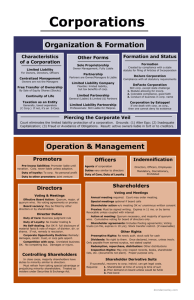

Corporations I

advertisement