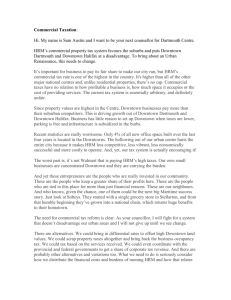

Commercial Market Analysis for Downtown Grand Rapids Arts and

advertisement