slovenia - Rabobank

advertisement

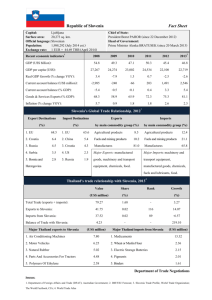

Country report SLOVENIA Summary Reflecting its economic and political problems, Slovenia has been singled out as the potential next candidate for an EU/IMF rescue package following this year’s Cypriot bailout. Its economy is going through a protracted double-dip recession due to a serious banking crisis, fiscal consolidation at home and weak external demand. The recent fall of the government has raised concerns that important policy initiatives might not be completely implemented by the new cabinet. As nonperforming loans worth 20% of GDP burden the local banking sector, the swift transfer of a large part of these loans to a bad-bank lies at the core of the current cabinet’s tasks, followed by fiscal consolidation and structural reforms. It remains to be seen whether the new center-left cabinet will be up to this challenge, as anti-austerity sentiment is rising. In spite of its current problems, Slovenia managed to cover its financing needs for this year amid ample liquidity on international capital markets, but larger-than-expected bank recapitalization costs might still force it to apply for external assistance. Author: Fabian Briegel Country Risk Research Economic Research Department Rabobank Nederland Contact details: P.O.Box 17100, 3500 HG Utrecht, The Netherlands +31-(0)30-21-64053 F.Briegel@rn.rabobank.nl May 2013 Rabobank Economic Research Department Page: 1/9 Country report SLOVENIA Slovenia National facts Social and governance indicators rank / total Type of government Parliamentary republic Human Development Index (rank) C apital Ljubljana Ease of doing business (rank) 35 / 185 Surface area (thousand sq km) 20 Economic freedom index (rank) 76 / 179 Population (millions) 2.1 C orruption perceptions index (rank) 37 / 176 Main languages Slovenian (91%) Press freedom index (rank) 35 / 179 Main religions 21 / 187 Serbo-C roatian (4.5%) Gini index (income distribution) 31.15 C atholic (58%) Population below $1.25 per day (PPP) 0.06% Muslim (2%) Head of State (president) Orthodox (2%) Foreign trade Borut Pahor Main export partners (%) 2011 Main import partners (%) Head of Government (prime-minister) Alenka Bratušek Germany 24 Germany 19 Monetary unit Italy 14 Italy 18 euro (EUR) Economy 2012 Austria 9 Austria 12 C roatia 8 C roatia 5 bn USD % world total Nominal GDP 46 0.07 Manufactures 83 Nominal GDP at PPP 58 0.07 Fuels and mining products 10 Export value of goods and services 35 0.16 Agricultural products IMF quotum (in m SDR) 275 0.13 Economic structure 2012 5-year av. Real GDP growth -2.3 0.9 3 2 Industry (% of GDP) 28 30 Services (% of GDP) 70 67 Economic size Agriculture (% of GDP) Standards of living Main export products (%) 7 Main import products (%) Manufactures 68 Fuels and mining products 20 Agricultural products 11 USD % world av. Nominal GDP per head 22621 206 Openness of the economy Export value of G&S (% of GDP) Nominal GDP per head at PPP 28169 218 Import value of G&S (% of GDP) 72 Real GDP per head 18656 225 Inward FDI (% of GDP) 1.4 75 Source: EIU, CIA World Factbook, UN, Heritage Foundation, Transparency International, Reporters Without Borders, World Bank, World Trade Organization. Economy falls back into a deep and protracted double-dip recession Slovenia’s economy still struggles to embark on a solid recovery following its very deep recession in 2009, when GDP declined by almost 8%. While economic growth returned to a meagre 1% on average in 2010 and 2011, as the global economic recovery helped Slovenia’s export-dependent economy, it slipped back into recession last year. Pulled down by protracted balance-sheet repairs by Slovenia’s heavily-indebted corporate sector, tight credit conditions, ongoing fiscal austerity measures and their impact on consumer spending, rising unemployment and stagnating exports, output fell by 2.3% in 2012. Compared to its euro area and regional peers, Slovenia experienced the deepest recession last year, while its total GDP loss since the onset of the global economic crisis (-8%) ranks second only to Greece (-20%) in the euro area. Figure 1: GDP contraction since 2008 Figure 2: Economic growth percentage points 0 percentage points 0 -5 -5 -10 -10 -15 -15 %-yoy 6 %-yoy 6 4 4 2 2 0 0 -2 -2 -4 -4 -6 -6 -8 -8 -10 -10 -12 -20 -20 Greece Slovenia Italy Source: Eurostat May 2013 Portugal Spain -12 08 09 10 11 Private consumption Gross fixed capital formation Net exports Ireland Cyprus 12 13f 14f Public consumption Inventories Real GDP Source: European Commission Rabobank Economic Research Department Page: 2/9 Country report SLOVENIA Going forward, Slovenia’s economic outlook remains rather bleak, as the further escalation of its serious banking crisis (also see next section) not only restricts access to credit, but also leads to spiking risk premiums on Slovenian debt amid concerns that the country might have to apply for EU/IMF financial assistance. While government and private consumption are expected to fall further due to still rising unemployment levels and decisive efforts to rein in Slovenia’s bloated fiscal deficit, further steep declines in gross fixed investments, particularly construction, are highly probable. This trend is unlikely to change soon, unless Slovenia’s banking system, which is currently drowning in bad loans, is cleaned up swiftly and thoroughly and thereby regains its capacity to provide credit. Meanwhile, foreign direct investment is unlikely to compensate for the domestic shortfall amid lingering concerns about Slovenia’s business climate and competitiveness after years of reform backlogs. This leaves net exports as the sole source of growth in2013, but owing to strongly declining domestic demand, Slovenia’s economy is expected to contract by 2% this year before stabilizing next year. Even worse, the downside risks to the outlook, both domestic and external, are considerable. As exports, primarily destined for the euro area, amount to about 70% of GDP, economic weakness abroad would hit Slovenia hard. At home, a protracted deleveraging process of the corporate sector, delays in resolving the banking sector crisis, and strongly rising taxes to finance recurrent recapitalizations of state-owned banks (SOBs) and enterprises (SOEs) could further undermine Slovenia’s economic recovery. A serious banking crisis asks for a swift policy response Slovenia’s banking system currently undergoes a grave banking crisis, as predominantly local state-owned banks are burdened with very high amounts of non-performing loans, while capitalization levels at several banks remain weak in spite of recurrent recapitalizations by the Slovenian state in recent years. In September 2012, Slovenia’s systemwide non-performing loan (NPL) ratio increased to 14.2% of total loans, up from 11.2% in December 2011, while the sectorwide Tier 1-capital ratio came in at 10.1%, also up from 9.6% from the end of 2011. Given total bank assets worth about 140% of GDP, non-performing loans currently amount to about EUR 7bn, or roughly 20% of GDP. In contrast to other euro area members with a banking crisis, e.g. Spain, non-performing loans are particularly prevalent in the corporate sector, while asset quality of household loans has held up relatively well. As of September 2012, about 24% of corporate loans were overdue, whereby the collapse of Slovenia’s construction sector brought with it a sectorwide NPL-ratio of 62% in that segment. Figure 3: Bank capitalization & Asset quality 12 Figure 4: Non-performing loans per bank % % 24 % of respective loan portfolio 80 % of respective loan portfolio 80 10 20 70 70 8 16 60 60 6 12 50 50 4 8 40 40 2 4 30 30 20 20 0 0 08 09 10 11 12 (Sept) Tier 1 capital ratio (l) Non-performing loan (NPL) ratio (r) NPL - Corporates (r) NPL - Housholds (sole proprietors)(r) NPL - Non-residents (r) NPL - OFIs (r) Source: Banka Slovenije 10 10 0 0 Large domestic banks Small domestic banks Total Financial intermediation Trade Banks under majority foreign ownership Construction Manufacturing Source: Banka Slovenije The systemwide figures hide marked differences among banks, however. As mentioned before, Slovenia’s three large state-owned banks (Nova Ljubljanska Banka (NLB), Nova Kreditna Banka May 2013 Rabobank Economic Research Department Page: 3/9 Country report SLOVENIA Maribor, Abanka) are particularly affected. While foreign-owned banks’ NPL-ratio stood at about 11% in September 2012, a-third of all loans of the largest domestic banks was non-performing. The sizeable build-up of bad loans comes in the wake of a lending boom that doubled Slovenia’s loan-to-GDP ratio from about 40% of GDP in 2003 to 92% of GDP in 2011. It brought with it extremely favorable credit conditions that oftentimes led to unprofitable corporate mergers and acquisitions, as well as leveraged management bailouts at too high prices. According to the OECD, the particularly poor performance of state-owned banks could be explained by a weak governance framework that contributed to excessive risk-taking and sub-optimal credit standards, while preliminary findings of the Slovenian Corruption Prevention Commission suggest that the apparent misallocation of capital was likely also due to corrupt behaviour. Moreover, we note that widespread direct and indirect state-ownership, estimated at up to 50% of the local economy, likely also contributed to the application of relatively lenient lending criteria by state-owned banks. Owing to Slovenia’s poor economic outlook, asset quality will continue to deteriorate, which will further undermine bank equity. Unsurprisingly, capitalization levels at the state owned banks are far lower than at foreign-owned banks, which makes recurrent recapitalizations by the Slovenian state necessary, especially so since Belgian banking group KBC sold its stake in NLB last year. In its third loss-making year in a row, the banking system’s pre-tax losses in the first ten months of last year increased by EUR 31m to EUR 155m compared to the same period in 2011, which will likely deter any foreign investment into the ailing sector. We consequently caution that, given the large and rising amount of NPLs (20% of GDP), considerable recapitalizations of the banking system will be needed in the near future, unless these loans are carefully removed from the banks’ balance sheets. Slovenia’s government currently expects recapitalizations worth EUR 1bn this year, but we caution that this amount will likely increase considerably given the country’s economic outlook and its impact on asset quality. We also note that the poor state of the banking sector has severely restricted its access to marketbased sources of external funding, on which the sector depends given its loan-to-deposit ratio of 136% in October 2012. While funding from foreign parent banks of local subsidiaries has declined markedly, Slovenian banks’ access to (external) wholesale funding worsened considerably and led to increased reliance on ECB funding (up from a pre-crisis 2.6% of total funding to 8.4% last October). Since Slovenian banks are not yet forced to use the ECB’s Emergency Liquidity Assistance (ELA) facility, the risks to an abrupt stop of this type of funding are minimal, which reduces the risk of imminent liquidity shortages of the local banking system. While Slovenia’s central bank stresses that the commonly known problems of the banking sector have so far not led to significant deposit flight in the wake of the Cypriot deposit bail-in, we do not completely exclude this risk. Even though the availability of roughly EUR 4bn in bank equity and EUR 2bn of junior and senior bank debt argue against a deposit bail-in, savers might still decide to take their money out of Slovenia’s banks, particularly once the country receives increased attention from the EU following the submission of its National Reform Program in May. Given the apparent unsustainability of the situation, Slovenia’s previous government decided to clean the banks’ balance sheets by means of transferring non-performing loans worth about EUR 4bn (11% of GDP) to a bad bank, the so-called Bank Asset Management Company (BAMC), which was established in October 2012. It is envisaged that banks will receive government-backed BAMC bonds in return for the transferred loans. Moreover, the creation of a Sovereign Holding (SH) was decided that would bundle the state’s various stakes in enterprises for the purpose of privatization. Both, the BAMC and the SH are not fully operational yet and have been subject to considerable May 2013 Rabobank Economic Research Department Page: 4/9 Country report SLOVENIA political debate in Slovenia. While the Positive Slovenia party of incumbent prime minister Alenka Bratušek opposed the SH, trade unions tried to block the BAMC by means of a referendum. In our view, the swift implementation of both institutions likely represents the only way out of Slovenia’s crisis. The removal of bad loans from banks’ balance sheets should re-enable them to provide credit, while the privatization of state-owned enterprises should harden their budget constraints and thereby reduce their need for ongoing funding by state-owned banks. While the first transfer of bad loans to the BAMC is planned for June, less is known about the government’s privatization agenda besides that it will likely comprise one of the state-owned banks. Still, we caution that this necessary overhaul of the ‘Slovenian model’, which has taken place in other regional peers decades ago, will likely face considerable public opposition. Seriously deteriorated public finances raise concerns about medium-term debt sustainability Slovenia’s once very healthy fiscal situation has worsened markedly since the onset of the global economic crisis and the start of the local banking misery. Unless high budget deficits are reined in soon in the current low growth/recessionary environment, public debt sustainability could be compromised over the medium-term. While public debt amounted to a comfortable 22% of GDP in 2008, stubbornly high budget deficits caused by declining tax revenues, recurrent recapitalizations of ailing state-owned banks and stateowned enterprises, as well as falling nominal GDP, increased public debt to 54% of GDP last year. Following three years of budget deficits in the range of 6% of GDP, expenditure-based fiscal consolidation programs implemented by previous governments brought last year’s budget deficit down to 4.0% of GDP. Partly owing to rising social transfers, this year’s budget deficit is expected to increase again to 5.3% of GDP, while the European Commission expects the 2014 deficit to still come in at 4.9% of GDP under the no-policy-change assumption. Given stagnant nominal economic growth, public debt is expected to increase to 61% of GDP this year. These projections neither include this year’s anticipated bank recapitalization costs of EUR 1bn (3% of GDP) nor state guarantees for the BAMC. In case government-guaranteed bonds issued by the BAMC are considered as public debt, the ratio may even increase to about 70% of GDP. Moreover, the possible recategorization of the national highway company’s (DARS) debt could increase public debt by another 8-9% of GDP. Figure 5: Public finances (excluding upcoming bank recapitalization costs) % of GDP Figure 6: CDS spreads % of GDP bps bps 80 8 1600 60 6 1400 1400 40 4 1200 1200 20 2 1000 1000 0 0 -20 1600 800 800 600 600 400 400 200 200 -2 -40 -4 -60 -6 -80 -8 08 09 Public debt (l) 10 11 Budget balance (r) 12 13f 14f 0 Structural budget balance (r) 0 10 Public debt (l) (incl. BAMC bonds) 11 Slovenia Source: European Commission, Rabobank 12 Portugal Italy 13 Ireland Spain Source: Bloomberg Since Slovenia’s debt refinancing costs have risen in line with its worrying debt dynamics, the government’s dependence on short-term funding has increased accordingly in recent years. As 10- May 2013 Rabobank Economic Research Department Page: 5/9 Country report SLOVENIA year government bond yields have repeatedly reached levels close to or above 7% and foreign investors are increasingly avoiding Slovenian exposures, reliance on the ailing local banking sector also increased. While these trends strengthened the problematic interdependency between the local sovereign and the banking sector, they also increased debt roll-over risks as the average maturity of public debt shortened. Given Slovenia’s still moderate public debt level, we note that the swift implementation of necessary policies, particularly the implementation of the bad bank and the privatization of SOEs, could restore international investor confidence and thereby improve access to international capital markets at more favorable rates. Still, we note that additional spending cuts and reforms, particularly pension reforms, will be needed to ensure medium-term debt sustainability, given last year’s structural budget deficit of 2.7% of GDP. More clues about the future trajectory of Slovenia’s public finances will be provided by the presentation of its privatization plans expected for early May 2013 and its National Reform Programme (NRP) for 2013-14, which has to be submitted to the European Commission (EC) by May 9th, 2013. According to its preliminary version that has been presented to parliament recently, the NRP aims at, among others, ongoing fiscal consolidation by means of both spending cuts and tax increases, as well as reforms of the banking system and the welfare state. In order to boost competitiveness and growth, a review of the minimum wage system and the elimination of bureaucratic red tape is also considered. As Slovenia, together with Spain, has been given a deadline under the EC’s new Macroeconomic Imbalance Procedure to implement necessary reforms by May 29th, close EU scrutiny can be expected, which could provide an important external anchor for the implementation of policies. Stability of Slovenia’s new center-left government will be crucial While weak euro area demand for Slovenian exports and the ongoing local banking crisis goes a long way in explaining the country’s current difficulties, we note that the impact of its rather volatile political landscape and the local population’s apparent weak support for reforms should not be underestimated. In particular, the instability of recent governments and the possibility of binding referendums (with only 40,000 signatures needed to call for such a referendum) considerably increased policy implementation risks in recent years. Given the country’s trade unions’ opposition to needed changes in social security legislation, the previous government faced considerable problems when implementing urgently needed labor and pension reforms. While last year’s ruling by the country’s Constitutional Court eventually blocked referenda on the BAMC and the SH, rising public discontent with economic policies could once more lead to proposals for new referenda that cannot be rejected by the Constitutional Court indefinitely. Following the gradual disintegration of previous prime minister Janez Janša’s center-right coalition government amid corruption allegations, Slovenia is currently governed by a center-left cabinet under the leadership of Alenka Bratušek of the Positive Slovenia (PS) party. Amid rising external pressure, Ms Bratušek struggled to form a coalition with the Social Democrats (SD), Gregor Virant’s Citizen’s List (DL) and the Party of Slovenian Pensioners (DeSus). Her coalition currently controls a narrow majority of 49 out of 90 seats in parliament, whereby the departure of any of the coalition’s members could lead to the collapse of the government. While coalition cohesion has been surprisingly strong so far in spite of lingering differences of opinion within the coalition, government stability might be weak once painful decisions need to be taken. In particular, we note that several parties, including the prime minister’s PS, were opposed to the previous government’s economic policies, which they are now forced to implement amid rising speculations that the country might be next in line for an EU/IMF bailout. Moreover, given the volatility of Slovenia’s May 2013 Rabobank Economic Research Department Page: 6/9 Country report SLOVENIA political landscape, several coalition members might opt to push for new elections if polls were to indicate a victory. Figure 7: Alenka Bratušek’s coalition Hungarian and Italian national communities Nova Slovenija (NSi) 4 Independents 3 2 Figure 8: Employment situation 80 % % 12 78 Pozitivna Slovenija (PS) Slovenska ljudska 6 stranka (SLS) 10 76 74 27 8 72 Slovenska demokratska26 70 6 68 stranka (SDS) 4 66 64 10 Demokraticna stranka upokojencev Slovenije (DeSUS)5 7 Socialni demokrati (SD) Državljanska lista Gregorja Viranta (DL) 2 62 60 0 08 09 10 Employment rate (l) Source: Slovenian parliament 11 12 13 Unemployment rate (r) Source: Eurostat Notwithstanding the risks of an early coalition break-up and consequent detrimental delays to policy implementation, we note that Ms Bratušek, Slovenia’s first female prime minister, will face a formidable task in convincing Slovenians that ongoing fiscal consolidation is needed. Moreover, it remains to be seen whether vested interests will provide unconditional support for her privatization agenda. Having assumed office with the promise of ‘more economic growth’ and milder austerity, she now has to sell a planned VAT hike and large-scale privatizations to a disgruntled public; a challenging task amid a continuously worsening labor market, increasing austerity fatigue and rising public disenchantment with what it perceives as a ‘corrupt’ elite. It remains to be seen whether she will be up to this challenge, given widespread perceptions among Slovenians that she has been a protégée of former PS leader Zoran Janković1 so far and the fact that her party once opposed most of the policies she now has to implement. We caution that the failure to implement necessary policies in time, either caused by politicallymotivated delays, public opposition or the break-up of the current coalition government, could have a detrimental effect on investor confidence and force the country to still apply for external assistance. Lingering concerns about an EU/IMF bailout Following the Cypriot bailout, Slovenia was quickly singled out as the most likely next candidate for an EU/IMF bailout. As foreign investors dropped their holdings of Slovenian sovereign bonds across the board, yields of both short-term and long-term bonds spiked and temporarily reached levels of almost seven per cent. Even though Slovenian government bond yields declined somewhat in recent weeks as prime minister Bratušek reaffirmed her cabinet’s commitment to a swift clean-up of the banking sector and ongoing austerity, they remain elevated and complicate the country’s access to long-term external financing at acceptable rates. Notwithstanding lingering concerns about insufficient access to funding, Slovenia’s government managed to refinance its maturing debt and prefund this year’s financing needs by tapping both local and external markets. Though denied by Slovenian officials, widespread state-ownership of the local banking sector likely helped the government in selling treasury bills domestically amid at times faltering external demand. In this regard, the importance of the local banking system’s 1 Mr Janković handed over the PS leadership to Ms Bratušek following the announcement by the country’s anticorruption commission that he could not explain the source of some of his income. May 2013 Rabobank Economic Research Department Page: 7/9 Country report SLOVENIA access to ECB funding, whereby Slovenian government bonds can be used as collateral, should not be underestimated, as it enables the local banking sector to finance the government in spite of its poor state. While access to external bond markets at acceptable rates has been rather volatile in recent weeks, Slovenia’s government successfully tapped international capital markets with USDdenominated 5-year and 10-year bonds in early May with a total volume of USD 3.5bn. The amount raised should cover the Slovenian government’s financing needs this year. Given lingering uncertainty about the actual implementation of the government’s rescue plan for the banking sector, we note, however, that the successful issuance likely mainly reflected investors’ search for yield amid ample liquidity on international capital markets. The recent successful domestic and external debt issuances should strongly reduce the need for an EU/IMF-bailout in the near-term, but larger-than-expected bank refinancing costs could still force the Slovenian government to once more issue debt this year. While we remain relatively optimistic that the local banking sector should be able to buy at least part of a new debt issuance, provided ECB funding remains in place, we note that access to international capital markets cannot be taken for granted. In this regard, lacking progress on bank restructuring or the demise of the current government could lead to a marked fall in external investor appetite for Slovenian debt. Therefore, depending on the size of upcoming bank recapitalization costs, Slovenia could still be forced to apply for external assistance, even as the likelihood of this event happening in the near-term has decreased considerably. Moreover, given the small size of the Slovenian economy (0.04% of Eurozone GDP), the likely small amount of needed support, and European leaders commitment to halt contagion across the Eurozone, we do not expect any difficulties in obtaining ESM funds if needed. May 2013 Rabobank Economic Research Department Page: 8/9 Country report SLOVENIA Slovenia Selection of economic indicators 2008 2009 2010 2011 2012 2013e 2014f GDP (% real change pa) 3.4 -7.8 1.2 0.6 -2.3 -2.0 -0.1 Harmonized consumer price index (%-yoy) 5.5 0.9 2.1 2.1 2.8 2.2 1.4 C urrent account balance (% of GDP) -6.1 -0.4 -0.4 0.1 2.7 4.8 4.7 -0.1 Key country risk indicators Economic growth GDP (% real change pa) 3.4 -7.8 1.2 0.6 -2.3 -2.0 Gross fixed investment (% real change pa) 7.7 -23.5 -13.3 -9.2 -8.5 -5.6 0.0 Private consumption (real % change pa) 2.4 0.0 1.7 0.6 -2.8 -3.5 -1.8 -1.7 Government consumption (% real change pa) 5.3 3.3 1.6 -1.6 -1.6 -1.6 Exports of G&S (% real change pa) 3.9 -16.8 10.1 6.9 0.4 1.3 3.4 Imports of G&S (% real change pa) 3.8 -19.7 8.2 5.2 -4.5 -1.9 1.9 -4.9 Economic policy Budget balance (% of GDP)1 -1.9 -6.2 -5.9 -6.4 -4.0 -5.3 Public debt (% of GDP)1 22 35 39 47 54 61 67 Harmonized consumer price index (%-yoy) 5.5 0.9 2.1 2.1 2.8 2.2 1.4 Exchange rate EUR to USD (average) 0.7 0.7 0.8 0.7 0.8 0.8 0.8 Recorded unemployment (%) 4.4 5.9 7.3 8.2 8.9 10.0 10.3 Balance of payments (m USD) C urrent account balance -3382 -279 -265 0 1157 2250 -3529 -697 -1327 -1531 -386 530 920 Services balance 2206 1672 1858 2088 2186 2390 2630 Income balance -1471 -975 -796 -696 -514 -660 -920 -441 -279 133 139 0 -130 -390 Trade balance Transfer balance 2230 Net direct investment flows 460 -885 439 1046 300 500 800 Net portfolio investment flows 561 6440 2633 1747 2000 1920 1950 External position (m USD) Total foreign debt 57461 56100 53691 56259 52768 n.a. n.a. -18529 -20630 -20706 -19596 n.a. n.a. n.a. Total assets 47661 49699 45461 43791 n.a. n.a. n.a. Total liabilities 66190 70329 66167 63387 n.a. n.a. n.a. International investment position Key ratios for balance of payments, external solvency and external liquidity Trade balance (% of GDP) -6.5 -1.4 -2.8 -3.0 -0.8 1.1 2.0 C urrent account balance (% of GDP) -6.1 -0.4 -0.4 0.1 2.7 4.8 4.7 Inward FDI (% of GDP) 3.5 -1.3 0.8 2.2 1.4 2.2 3.2 Foreign debt (% of GDP) 105 113 114 112 114 n.a. n.a. Foreign debt (% of XGSIT) International investment position (% of GDP) 1 144 180 161 142 140 n.a. n.a. -33.8 -41.6 -43.8 -38.9 n.a. n.a. n.a. Excluding state guarantees for the Bank Asset Management Company (BAMC) and upcoming bank recapitalization costs. Source: European Commission Spring Forecast 2013, EIU (exchange rate, FDI & portfolio investment flows), Central Bank of Slovenia/Banka Slovenije (External position) Disclaimer This document is issued by Coöperatieve Centrale Raiffeisen-Boerenleenbank B.A. incorporated in the Netherlands, trading as Rabobank Nederland, and regulated by the FSA. The information and opinions contained herein have been compiled or arrived at from sources believed to be reliable, but no representation or warranty, express or implied, is made as to their accuracy or completeness. It is for information purposes only and should not be construed as an offer for sale or subscription of, or solicitation of an offer to buy or subscribe for any securities or derivatives. The information contained herein is not to be relied upon as authoritative or taken in substitution for the exercise of judgement by any recipient. All opinions expressed herein are subject to change without notice. Neither Rabobank Nederland, nor other legal entities in the group to which it belongs accept any liability whatsoever for any direct or consequential loss howsoever arising from any use of this document or its contents or otherwise arising in connection therewith, and their directors, officers and/or employees may have had a long or short position and may have traded or acted as principal in the securities described within this report, or related securities. Further it may have or have had a relationship with or may provide or have provided corporate finance or other services to companies whose securities are described in this report, or any related investment. This document is for distribution in or from the Netherlands and the United Kingdom, and is directed only at authorised or exempted persons within the meaning of the Financial Services and Markets Act 2000 or to persons described in Part IV Article 19 of the Financial Services and Markets Act 2000 (Financial Promotions) Order 2001, or to persons categorised as a “market counterparty or intermediate customer” in accordance with COBS 3.2.5. The document is not intended to be distributed, or passed on, directly or indirectly, to those who may not have professional experience in matters relating to investments, nor should it be relied upon by such persons. The distribution of this document in other jurisdictions may be restricted by law and recipients into whose possession this document comes from should inform themselves about, and observe any such restrictions. Neither this document nor any copy of it may be taken or transmitted, or distributed directly or indirectly into the United States, Canada, and Japan or to any US-person. This document may not be reproduced, distributed or published, in whole or in part, for any purpose, except with the prior written consent of Rabobank Nederland. By accepting this document you agree to be bound by the foregoing restrictions. May 2013 Rabobank Economic Research Department Page: 9/9