Unit 3 - Lesson 1A - Types of Economic Systems

advertisement

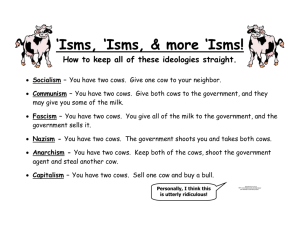

Grade 12 Canada and World Issues – Unit 3 Lesson 1 Types of Economic Systems In general terms, economic systems can be classified in four terms. The four terms and their definitions are noted in Table 1. Table 1. Types of Economic Systems Definition Terms Practice Market Economy An economic system in which individuals own and operate the factors of production. Free enterprise Capitalism United States Great Britain Japan Command Economy An economic system in which the government owns and operates the factors of production. Socialism Communism Cuba China Laos Traditional Economy An economic system based upon customs and traditions. Economy is based upon agriculture and hunting. NonIndustrialized Agrarian societies Chad Haiti Rwanda Mixed Economy An economic system that has features of both market and command economies. In reality, there are no pure market economies or pure command economies. For example, free enterprise reigns in the United States, yet the government plays a major role in the USA economy. Minimum wages, social security, and regulatory policies are examples of government involvement. In China, some private ownership of businesses is allowed, however the government still maintains tight control over the factors of production and prices. While the United States and China are mixed economies because they contain both market and command economic features, this statement may be misleading because the role that the respective governments play in the economy are quite different. Our economic system is often referred to as a Market Economy. A Market is defined as any place a buyer or consumer can meet with a seller or provider of a good to determine the price and quantity of a good. Thus, a yard sale or Internet purchases qualify as a “market.” The Market Economy is based on certain fundamental beliefs. Private Property - Labor resources, natural resources, capital resources (e.g., equipment and buildings), and the goods and services produced in the economy are largely owned by private individuals and private institutions rather than by government. This private ownership combined with the freedom to negotiate legally binding contracts permits people, within very broad limits, to obtain and use resources as they choose. Freedom of Enterprise and Choice - Private entrepreneurs are free to obtain and organize resources in the production of goods and services and to sell them in markets of their choices. Consumers are at liberty to buy that collection of goods and services that best satisfies their economic wants. Workers are free to seek any jobs for which they are qualified. Motive of Self-Interest – This is the "Invisible Hand" that is the driving force in a market economy: each individual is promoting her/his self-interest. Consumers aim to get the greatest satisfaction from their budgets; entrepreneurs try to achieve the highest profits for their firms; workers want the highest possible wages and salaries; and owners of property resources attempt to get the highest possible prices from the rent and sale of their resources. Competition - Economic rivalry means that buyers and sellers are free to enter or leave any market and that there are buyers and sellers acting independently in the marketplace. It is competition, not government regulation, that diffuses economic power and limits the potential abuse of that power by one economic unit against another as each attempts to further its own self-interest. System of Markets and Prices - Markets are the basic coordinating mechanisms in our type of economy, not central planning by government. A market brings buyers and sellers of a particular good or service into contact with one another. The preferences of sellers and buyers are registered on the supply and demand sides of various markets, and the outcome of these choices is a system of product and resource prices. These prices are guideposts on which participants in markets make and revise their free choices in furthering their self-interests. Limited Government - A competitive market economy promotes the efficient use of its resources. As a self-regulating and self-adjusting economy, no significant economic role for government is necessary. However, a number of limitations and undesirable outcomes associated with the market system result in an active but limited economic role for government. The Causes of Economic Growth Economic Growth is caused by improvements in the quantity and quality of the factors of production that a country has available i.e. land, labour, capital and enterprise. Conversely economic decline may occur if the quantity and quality of any of the factors of production falls. Improving the Quantity and Quality of Land Resources Increases in the quantity of land available for agriculture will increase economic growth. However, the extent to which this happens is limited to the extent to which unused land can be converted to agricultural land. Land, as an economic resource, is scarce. Land has an opportunity cost. Land converted for agricultural purposes is no longer a habitat for wildlife. The scarcity of land in the face of a growing population means that the law of diminishing returns might become relevant. The law predicts that an increasing amount of labour applied to a fixed quantity of land will cause the productivity of the labour to fall. To prevent this loss in productivity the quality of the land must be improved (e.g., improved irrigation, fertilizers, pest control). Improving the Quantity and Quality of Human Resources Increases in the supply of labour can increase economic growth. Increases in the population can increase the number of young people entering the labour force. Increases in the population can also lead to an increase in market demand and stimulate production. However, if the population grows at a faster rate than the level of GDP, the GDP per capita will fall. The quality of that labour also impacts economic growth. Improving the skills is seen important key. Many LDC work to provide universal primary education. As more and more capital is used, labour has to be better trained in the skills to use them, such as servicing tractors and water pumps, running hotels and installing electricity. Education spending is also an opportunity cost, and it is often referred to as investment spending on human capital. Improving the Quantity and Quality of Capital Resources It is important to distinguish between: Directly productive capital (e.g., plant and equipment, factories) Indirectly productive capital (e.g. infrastructure, roads and railways). The process of acquiring capital is called investment. The opportunity cost of capital investment is the current consumption foregone. The level of investment and the quality of investment will directly affect the level of economic growth. The efficiency of the labour force and the other factors of production will depend upon the amount and quality of capital. In LDCs, some investment comes from abroad in the form of foreign direct investment. There has been criticism of some investment in LDCs as to whether it is appropriate. If production moves from being labour intensive to capital intensive, unemployment and poverty increases. The Quantity and Quality of Enterprise Resources The level of economic growth may be slowed down if there is a lack of entrepreneurial and risk taking managers. For growth to take place inventions and innovations must be encouraged. Again the role of education is seen as being essential here. Multinational enterprises also can provide training in management skills. In countries where government has taken a considerable role in production, there might be a lack of enterprise culture. In addition, where traditional agriculture has been communally organized, the move towards a private sector profit-making culture is likely to be slow. Grade 12 World Issues - Unit 3 Lesson 1 - Challenges to Diversity Economic Theories – Wallerstein’s Core and Periphery The Core and Periphery Theory was developed by Immanuel Wallerstein. Wallerstein examined the development and change in post-colonial Africa, and between 1974 and 1989, he wrote a three-volume theory regarding global economics called The Modern World System. Wallerstein rejected the idea of a Third World. Rather, he suggested there is only one world connected by a complex network of economic exchanges (i.e., a World System). This system originates in 16th Century Europe giving the politically and economically modernizing countries such as Britain and France an initial capital or economic advantage over other parts of the world. The advantage expands through industrialization in the 20th Century so that every part of the world is incorporated into a global capitalist economy. However, the distribution of capitalism is not homogeneous; rather, it differs due to civilization development. These differences give rise to an economic core and periphery. Wallerstein’s theory has the following main features. Countries in Western Europe form an “economic core” around which the rest of the world developed. Western European countries shared these common characteristics: Strong central government Large public service Effective and well equipped armies Capital concentrated in urban centres Expanding economy The periphery countries include Asia, Africa, Eastern Europe and Latin America. The periphery countries typically were controlled by the core countries. The periphery feeds materials, natural resources and labour to the core. The theory has four country categories: Core Semi-periphery – manufacture goods with high value, exist outside of core but exploit the periphery Periphery – owned by the core, supplies and all surpluses to the core, weak or no central government, cheap labour External – outside world economy, isolated The Core will continue to dominate. The Core may shift geographic location, but its function does not change. As well, rich and poor sectors will continue to grow (i.e., the Core will get richer while the Periphery becomes poorer). This gap serves the needs of the Core (e.g., Periphery is source of cheap labour). An effect of the Core’s shift and expansion is everything is turned into a commodity, including human labour. As a commodity, the economic market dictates their value, and as such, the intrinsic value given to human relationships, labour, natural resources and land is removed. Although criticized by conservatives and neo-liberals because it downplayed the role of culture, many anti-globalization use Wallerstein’s ideas to advocate for “non-system approaches” to world development. NOTE: The UN Development Program suggests the difference between the bottom 20% (poor) and the top 20% (rich) is increasing. The ratio of poor to rich has increased from 30:1 in 1960 to over 60:1 in 2000. Economic Theories - Rostow’s Modernization Theory The Five Stages of Economic Growth W.W. Rostow. 1960. The Stages of Economic Growth: A Non-Communist Manifesto. Cambridge. In 1960, Walt Whitman Rostow suggested that economic development within a country moves along five identifiable stages of growth. NOTE: Rostow was a strong anti-communist and a strong advocate of capitalism and free market enterprise. His theory is seen as part of the framework for the Modernization Theory of world development. According to Rostow, development or the movement from an early stage to a later stage requires substantial investments of capital. Moreover the right conditions for investment need to be established for change to occur. Thus, foreign aid or direct investment in a country is only effective if the conditions of the prior stage have been met. For example, aid for a Stage 3-type development would be premature if the Stage 2 requirements have not been reached. In this case, it would be better to invest in Stage 2-type actions to ensure a more rapid rate of change. Like Wallerstein, Rostow’s approach was centred in Western culture and tended to ignore regionally differences. As well, it may be difficult to distinguish between stages as change occurs. Regardless, Rostow’s Five Stages of Economic Growth highlighted the need for investment, economic development and targeted foreign aid. Stage 1 Traditional Society - The economy is dominated by subsistence activity. Output is consumed by producers; it is not traded. Trade is barter where goods are exchanged directly for other goods. Agriculture is the most important industry. Production is labour intensive using only limited quantities of capital. Technology is limited, and resource allocation is determined very much by traditional methods of production. Stage 2 Transitional Stage (Preconditions for Takeoff) Increased specialization generates surpluses for trading. There is an emergence of a transport infrastructure to support trade. Entrepreneurs emerge as incomes, savings and investment grow. External trade also occurs concentrating on primary products. A strong central government encourages private enterprise. Stage 3 Take Off Industrialization increases with workers switching from the agricultural sector to the manufacturing sector. Growth is concentrated in a few regions of the country and within one or two manufacturing industries. The level of investment reaches over 10% of GNP. People save money. The economic transitions are accompanied by the evolution of new political and social institutions that support industrialization. The growth is self-sustaining as investment leads to increasing incomes in turn generating more savings to finance further investment. Stage 4 Drive to Maturity The economy is diversifying into new areas. Technological innovation is providing a diverse range of investment opportunities. The economy is producing a wide range of goods and services and there is less reliance on imports. Urbanization increases. Technology is used more widely. Stage 5 High Mass Consumption The economy is geared towards mass consumption, and the level of economic activity is very high. Technology is extensively used but its expansion slows. The service sector becomes increasingly dominant. Urbanization is complete. Now, multinationals emerge. Income for large numbers of persons transcends basic food, shelter and clothing. Increased interest in social welfare. Grade 12 World Issues - Unit 3 Lesson 1 World Economic Systems http://www.dogchurch.com/dogpac/weconomics.html Here is a practical…if not funny…way of thinking about political and economic systems. FEUDALISM - You have two cows. Your lord takes some of the milk. PURE SOCIALISM - You have two cows. The government takes them and puts them in a barn with everyone else's cows. You have to take care of all the cows. The government gives you as much milk as you need. BUREAUCRATIC SOCIALISM - You have two cows. The government takes them and puts them in a barn with everyone else's cows. They are cared for by ex-chicken farmers. You have to take care of the chickens the government took from the chicken farmers. The government gives you as much milk and eggs as the regulations say you should need. FASCISM - You have two cows. The government takes them both, hires you to take care of them and sells you the milk. PURE COMMUNISM - You have two cows. Your neighbors help you take care of them, and you all share the milk. RUSSIAN COMMUNISM - You have two cows. You have to take care of them, but the government takes all the milk. CAMBODIAN COMMUNISM - You have two cows. The government takes both and shoots you. DICTATORSHIP - You have two cows. The government takes both and drafts you. PURE DEMOCRACY - You have two cows. Your neighbors decide who gets the milk. REPRESENTATIVE DEMOCRACY - You have two cows. Yours neighbors pick someone to tell you who gets the milk. BUREAUCRACY - You have two cows. At first the government regulates what you can feed them and when you can milk them. Then it pays you not to milk them. Then it takes both, shoots one, milks the other one and pours the milk down the drain. Then it requires you to fill out forms accounting for the missing cows. In triplicate. PURE ANARCHY - You have two cows. Either you sell the milk at a fair price or your neighbors take the cows and kill you. CAPITALISM - You have two cows. You sell one and buy a bull. SURREALISM - You have two giraffes. The government requires you to take harmonica lessons.