Vendor Rebates Audit

advertisement

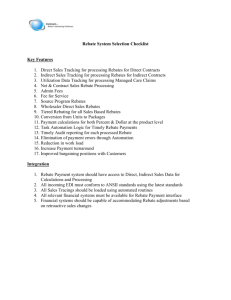

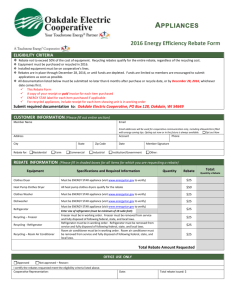

Vendor Rebates Audit Audit Objectives To determine whether: 1. Vendor rebate receivables have been properly recorded; 2. Vendor rebate receivables have been properly calculated according to terms of the vendor contracts; 3. The General Reserve for vendor rebates and the inventory adjustment are adequate; 4. Review supporting documentation for significant or unusual reconciling items. Audit Step Obtain trial balance / lead schedules: 1. Obtain the trial balance for the applicable ending period from the vendor rebate senior accountant. 2. From the trial balance, select a sample of vendor rebate balances to test. Obtain the vendor rebate reconciliation and vendor-supporting schedules for the applicable period: 1. Test clerical accuracy of the reconciliation and supporting schedules. 2. Tie the calculated rebate receivable balance per the reconciliation to lead schedule or trial balance. 3. Tie the monthly rebate accruals per the reconciliation to the vendor-supporting schedules. 4. Obtain copy of cancelled checks, and trace and agree payments received per the reconciliation to the cash records. 5. Prepare a schedule of subsequent cash receipts (rebate payments received after (insert date)), make a selection of receipts, obtain copy of cancelled checks, and trace and agree payments received to the reconciliation to the cash records. 6. Obtain adequate support for all adjustments made to receivable balances per the rebate reconciliation. 7. Scan reconciliation for unusual amounts (e.g. negative balances, repetitive amounts, unreasonably large amounts, etc.) and obtain explanations for such items. Obtain the vendor contracts: 1. Agree rebate calculations per selected test items to terms of the contract and ensure all applicable terms agree with information used in the calculations. 2. Agree purchase data used in the rebate calculations to source data. 3. Scan vendor-supporting schedules for unusual amounts (e.g. negative balances, repetitive amounts, unreasonable large amounts, etc.) and obtain explanations for such items. Test the adequacy of the General Reserve. 1. Review assumption. 2. Test for adequacy. Page 1