Chpt 6 - Supply and Demand: How Free Enterprise Works

advertisement

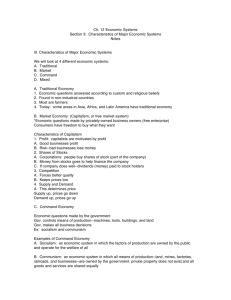

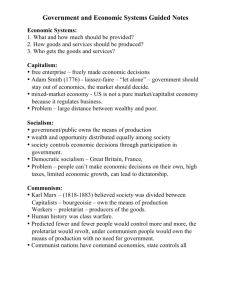

Chpt 6 - Supply and Demand: How Free Enterprise Works Economic Systems If productive resources are scarce, how do we decide whether to produce capital goods or consumer goods? Economic systems is an organized way for a country to decide how to use its productive resources…what will be produced, how will it be produced, and for whom goods and services will be produced. Types of economic systems: There are three primary types of economic systems. 1. Market Economy - consumers and producers decide what, how, and for whom goods will be produced. It is a Free Enterprise System. (U.S., Canada, Germany) 2. Command Economy – what, how and for whom goods will be produced is decided by a central planning authority. Decisions are not made by consumers but by the ruling government Dictatorships – N.Korea, China, Vietnam, Cambodia 3. Mixed Economy – Blend of market and command. National government makes production decisions for certain items such as post office, telephone systems, healthcare, public utilities. All countries have a blend of sorts. No country is 100% Market or Command however; the tendency in the last decade is for countries to become more of a market economy and to restrict the number of goods and services controlled by the government (China, France, England Mexico, Eastern European countries). ¾ In a free market economy, entrepreneurs and consumers make millions of decisions every day, usually in response to prices. ¾ A free market system is much more efficient than command economies. o Efficiency is how desired results are obtained with limited resources in an uncertain world. Consumers’ needs are met and entrepreneurs earn a profit. ¾ A command economic system fails to meet the needs of citizens. When a country or state transfers its authority to provide a good or service to individuals or businesses it is called privatization. In the U.S. some cities and states have privatized by paying businesses to collect trash, operate jails, run cafeterias in government buildings etc. The incentive is to reduce costs for taxpayers and to increase efficiency. Types of economic/political systems An economic system cannot be separated from the political system in a country. The political system influences the economic system and the economic system is nearly always determined by the political system. 1 There are three economic/political systems that exist today – capitalism, socialism, and communism. What kind do we have in the US? 1. Capitalism – free enterprise – Operates in a democracy – Private citizens are free to go into business for themselves, to produce whatever they choose to produce, and to distribute what they produce. – Private citizens are free to own their own property. – Some government restrictions exist to assure an orderly marketplace that does not harm the public – Market/mixed economy In recent years the government has assumed an important role in the economic in the US. Without controls abuses take place -Large businesses began to exploit small businesses. Manufacturing firms didn’t concern themselves with the cost of pollution (poor health, destroyed natural resources such as polluted water. 2. Socialism – government controls and regulates the means of production - May be democratic or autocratic. - Socialists don’t even agree how much of the productive resources government should own. Extreme socialists believe government should own all natural resources and capital goods. Middle of the road socialists believe government should own key industries but all other productive resources should be owned by individuals and businesses - Often associated with mixed economies. 3. Communism – forced socialism -All or almost all productive resources are owned by the government -Government decides what, how and for whom goods and services are produced -Government measures how well producers perform on the basis of volume produced without regard for quality of or demand for the goods and services. -Command economy. Fundamentals of Capitalism Some of the basic features of capitalism are the right to own private property (most fundamental), the right to make a profit, the right to set prices and the right to determine wages. 1. Private Property – consists of items of value that individuals have the right to own, use, and sell a. Individuals can control productive resources such as land, labor, and capital goods. b. These productive resources can be used to produce goods and resources. c. The producer also owns the goods produced. 2. Profit – the incentive and reward for producing goods and services. Being in business does not guarantee a profit. Business must produce goods and services that people want at a price they are willing to pay. 2 3. Price Determination - price changes send signals to entrepreneurs. Entrepreneurs know that if prices are too high, customers refuse to buy it but, if prices are too low, the product sells out quickly. Price is determined by the laws of supply and demand a. Demand – the number of products that will be bought at a given time for a given price. Demand is not the same as want. Wanting a luxury car without the ability to pay for it does not generate demand. Demand for an item is represented by people who want an item, have the money for the item, and are willing to spend the money on the item. • As price goes up, the quantity demanded by consumers goes down • There is a relationship between price and demand. Prices usually rise with increased demand, and as demand decreases, prices will usually come down. Ex. DVD players • What do you expect to happen to demand for air conditioners in the summer? • What will most likely happen to the price for air conditioners in the summer? b. Supply - the number of products that will be offered for sale at a particular time and at a particular price. If there is a supply shortage, prices will generally rise. Ex. Gasoline • As price for a product goes up, producers are more willing to supply the market c. The Market Clearing Price – the price at which the quantity of the product the consumer is willing to buy equals the number of products the producer is willing to supply Market Price Clearing $1.00 Supply $ .90 P r i c e $ .80 $ .70 $ .60 $ .50 $ .40 Demand $ .30 $ .20 $ .10 1 2 3 4 5 6 7 8 9 10 11 Quantity 3 • Supply and demand together determine what will be bought and sold and what the price will be in any given market d. Price changes are the result of changes in both supply and demand. Price changes indicate to businesses what is profitable or not profitable to produce and how much should be produced. 4. Competition - sellers want to make a profit while consumers want the quality goods at a low price. Competition settles this conflict. Competition is the rivalry among seller’s for consumers’ dollars. Benefits of competition to society include: a. Improved quality to attract customers b. Development of new products c. Operate efficiently to keep prices down and conserve scarce productive resources This ensures that customers get new and quality products at fair prices. There are different ways for companies to compete. a. Price competition – you take a competitor’s business by lowering prices. b. Non-price competition – better quality products or adding a feature that the competition doesn’t have. Unique shapes, colors, etc are ways to compete. What is the opposite of competition? 5. Income Distribution – not only must companies decide what to produce, they must also decide how to divide the goods among society. a. In our market this is determined by the amount of income a person has to purchase these goods/services. b. Wages for employees are determined by supply and demand and factors such as skill required, education, and abilities. 4