)]

> 0: import elasticity to relative price changes.

Nominal value of imports:

J = J-1 + (QJ-1 - E-1)E

+ E-1[y + (PD - P*)] (16)

32

With relatively small QJ-1, a devaluation in the

nominal exchange rate (E > 0) will lower the

nominal value of imports, improve the trade balance

and increase official reserves.

Income velocity: constant as in Polak model, money

market assumed to be in flow equilibrium.

Government Budget Constraint: G - T = L + Fg,

budget deficit is financed by foreign borrowing or

changes in central bank credit.

33

Structure of Extended Framework:

Target variables: R, PD

Endogenous variables: Y, Lp, M, P, J, G-T

Exogenous variables: y, P*, X, F = Fp + Fg

Policy instruments: Lg, E

Predetermined: y-1, P-1, QJ-1

Parameters: v, , , , .

34

Target variable equations:

R = (v-1 - )y - 1 PD =

(20)

with

= (v-1 - )[y-1(1 - )(E + P*) + P-1y]

-Lg.

R + PD = X + F - J-1 + (QJ-1 - E-1)E

+ P* - E-1y

(21)

35

Positive and programming mode solutions

Positive Mode: for given values of exogenous

variables and policy instruments, determine

simultaneously the target variables.

Programming Mode:

~

~

R, PD are targets and equations are solved for

the policy instruments, Lg, E.

See Figure 9.2 for graphical representation of (20)

and (21) in R-PD space as the MM and BB curves

respectively.

36

F

i

g

u

r

e

9

.

2

T

h

e

E

x

t

e

n

d

e

d

F

i

n

a

n

c

i

a

l

P

r

o

g

r

a

m

m

i

n

g

M

o

d

e

l

R

B

~

E

'

M

R

E

M

B

~

P

D

S

o

u

r

c

e

:

A

d

a

p

t

e

d

f

r

o

m

K

h

a

n

,

M

o

n

t

i

e

l

,

a

n

d

H

a

q

u

e

(

1

9

9

0

,

p

.

1

6

1

)

.

P

D

37

Programming Mode

Given the objective of lowering inflation and

increasing official reserves, policymakers can,

g

reduce L , shift MM curve left in Figure 9.2, or

depreciate the nominal exchange rate, shift MM

left and BB right in Figure 9.2.

38

The World Bank RMSM

Model

39

Revised Minimum Standard Model:

Precursor to the RMSM-X model.

Developed in the early 1970s.

Objective: make explicit the link between mediumterm growth and its financing.

40

Five relationships (prices taken as given):

I = y/

(22)

: incremental capital-output ratio (ICOR).

Imports:

J = y, 0 < < 1

Cp = (1 - s)(y - T),

(23)

(24)

0 < s < 1: marginal propensity to save.

41

Balance-of-payments identity:

R = X - J + F

(25)

National income identity:

y-1 + y = Cp + G + I + (X - J)

(26)

42

The structure of RMSM:

Target Variables: R, y.

Endogenous Variables: I, Cp, J.

Exogenous Variables: X .

Policy Instruments: G, T, F

Predetermined: y-1

Parameters: , s, .

43

Target equations:

(s + )y-1 + (1 - s)T - (X + G)

y =

-1 - (s + )

(27)

Substituting (23) in (25),

R = X - (y-1 + y) + F. (28)

44

Solutions:

Positive or Policy Mode

Recursive: first equation can be used to determine

second equation.

See Figure 9.3: for given values of exogenous

variables and policy instruments, equilibrium is

found at the interception of the horizontal YY curve

and the BB curve, equations (27) and (28)

respectively.

45

F

i

g

u

r

e

9

.

3

T

h

e

R

M

S

M

M

o

d

e

l

i

n

t

h

e

P

o

s

i

t

i

v

e

M

o

d

e

yB

Y

E

Y

B

R

46

Programming Mode:

Trade-gap mode: Given X-J, calculates F in (25).

Saving-gap mode: Given X-J and F, calculates

~

required level of savings, y/

in (22).

Total consumption assumed to be a residual of

national income identity (26),

Cp = y-1 + y - y/ - X - m(y-1 + y) - G

Limitation: priori expectation that private

consumption will be consistent with national

accounts identity unrealistic.

However, possible to use trade sap and saving

gap as potentially binding constraints.

47

Two-Gap Mode:

Determine financing requirements for alternative

target rates of output growth and official reserves.

Determine feasibility of particular growth rate given

alternative financing scenarios.

Saving Constraint:

Begin with national income accounting identity,

I = (y - T - Cp) + (T - G) + (J - X) (30)

(y - T - Cp): private sector savings;

(T - G) : public sector savings;

(J - X ): foreign savings.

48

Saving Constraint:

p

Substituting out for C and J - X,

I S + F (31)

with,

~

S = s(y-1 + y) + [(1 - s)T - G] - R.

~

Figure 9.4: graphs inequality in I-F space.

49

F

i

g

u

r

e

9

.

4

T

h

e

R

M

S

M

M

o

d

e

l

i

n

T

w

o

G

a

p

M

o

d

e

I

T

Z

o

n

e

I

I

S

Z

o

n

e

I

V

Z

o

n

e

I

4

5

º

Z

o

n

e

I

I

I

S

T

F

50

Trade Constraint:

Rewrite (25) as,

~

J - X = F - R. (32)

Substitute (23) into (32),

y = (X - R + F)/ - y-1. (33)

Trade constraint: substitute (33) into (22),

I T + F/ (34)

with,

T = (X - R)/ - y-1/

51

RMSM: Two Gap Mode

Binding constraint: constraint yielding lowest level

of investment.

Suppose foreign financing is binding constraint.

Other variables solved for using iterative

process:

Step 1: Specify values for a) parameters, , s, and

; b) predetermined variable, y-1;

c) exogenous variables, X and F; d) policy

~

~

instruments, T and G; e) policy targets, y and R.

Step 2: given target output, determine required

investment,

~

IR = y/

52

Step 3: Determine the levels of investment, IS and

IT implied by the saving constraint (31),

Imin = min(IS , IT).

Step 4: If Imin IR, no constraint is binding.

4a: If Imin IR, and if savings constraint is

binding

either increase taxes, T, and/or reduce G,

~

and/or reduce R, until constraint is relaxed

or you have exhausted policy instrument

options.

53

4b: If Imin IR and if trade constraint is binding

~

reduce R, until constraint is relaxed or

further policy or target variable changes

unfeasible.

4c: If Imin IR and both constraints are binding:

~

reduce R and/or adjust T and G.

Step 5: If adjustments in step four do not still satisfy

constraints, lower desired level of output by,

y = Imin

~

54

Step 6: determine required level of imports as

JR = (y-1 + y)

Step 7: now, given JR, X, and F, recalculate target

level of reserves as,

~

R[1] = X - JR + F,

~

~

redo iterations in step 3-8 until R[1] R.

55

Step 8: Once convergence has been achieved,

model yields inter-related consistent values of the

levels of investment, the change in output, imports,

and the change in official reserves.

Step 9: Use equation (24) along with the new value

of output and the value of taxes to estimate private

consumption, Cp.

56

Three criticisms:

Difficulty identifying binding constraint a priori.

Assumes imports as essential for investment

and growth; however, saving gap can also be

closed by combination of reducing imports or

increasing exports, thereby freeing foreign

exchange necessary for investment.

Incomplete; essentially a growth-oriented model

with emphasis on a small number of real variables

and no financial side.

Relative prices and induced substitution effects

among production factors (and their possible

impact on exports, for instance) are neglected.

57

The Merged Model

and RMSM-X

58

The Merged IMF-World Bank Model

Combines extended model and RMSM model.

As in extended model, relative prices affect imports

and domestic absorption.

Equations:

Changes in real output,

y = I/(1 + P),

Y = Py-1 + P-1y,

P = PD + (1 - )E,

P* = 0

59

Domestic credit

L = Lp + Lg,

with

Lp = Y.

Money supply identity

M = L + R,

with

R = ER*

60

Balance of payments:

R = X - J + F,

with

F = (1 + E)F*,

X: exogenous.

Nominal imports:

J = J-1 + (QJ-1 - E-1)E + E-1(y + PD).

61

Money demand:

Md = v-1Y.

Flow equilibrium of the money market:

Ms = Md

62

Government budget constraint:

G - T = Lg + Fg.

Private Sector Budget Constraint:

(Y - Cp - T) - I = Md - Lp - Fp

Cp = (1-s)(y - T), private sector budget constraint

implies,

I = s(Y-1 + Y - T) + Lp + Fp - Md. (47)

63

Structure of the merged model:

Target Variables: R,PD, y

Endogenous Variables: Y, Lp, M, P, J, G-T

Exogenous Variables: X, F = Fp + Fg

Policy Instruments: Dg, E, G or T

Predetermined: y-1, P-1

Parameters: , , , , .

64

Target equations: merged model

PD =

- + (-1 - )y

y-1

- (1 - )-1E

R + (y-1PD + y) =

R = X - J-1 - (QJ-1 - E-1)E

- E-1(y + PD) + F

Figure 9.5.

65

F

i

g

u

r

e

9

.

5

T

h

e

M

e

r

g

e

d

I

M

F

W

o

r

l

d

B

a

n

k

M

o

d

e

l

y

M

Y

~

A

'

B

y

A

E

'

E

B

Y

P

D

~

P

D

M

~

R

R

66

The RMSM-X Framework

Expanded version of the RMSM model (see

World Bank, 1997b):

Conceptual basis: merged IMF-World Bank model

described earlier (adds to the RMSM model a price

sector, a monetary sector, and government accounts,

along the lines of the financial programming

approach.

In practice, RMSM-X models fairly detailed;

General RMSM-X model characteristics: often consist

of four economic sectors: the public sector, the

private sector, the consolidated banking system, and

the external sector.

67

Budget constraints associated with each sector.

National accounts derived via aggregation of the

sectoral budget constraints serve to close the RMSMX model.

Two types of financial assets, money and foreign

assets in standard model, some versions include

(particularly for middle-income countries) domestic

bonds.

Money demand function frequently follows Polak

model; constant income velocity of money.

68

Some models disaggregate banking system

structure: here Ms is not equal to the sum of central

bank credit and official reserves; rather obtained as

the product of the monetary base and a constant

money multiplier.

Prices: assume domestic and foreign goods are

imperfect substitutes, so that substitution effects can

be analyzed on the demand side.

Imports: several categories with the demand a

function of the real exchange rate and either real

GDP or (e.g. imports of capital goods) gross domestic

investment.

69

Consumption: generally assumed to depend only

on disposable income---thereby excluding

consumption-smoothing effects.

Model closures:

Public sector closure: values for all variables

except public sector expenditure and domestic

borrowing specified; latter two variables then

determined by model.

Private sector closure: values for government

expenditure and revenue are specified, and the

model estimates private sector variables.

70

Marginal economic agent:

In both approaches, likely disbursements from

external donors provide estimate of external

financing.

External borrowing requirements determined

separately, through the balance-of-payments

identity.

Gap financed by marginal economic agent.

In public sector closure, central government is

marginal borrower and foreign commercial banks

are assumed to be the marginal foreign creditor.

71

Policy closure as availability mode: all external

financing identified in advance and imports are

adjusted to equilibrate BOP.

Programming Mode:

targeted values given;

RMSM-X then solved for mix of fiscal,

monetary and exchange rate policies consistent

with targeted values.

72

Programming mode: solution sequence

Step 1: set targets for inflation rate, potential GDP

growth rate (evaluated at full employment), real

exchange rate, real interest rate, and international

reserves (specified in months of imports).

Step 2: Calculate investment requirements, given

estimates of ICOR and the actual growth rate of

output.

Step 3: Calculate the demand-side relationships

based on the projections of the exogenous

variables.

73

Step 4: Estimate likely availability of foreign

borrowing. Calculate reserve requirements for

exogenously determined import target. Determine

additional foreign borrowing required.

Step 5: Determine growth rate of money supply,

given inflation targets, output growth, estimates of

velocity and the money multiplier. Estimate,

residually, amount of domestic credit supplied by

the central bank or banking system, given the

reserve accumulation target.

74

Step 6: Close the model by determining the

following residuals in the relevant markets:

consumption of goods and services, that is, public

(private) consumption in the public (private) sector

closure; borrowing from the foreign external sector;

and credit allocated by the banking system (or, in

more specific cases, central bank credit to the

nonfinancial public enterprises).

Limitations

Retains limitations of the two models that underlie

it.

IMF framework rudimentary; static nature

problematic for short-term projections, given the

importance of lags.

75

Missing important features of developing countries:

effect of debt financing of fiscal deficit on

domestic interest rates as well as the

endogeneity of private capital flows ignored;

short-run link between production and bank

credit ignored, obviating a critical channel

through which monetary policy can affect the real

economy.

Supply-side problems:

Not account for the complementarity between

public investment and private investment.

Fixed-coefficient production function (the ICOR

relationship) remains subject to a number of

76

analytical and practical difficulties.

Easterly (1999) found that the assumed

linear relationship between growth and

investment is significantly rejected by the

data.

ICOR rules out capital-labor substitutability and is

unable to account for observed fluctuations in real

wages.

Relative prices (and the real exchange rate)

influence the allocation of resources only through

the demand side, not the supply side.

No role to expectations.

No explicit role for the labor market, unable to

account for fluctuations in unemployment.

77

Three-Gap Models

78

Two gap RMSM approach extended to three-gap

framework by Bacha (1990).

Addition of fiscal gap links foreign exchange

availability directly to the rate of growth of

productive capacity and only indirectly to the actual

level of real output.

79

Equations:

ICOR relationship:

I = y/,

80

Setting up the foreign exchange constraint:

JK = I,

XN = X - (J - JK),

XN: level of exports net of noncapital imports.

FN : F minus changes in foreign exchange

reserves, R.

OS : net factor serves to rest of world (external debt

services and other transfers)

81

Standard BOP identity,

R = (X - J) - OS + F.

Substitute, FN = F - R, and X = XN + J - JK,

rearrange,

FN - OS + (XN - JK) = 0.

Solve for JK, then substitute I = JK/ ,

I = (XN + H)/

with

H = FN - OS .

82

Suppose (non-capital) imports are invariant and there

is an upper bound on exports, XN, based on external

demand.

First gap: foreign exchange constraint,

~

I (XN + H)/

83

Setting up the saving constraint:

Using (58), basic national income identity is written

as,

I = (y - Cp - G) + H,

equivalently,

I = Sp + (T - G) + H

with

Sp = y - T - C,

decomposes financing of investment into domestic

and public sector savings.

84

Cp: assume exogenous.

~

~

p

S =y

- Cp

with y bounded from above by full capacity output.

Second gap: saving constraint

~

I Sp + (T - G) + H

Setting up the fiscal constraint:

Suppose:

money money is only asset available;

foreign capital inflows serve to finance

government’s budget deficit.

85

Private sector budget constraint can be written as

Sp - Ip = M/P.

Assume constant real money balances.

M/P: measures both seigniorage and inflation tax.

Revenue generated as function of inflation rate,

P/P and propensity to hoard, ,

M/P = h(, ).

Budget constraint of the consolidate public sector:

Ig = h(, ) + (T - G) + H.

86

Suppose: private and public investment are

complements:

Ip Ig,

: ratio of private to public investment in capital stock.

Ig + Ig = I,

(1 + ) Ig = I

Third gap: fiscal constraint

I (1 + )[h(, ) + (T - G) + H]

87

Model without fiscal constraint

Consider changes in level of foreign financing, H,

in presence of foreign exchange and savings

constraints.

Figure 9.6:

Foreign exchange and saving constraint graphed

in I-H space as FF and SS respectively.

Slope of SS is unity, whereas slope of FF is 1/.

Three cases considered:

*

Case 1: if net foreign inflows H are equal to H

(where FF and SS curve intersect), both

constraints are binding and investment is equal to

I* .

88

F

i

g

u

r

e

9

.

6

T

h

e

T

h

r

e

e

G

a

p

M

o

d

e

l

I

F

(

1

+

)

[

h

(

,

)

+

(

T

G

)

]

G

S

I

*

G

S

~

p

S

+

(

T

G

)

~

X

/

F

0

H

*

H

S

o

u

r

c

e

:

A

d

a

p

t

e

d

f

r

o

m

B

a

c

h

a

(

1

9

9

0

,

p

.

2

9

1

)

.

89

Case 2: if H is less than H*, only FF binds.

Investment determined by foreign exchange

availability.

Economy suffers from excess capacity with

actual output given by,

~

y = Cp + G + (1 - )Ic + XN

Ic: foreign exchange constrained investment.

90

Case 3: if H exceeds H*, the economy will be

constrained by domestic saving:

Output at full capacity;

actual value of adjusted exports will be less than

maximum value, given by foreign demand;

domestic demand ‘squeezes’ exports to

~

XN = y - Cp - G + (1 - )Ic

Ic :saving-constrained level of investment

91

Minding the Fiscal Gap

Adding the fiscal gap leads to the following

adjustments:

In Figure 9.6, add GG curve with slope 1 + and

vertical intercept, (1 + )[h(, ) + (T - G)].

Curves GG and SS have same slope.

Relative heights depend on the values of and . As

long as Ip is positive, the private sector budget

constraint, implies that,

~

Sp >

h(, ).

Larger values of and raise the height of GG

relative to SS.

92

Fiscal constraint incorporated in a variety of ways.

Two possibilities:

Inflation as an endogenous variable: Fiscal

constraint serves limited purpose of determining

inflation rate, , necessary for a given level of total

investment.

Inflation as an exogenous policy variable:

GG serves as an independent constraint;

if fiscal constraint does not bind, is slack

variable and Ip is determined residually;

if fiscal constraint does bind, a rise in H will

increase capacity growth. Output will rise,

economy will move to full capacity with lower net

93

exports.

The 1-2-3 Model

94

Developed at the World Bank by Devarajan et al.

(1997),

CGE (computable general equilibrium) models.

1-2-3 captures features of CGE models: highly

disaggregated models (on both the demand and the

supply side) designed to study issues such as the

allocational and distributional effects of domestic and

external shocks (see Bandara, 1991).

Demand side: typically consider several households.

Price rigidities common.

95

Macroeconomic dimension of CGE models:

Closure rules for ensuring identity between

aggregate savings and investment.

Classical rule:investment endogenous and

determined by aggregate saving.

Keynesian rule:investment exogenous and real

wages adjust to establish saving, investment

identity.

Johansen rule: endogenous public or private

consumption equates total saving to exogenous

investment.

96

The Minimal setup:

Small open economy.

Two representative agents: a producer and a

household.

Economy produces two goods: home good and

exportable good, the price of which is fixed on

world markets.

Household consumes an imported good.

Assume:

demand for exportables perfectly elastic;

zero access to capital markets; external equilibrium

at, X - J = 0.

97

Production possibility frontier (PPF):

Defines the maximum achievable combinations of

exportables and nontradables that the economy

can supply, given by,

Y = F(YX, Yns ;)

(71)

with Y assumed fixed (e.g. full employment to all

production factors).

98

Using a constant elasticity of transformation

(CET) function:

Y = [YX + (1 - )YN]1/ ,

with

0 < < 1,

1 < < +.

Elasticity of transformation, ,

1

=

-1

99

Efficient ratio of exportables to nonexportables in

output as:

YX/Yns = h1(PX , PN )

(72)

PN : price of home goods;

PX : price of exportables.

Price of aggregate output:

PY = g1(PX , PN ). (74)

Thus

PYY PXYXs + PNYNS (75)

100

Household consumption function,

Qs = q(Ynd, J; )

(76)

Qs = [YN + (1 - )J]1/ ,

0 < < 1, - < < 1

1

=

1-

: elasticity of substitution.

101

Desired ratio of imported, home goods,

J/Ynd = h2(PJ , PN ).

(77)

Aggregate supply of the composite good and

import, nontradables demand related by,

PQQs PJ J + PNYNd . (80)

Household total income, V,

V = PYY

(81)

102

With all income spent on composite goods,

V PQQd

Equilibrium conditions

Demand and supply of nontradables:

Yns = Ynd

(83)

(84)

Demand and supply of composite goods:

Qs = Qd

(85)

103

Balanced trade:

PJ J - PXYX = 0

(86)

Constraints not independent as in Walras’ Law.

Model satisfies all three identities in the following

equation:

PN(Yns - Ynd) + PQ (Qs - Qd) + PJ J - PXYX

=0

104

Figure 9.7: illustration of the model.

*

*

World prices are normalized to unity, PX = PJ .

Balance of trade constraint shown as 45-degree line

in quadrant 1.

PPF (71) and CPF shown as mirror images with

balanced foreign trade.

Absorption (maximizing (76)) occurs at point of

tangency between isoabsorption curve and

consumption possibility frontier.

105

F

i

g

u

r

e

9

.

7

E

q

u

i

l

i

b

r

i

u

m

i

n

t

h

e

1

2

3

M

o

d

e

l

J

T

r

a

d

e

b

a

l

a

n

c

e

X

=

J

C

B

s

d

Q

=

q

(

J

,

Y

;

N

P

/

P

J

N

d

Y

N

4

5

º

X

P

/

P

X

N

A

M

a

r

k

e

t

f

o

r

h

o

m

e

g

o

o

d

s

s

Y

N

S

o

u

r

c

e

:

A

d

a

p

t

e

d

f

r

o

m

D

e

v

a

r

a

j

a

n

e

t

a

l

.

(

1

9

9

7

,

p

.

1

6

4

)

.

106

Adverse Terms-of-Trade Shock

Suppose import prices, PJ*, increase.

Figure 9.8:

N

P /PJ remains constant;

imports decline;

new equilibrium at lower utility, consumption of both

imports and home goods have declined (e.g. income

and substitution effect);

value of import rises, exports must rise;

real exchange rate must depreciate.

107

F

i

g

u

r

e

9

.

8

A

n

A

d

v

e

r

s

e

T

e

r

m

s

o

f

T

r

a

d

e

S

h

o

c

k

i

n

t

h

e

1

2

3

M

o

d

e

l

J

T

r

a

d

e

b

a

l

a

n

c

e

X

=

J

C

s

d

Q

=

q

(

J

,

Y

;

N

B

B

'

C

'

P

/

P

J

N

d

Y

N

X

4

5

º

P

/

P

X

N

A

'

A

M

a

r

k

e

t

f

o

r

h

o

m

e

g

o

o

d

s

s

Y

N

S

o

u

r

c

e

:

A

d

a

p

t

e

d

f

r

o

m

D

e

v

a

r

a

j

a

n

e

t

a

l

.

(

1

9

9

7

,

p

.

1

6

7

)

.

108

Real exchange rate, depreciate?

Contingent on the elasticity of substitution

between imports and home goods, .

If 0, isoabsorption curves are L-shaped, real

exchange rate will depreciate

If , isoabsorption curves are flat; tangency

with new CPF will occur to the left of initial

equilibrium consumption point, C. Demand for

home goods rises and the real exchange rate

appreciates.

109

Income and substitution effects:

If < 1, the income effect dominates. Reduction in

output of nontradables and an increase in output of

exportables.

Real depreciation:

If > 1, substitution effect dominates. Real exchange

rate appreciates

If = 1, there is no change in either real exchange

rate or production.

110

Investment, Saving, and the Government

Two extensions: government sector and investment

Government imposes tariff on imported goods at rate,

0 < J < 1,

PJ = (1 + J)EPJ*

111

Sales price of composite good, cost of living index,

differs from PQ , by sales tax, 0 < s < 1,

PS , = (1 + s)PQ

and,

PQQs PJ J + PSYNd .

112

Houshold income, V,

V = PYY + PQNTgg + E ·NTfh

NTgg : net transfers from government.

NTfh : net transfers from abroad.

Share of household income used on composite

good,

PSQhd = (1 -sh - V)V,

sh : household savings rate.

113

Government sector:

Government revenues:

T = J EPJ*J + S PQQd + V V

Government savings:

Sg = T - PQG - PQNTgh

Aggregate savings:

S = Sg + sVV

114

Market-clearing conditions:

External balance:

PZ*Z - PX*X - NTfh = 0.

Equality between saving and investment:

PsI = S

115

Lags and Behavioral

Functions

116

Accounting for lags: critical for establishing shortterm projections.

Two types of lags:

Inside lags: legal and institutional delays involved

in implementing a change in policy.

Outside lags: delay involved between

implementation of a policy and its effects on the

target variables.

117

Endogeneity of lags:

often affected by private agents’ expectations

about the sustainability of the various policies;

highly credible policy; with low probability of

reversal may have relatively short lag.

Behavioral functions often difficult to estimate in

countries undergoing comprehensive reform

programs or large shifts in policy.

In this case, use of relatively sophisticated

econometric techniques such as the error correction

framework may not be enough to detect stable

relationships.

118