In the markets: A week of strong gains nearly offset the previous

advertisement

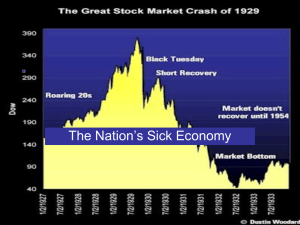

In the markets: A week of strong gains nearly offset the previous week’s sharp losses and brought the LargeCap S&P 500 index back into positive territory for the year. The Dow Jones Industrial Average gained 578 points to end the week at 17,823, a gain of +3.36%. The tech-heavy Nasdaq blew through the 5000-level again, gaining 177 points and closing at 5,104, an improvement of +3.59%. The LargeCap S&P 500 gained +3.27%, the MidCap S&P 400 was up +2.92%, and the SmallCap Russell 2000 was up +2.49%. As has been the case for some time, the SmallCap and MidCap indexes have been unable to match the gains of their LargeCap brethren. Canada’s TSX gained +2.74%, at the low end of US gains. In Europe, Germany’s DAX Composite was up a strong +3.84%, and the United Kingdom’s FTSE gained +3.54%. Doing less well, but still positive, were France’s CAC40 (+2.14%) and Italy’s Milan FTSE (+1.36%). In Asia, major markets gained across the board with China’s Shanghai Stock Exchange up +1.39%, Hong Kong’s Hang Seng rising +1.6%, and Japan’s Nikkei climbing +1.44%. In commodities, a barrel of West Texas Intermediate crude oil gained $0.73 to $41.46 a barrel. Crude oil spent the week retesting support at the $40 a barrel level, last visited in late August. Precious metals gave up ground as both Gold and Silver were down roughly -0.6% at $1076.70 and $14.14 an ounce, respectively. Copper continued its plunge, down over -5.7% last week. If copper is a harbinger of upcoming worldwide industrial health, as many maintain it is, then the future is not bright for that segment as copper hit a low this week not seen since the Great Recession of 2008-09. In US economic news, initial claims for state unemployment benefits fell by -5,000 last week to 271,000, according to the labor department. Initial claims have been holding near a 42-year low and have been below 300,000 for over half a year. The number of people continuing to claim benefits rose by +2,000 to 2.18 million. Housing starts fell -11% in October to an annual rate of 1.06 million units, with the decline led by a plunge in new apartment construction. On the other hand, permits for single-family homes rose to the best level in almost 8 years. Single-family home starts fell -2.4% to 722,000, the lowest since March. The Mortgage Bankers Association reported that mortgage applications rose +6.2% last week; rising mortgage rates are encouraging buyers to act sooner rather than later. Delinquency rates for mortgage loans fell in the third quarter to their lowest rate since 2007, and mortgage foreclosures fell to the lowest rate since 2005. The October US Consumer Price Index rose +0.2% versus September. Energy prices rose last month, but are still down -17.1% versus October of last year. Core inflation, which excludes food and energy, remained at 1.9% and is holding just below the Federal Reserve’s oft-stated 2% target. US manufacturing rebounded in October as manufacturing output rose +0.4% after two months of declines. Motor vehicle production advanced +0.7% to a +10.9% annual gain as carmakers enjoy their strongest US sales in years. However, overall industrial production declined -0.2% last month, reflecting weakness in the mining sector and utilities. The New York Federal Reserve’s Empire State Manufacturing Index was still in contraction at -10.74 in November. Economists had been expecting an improvement to -5. New orders and shipments improved, but were still negative for the fourth straight month. Unfilled orders, the workweek, and employment gauges were all the weakest in a year. The Empire State index is the first of several factory activity gauges scheduled for release in November. New York Fed President William Dudley said that he Federal Reserve rate hike should show confidence in the economy, though he admits he doesn’t know how markets would react to a rate lift off. He also stated that winding down the global banking giants safely in a crisis would require more work-specifically making their legal structures “more rational and less complex.” In their October meeting minutes, released on Wednesday of this week, Federal Reserve policymakers inserted language stating that “it may well become appropriate” to raise the benchmark lending rate in December, and largely agreed that the pace of increases would be gradual. According to the minutes, “members emphasized that this change was intended to convey the sense that, while no decision had been made, it may well become appropriate to initiate the normalization process at the next meeting.” A majority of Fed officials have now signaled that they expect to raise interest rates this year for the first time since 2006. In Canada, September retail sales fell -0.5% after 4 months of gains, worse than expectations. Excluding price changes, retail sales volume rose a bare +0.1%. Canada’s October consumer price index rose +0.1% versus September, and sits at 1% versus a year earlier. Core CPI was up +0.2% versus September and up 1.7% versus a year earlier. In the Eurozone, European Central Bank (ECB) policymakers will “do what we must”, as expressed by ECB President Mario Draghi, giving an indication that the ECB will ease further at its December 3rd meeting. The ECB President also stated that the bank is ready to act quickly to boost anemic inflation in the Eurozone—“If we decide that the current trajectory of our policy is not sufficient to achieve our objective, we will do what we must to raise inflation as quickly as possible.” They definitely have their work cut out for them: October consumer prices rose +0.1% versus September, while Core CPI grew +0.2%. Core inflation was an annualized 1.1% for October versus September’s 1%. Japan has fallen back into recession as the economy contracted at a -0.8% annual rate in the thirdquarter, following a -0.7% decline in Q2. Business spending fell at a -1.3% rate, worse than forecasts and the second straight decline. The data will doubtless put even more pressure on the Bank of Japan to step up its monetary easing program. Finally, last week we noted the narrowing leadership in the LargeCap S&P 500. The largest 90 of the S&P 500 are showing gains for the year, while the remaining 410 are, on average, down substantially. The same situation – but even more narrow – exists in the Nasdaq 100, the home of the largest tech titans. A new acronym has been born – “FANG”. FANG stands for Facebook, Amazon, Netflix and Google. One could say that “without FANG, the market’s not worth a dang!” Consider this: with FANG, the Nasdaq 100 is +10% for the year; but without just these four FANG members (leaving 96 other Nasdaq 100 stocks), the Nasdaq 100 is -5% for the year. (sources: Reuters, Barron’s, Wall St Journal, Bloomberg.com, ft.com, guggenheimpartners.com, ritholtz.com, markit.com, financialpost.com, Eurostat, Statistics Canada, Yahoo! Finance, stocksandnews.com, marketwatch.com, wantchinatimes.com, BBC, 361capital.com, pensionpartners.com, cnbc.com; Figs 3-5 source W E Sherman & Co, LLC)