financial markets and institutions: important functions

advertisement

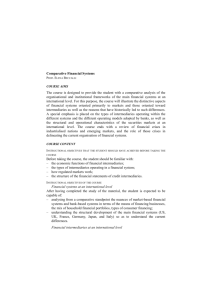

FINANCIAL MARKETS AND INSTITUTIONS: IMPORTANT FUNCTIONS Economic system relies heavily on financial resources and transactions, and economic efficiency rests in part on efficient financial markets. Financial markets consist of agents, brokers, institutions, and intermediaries transacting purchases and sales of securities. The many persons and institutions operating in the financial markets are linked by contracts, communications networks which form an externally visible financial structure, laws, and friendships. The financial market is divided between investors and financial institutions. The term financial institution is a broad phrase referring to organizations which act as agents, brokers, and intermediaries in financial transactions. Agents and brokers contract on behalf of others; intermediaries sell for their own account. Financial intermediaries purchase securities for their own account and sell their own liabilities and common stock. For example, a stockbroker buys and sells stocks for us as our agent, but a savings and loan borrows our money (savings account) and lends it to others (mortgage loan). The stockbroker is classified as an agent and broker, and savings and loan is called a financial intermediary. Brokers and savings and loans, like all financial institutions, buy and sell securities, but they are classified separately, because the primary activity of brokers is buying and selling rather than buying and holding an investment portfolio. Financial institutions are classified according to their primary activity, although they frequently engage in overlapping activities. The classification of financial market participants is outlined in Figure 1. Financial markets provide our specialized, interdependent economy with many financial services, including time preference, distribution of risk, diversification of risk, transactions economy, transmutation of contractual arrangements, and financial management. Time Preference Time preference refers to the value of money spent now relative to money available for spending in the future. Businesses are frequently making decisions among short-term and long-term uses of funds, and business executives must judge between outlays which provide a return in the near term and those which pay off many years from now. They must decide upon commitments requiring funds now and those requiring funds later, by allocating not only funds that they expect to receive currently, but also those that they expect to receive in the future. The money and capital markets price funds so that businesses and governments can make rational economic allocations of capital. The price of capital is set in a competitive marketplace by supply and demand forces. The market price of capital is compared by businesses to the expected returns in proposed capital expenditures. Businesses allocate their capital to real investments whose return is at above the cost of capital. Long-term investments are compared to short-term investments using the financial-market-determined cost of capital. Consequently, the allocation of capital between short-and long-term investments depends on the free play of supply and demand in an open market. Like businesspersons, consumers may decide upon a time pattern for expenditures that does not necessarily coincide with their current or expected income flows. Financial markets allow us to implement time adjustments in the payments for goods. Without them, there would be no opportunity to earn interest on savings, and expenditures would be limited to current receipts and cash. Savings allows many consumers to postpone consumption and to receive returns from investments. Risk Distribution The financial markets distribute economic risks. Employment and investment risks are separated by the creation and distribution of financial securities. On a larger scale, the money and capital markets transfer the massive risks from people actually performing the work (employment risks) to savers who accept the risk of an uncertain return. The chance of failure for a 100 million € mobile phones manufacturer may be divided among thousands of investors living and working all over the world. If the mobile phones business fails, each investor loses only part of his or her wealth and may continue to receive income from other investments and employment. Figure 1 Classification of participants in the financial markets Participants Commercial Banks Savings Banks Savings and Loans Credit Unions Finance Companies Life Insurance Companies Pension Funds Investment Companies Real Estate Investment Funds Mortgage Bankers Investment Bankers Securities Dealers and Brokers Clearing Houses Stock Exchanges People who own stocks, bonds, and other securities People who borrow money with mortgages, installment loans, and other instruments Classification Financial Intermediaries Financial Financial Institutions Institutions Agents Securities andMarket Brokers Institutions Investors and Borrowers Businesses (Non financial) Governments Diversification of risk In addition to permitting individuals to separate employment and investment risks, the financial markets allow individuals to diversify among investments. Diversification means combining securities with different attributes into a portfolio. Ordinarily, a diversified portfolio of financial claims is less risky than a portfolio consisting of one or at most a handful of similar securities. Total risk is reduced because losses in some investments are offset by gains in others. The benefits of diversification are possible due to the existence of large, diversified financial markets where investors may buy and sell securities with minimum transactions cost, regulatory interference, and so forth. 2 Functions of Financial Intermediaries Financial markets facilitate the movement of funds from those who save money to those who invest money in capital assets. Savings are distributed among investments and expenditures through securities traded in the financial markets. Financial institutions facilitate and improve the distribution of funds, money, and capital in several respects: 1. 2. 3. 4. 5. Payments mechanism Security trading Transmutation Risk diversification Portfolio management All of these functions are important to an efficient financial system, and managers are improving execution capability through improved electronic communication, computer processing, and institutional design. Note that these functions are characteristic of agents. Financial intermediaries are special types of agents that collect information about economic entities, evaluate financial information, and package financial claims. The financial intermediary, by purchasing primary securities and issuing secondary securities adds choices to borrowers and lenders. Issues of financial intermediaries are termed secondary securities. The process of changing the terms of money bought and sold by financial intermediaries is termed transmutation. For example, savings and loan associations obtain money with short-term, smallbalance savings deposits to make 20- to- 30 year mortgage loans in amounts usually exceeding 10,000 €. Timing and amount are usually changed through transmutation, with alterations limited only by the creativity of the financial institution and the acceptance of its customers. Financial institutions also act as portfolio managers and advisers over most of the primary securities owned by investors. The private financial sector manages most of the home mortgages, commercial mortgages, consumer loans, state and local government securities, and business loans. In addition, nearly one-fourth of outstanding common stocks are managed by investment companies, and a large portion of the remaining shares of stock are invested with the advice of trust institutions. The most important reasons for obtaining institutional management are: convenience, protection against fraud, quality of investment selection, and a low transaction cost. Financial institutions provide a convenient place where savers can safely invest excess money and consumers can easily borrow funds. Investments are protected against unscrupulous borrowers by the institution’s qualified loan officers and a bevy of collectors and attorneys. Well-trained investment analysts and loan officers seek good investment opportunities and screen prospective securities so as to obtain the best yield available for the risk level that suits the investor’s preferences. Income tax differentials among individuals and businesses are mitigated by intermediaries which transfer tax deductions from low-to high-income taxpayers and provide tax-free services in place of taxable interest. For example, pension funds owe their existence to tax differentials. Income invested in and earned by pension funds is not taxed until retirement when rates are generally lower than before retirement. Commercial banks reward depositors with “free services”, which are nontaxable, rather than pay interest, which is taxable. The depositors receive nontaxable benefits such as checking 3 accounts, traveler’s checks, and low-rate loans in return for the use of their money. Leasing intermediaries, a type of finance company, pass depreciation tax shields from equipment users in lowtax brackets to equipment owners in high-tax brackets. The depreciation expense reduces income taxes more for high-than for low-tax-bracket owners. 4