Lesson Plan

advertisement

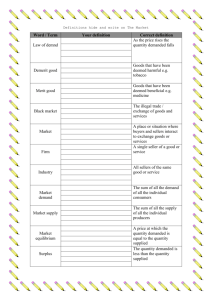

Lesson Plan – Law of Demand and Supply Aim of Lesson: The aim of this lesson is to introduce the students to the topic of markets and how markets work using the law of demand and the law of supply. Objective of Lesson: To define markets To explain what markets provide Examine the way in which markets work To define the law of demand To define the law of supply Identify what happens when demand exceeds supply Identify what happens when supply exceeds demand Explain how supply and demand affects choices To illustrate how markets and the law of demand and supply operate through class activity Materials Used: Whiteboard Overheads Textbook Tokens for bidding Chocolate bars Development 1 (lesson structure and methodology): Write the term ‘Markets’ on the whiteboard Ask the students if they can define what a market is Write their answers on the whiteboard, using a spider diagram Using an overhead show them the economic definition as follows: ‘A market is a mechanism by which potential buyers of a good or service are brought into contact with potential sellers of that good or service’. Explain simply that markets are where buyers and sellers meet Next discuss what economic questions markets provides answers to as follows: Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies 1. What goods should be produced (and in what quantities)? 2. For whom are goods produced? 3. How are the goods to be produced (what combination of the factors of production should be used)? 4. What rewards should be given to those who supply the factors of production? Explain to the students when you look at the above 4 points, it is obvious that a market is a group of people rather then a particular place Continue that while a market can be confined to a particular location e.g. the New York Stock Exchange and the London Stock Exchange, a market may also be dispersed, as is the market for foreign currencies which extends worldwide and is know as the Foreign Exchange market Ask for further examples of markets based on this example Next ask the students if a market can be created? Try and elicit ‘yes’ from them and ask for reasons why and how Give an examples to them such as if a new vaccine is discovered to cure cancer – a market now exists for that vaccine Another example will be the design of new technology e.g. playstation 3 or The Wii Sub-Development 1 (lesson structure and methodology) Next examine how markets work Coordinate a class activity to introduce students to this The activity will allow students personal involvement in the concept of supply and demand which helps the students see how it relates to their everyday life Students will be given a box of tokens with two colours in it, and asked to select any number of them from 1 to a handful Place a value on the tokens AFTER the students have already selected their tokens Then present a bar of chocolate and let the students know that they will only receive a homework free lesson if they own this selected item of which the teacher has EXACTLY one of. Announce the bidding to be open at 10cents and they may use their tokens to purchase the item Continue auction until a student has paid a high price for this item and received it Then pull out a class supply of chocolate – the same chocolate as already bid for Announce that actually there is more then one item and teacher is now willing to open bids at 1 cent Students will have a shocked reaction to this exercise Continue to explain that they have just experienced the law of demand and supply and explain these now in detail Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Sub-Development 2 (lesson structure and methodology) Explain to the students that every market works through the interaction of supply and demand. Explain the following points to the students When discussing the law of demand for a good we mean the quantity consumers are will to buy at different prices When discussing the law of supply, we mean the quantity that producers would be willing to make available at different prices A market works on the principle that there is some price that satisfies both consumers and producers. Emphasise to the student that this point is extremely important to know and understand. At this point ask the students if they have any questions and answer any that are posed Examine the situation from the view of the consumer and from the view of the producer Sub-Development 3 (lesson structure and methodology) First consider the consumer – the Law of Demand Demand can be defined as follows: If price rises, quantity demanded falls and if price falls, quantity demanded rises Put these statements on the overhead projector so students can read the statements again. Explain that the Law of Demand is very important to know as it will help us understand how consumers operate in markets Put an overhead on the projector illustrating the market for tea in Ireland – demonstrating the relationship between price and quantity This list will show the quantities that would be demanded at number of different prices. This table is called a demand schedule Examine this table with the class, and highlight to each student that quantity demanded and sold will increase as price decreases Then explain to the students that demand can also be illustrated graphically and this is known as a demand curve Show an overhead of the demand curve for the table previously discussed on the tea market in Ireland. Explain the Demand Curve to the students and instruct them to take it down in their copy books Sub-Development 4 (lesson structure and methodology) Next consider the situation from the point of the producer – Supply Supply can be defined as follows: If price rises, quantity supplied rises and if price falls, quantity supplied falls Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Put these statements on the overhead projector so students can read the statements again. Explain that Supply is very important to know as it will help us understand how producers operate in markets Staying with the examples of the tea market in Ireland, we will look at the supply schedule of tea and look at the relationship between price and quantity Then present this information on a supply curve – the economic method in which we view supply As a class discuss the differences between demand and supply Continue with explaining the term excess supply Excess supply exists when quantity supplied is greater then quantity demanded Producers have no option but to lower the prices S > D = P decreases Continue with explaining the term excess demand Excess demand exists when quantity demanded is greater then quantity supplied In this case consumers would compete against each other for the available supply and price would be forced to increase D > S = P increases Next explain the term Equilibrium Price This is where supply = demand. By equilibrium we mean a situation from which there is no tendency to change If the price on the market e.g. tea is above the equilibrium price, there will be a downward pressure on price. Quantity supplied will exceed quantity demanded and producers will lower their price to get rid of surplus stock If the price on the market e.g. tea is below the equilibrium price, there will be an upward pressure on price. Quantity demanded will exceed quantity supplied and consumers will be competing for a limited supply of the good. Scarcity would exist and price would increase If no interference in the market occurs (by government of other agency), price will eventually settle at a level where quantity demanded equals quantity supplied. This position is called the market equilibrium Having defined demand and supply ask the student that bought the overpriced bar of chocolate to define what these terms mean to him in light of the experience he just had, explain why he was motivated to pay such a high price for it, and let us know if he would have paid so much if he had know there were enough chocolate bars to go around. Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Lesson Plan on the topic of ‘Supply’ Aim of Lesson: The aim of this lesson is to incorporate the information students have learned from the topic ‘supply’, into workbook, exam and life related questions. Students should confidently and competently recognise and understand the factors that affect the supply of a good and relate it to life examples. Objective of Lesson: Recap and discuss supply curves which are exceptions to the rule of supply Recap and discuss the 5 factors affecting the supply of a good Comprehension of the details involved in each factor Understanding of the shifts in supply curve – both in the negative effect and positive effect Efficiently answer questions on supply that are workbook related, exam related and related to their daily lives Encourage an appreciation of economics throughout the class Materials Used: Whiteboard Overheads Textbook PowerPoint presentation Products: salt + pepper, potatoes + pasta, beans + peas, coffee + hot chocolate Homework sheet Development 1 (lesson structure and methodology): Ask the students to explain the basic law of supply that relates to most products, eliciting the following: as price increases, supply increases (P increases = S increases). If price decreases, supply also decrease (P decreases = S decreases). Question from homework should illustrate how the law of demand operates. Correct this question according to the law of supply. Next examine the 3 exceptions to the rule of Supply. These exceptions are put into practice with homework questions Ask the students to explain the first exception to the law Supply. That exception is as follows: Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Exception 1 = Perfect Inelastic Supply o If the quantity supplied is fixed, so that an increase in price will not bring forth further suppliers and a fall in price will not result in less being supplied e.g. fresh fruit, vegetables, open-air markets Next complete homework question in class so that this issue can be illustrated in economic terms on a graph. The students will be asked to explain the shape of the graph and a student will draw this on the whiteboard Students will then explain the answer to the questions with reference to Exception 1 Next ask the students to explain the second exception to the law of supply. This exception is as follows: Exception 2 = a minimum price is established below which supply will be zero o Suppliers are able to impose a minimum price (P1). At prices below P1 nothing will be supplied. At prices above P1 the curve will revert back to its normal upward slope as increase in prices = increase in supply o E.g. trade union where there is a minimum wage Next complete homework question in class so that this issue can be illustrated in economic terms on a graph. The students will be asked to explain to me the shape of the graph and a student will draw this on the whiteboard Students will then explain the answer to the questions with reference to Exception 2 Next ask the students to explain the final exception to the law of supply. This exception is as follows: Exception 3 = the firm reaches its maximum output o Depicts a situation where the firm increases output as price increases, up to its maximum level of output Q1. Any increase in price above P1 will have no effect on quantity supplied because the firm is operating at full capacity Complete homework question in class so that this issue can be illustrated in economic terms on a graph. The students will be asked to explain to me the shape of the graph and another student will draw this on the whiteboard Students will then explain the answer to the questions with reference to Exception 3 Draw the diagrams again on the whiteboard as per their explanations As the class are completing the questions ask the students to give further examples to support these exceptions Sub-Development 1 (lesson structure and methodology) The next section of the lesson will recap the factors that affect the supply of a good. There are 5 overall factors to consider. Ask the students to list these 5 factors Ask the students to briefly explain each of the 5 factors clearly and with good explanation and ask for examples to support their explanations. The factors that affect the supply of goods are as follows: Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Supply of a good depends on its own price o Goods which obey the law of supply o If price rise, quantity supplied rises o If price falls, quantity supplied falls Supply of a good depends on the prices of related goods o If price of a related good rises, while the price of the good the firm is making now remains the same or falls, it becomes attractive for the firm to supply the good that has increased in price o An increase in price or a related good will cause a fall in the supply of Good Y o Consequently it will switch resources to the production of the relatively more high priced good o A fall in the price of a related goodwill cause an increase in the supply of Good Y Supply of a good depends on the cost of production o If there is an increase in the cost of production of Good Y, there will be a reduction in supply. This will cause the supply curve to shift to the left o Possible causes for an increase in the cost of production are as follows: A rise in labour costs A rise in the cost of raw materials An increase in tax A reduction in subsidies o Similarly a fall in the cost of production will cause an increase in the supply of Good Y and will cause the supply curve to shift to the right o Possible causes for a decrease in the cost of production are as follows: A fall in labour costs A fall in the cost of raw materials A reduction in tax An increase in subsidies Supply of a good depends on the state of technology o The methods of production available to the firm. As technology advances it improves the productivity of the firm and therefore increases supply o The supply curve will shift to the right o It is important to note that we do not discuss a ‘fall’ in the state of technology. This is because we assume that any method of production available to the firm now will always remain an option to the firm Supply of a good depends on the factors outside the control of the firm o Factors that are not planned in advance by the producer o Favourable unplanned factors E.g. favourable weather conditions Causes a shift in the supply curve to the right = increase in supply o Unfavourable unplanned factors E.g. a strike Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Causes a shift in the supply curve to the left = decrease in supply When students have completed listing and explaining the 5 factors affecting supply the teacher will write the supply function on the whiteboard as follows: Sy = f(Py, Pr, C, T, U) Continue with the homework. Question 4 incorporates all of the factors discussed above. Put up an overhead of a supply curve and for each point on question 4 the students will inform the teacher what happens to the supply curve and teacher will amend it with a whiteboard marker as required. Briefly recap the concept of supply using a PowerPoint presentation which will illustrate the shifts in the supply curves from a negative and a positive perspective. Sub-Development 2 (lesson structure and methodology) The final part of the lesson will involve group work and a group exercise. Students will be split into groups of 5 (4 groups all together) A team leader will be designated to keep the worksheet safe and complete the analysis in writing on behalf of the team Give each group 2 related products. The products are as follows: Salt + pepper Pasta + Potatoes Beans + Peas Coffee + hot chocolate With these products give them a worksheet with a certain amount of information (see attached) The group will be required to discuss the products and information supplied and plot their analysis on a supply curve As the students are undertaking this exercise, the teacher will walk around the classroom This is to ensure teacher is available for questioning by the students and also to ensure management of the group work and maintain discipline If time allows discuss the analysis from each team. Otherwise begin the next lesson with their analysis and suggestions Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Lesson Plan - Markets Aim of Lesson: The aim of this lesson is to continue the topic of with the topic of markets, explaining how the laws of demand and the law of supply apply to the various markets. Objective of Lesson: To recap on the definition of markets To discuss what markets provide Examine the way in which markets work To discuss the types of markets To examine markets in operation To recap on the definition and explanation of the law of demand To recap on the definition and explanation of the law of supply Examine what happens when demand exceeds supply Examine what happens when supply exceeds demand Explain how supply and demand affects choices Define and discuss excess supply and excess demand Define and discuss equilibrium price Discuss shifts in the supply and demand curves To illustrate how markets and the law of demand and supply operate through class activity Materials Used: Whiteboard Overheads Textbook Newspaper clipping handout PowerPoint presentation Index price cards Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Introduction: . Ask the students to take out the newspaper clipping from the previous lesson. This clipping was on the product Playstation 3 which was not available in Europe until March 2007. A British man paid over €11,000 for an advance copy of the product. This is a great example of demand and supply that the students can relate to. Development 1 (lesson structure and methodology): Write the term ‘Markets’ on the whiteboard Students were asked in the workbooks to define a market, so a good definition is expected Randomly choose a student to answer this question Using an overhead support this answer using the economic definition as follows: ‘A market is a mechanism by which potential buyers of a good or service are brought into contact with potential sellers of that good or service’. Ask the students to explain simply what are markets, eliciting the point that markets are where buyers and sellers meet Next recap on what economic questions do markets provides answers to. Ask students randomly to elicit the following points: 5. What goods should be produced (and in what quantities)? 6. For whom are goods produced? 7. How are the goods to be produced (what combination of the factors of production should be used)? 8. What rewards should be given to those who supply the factors of production? Next ask students where one would find a market – eliciting as many examples as possible including the following: 1. A market can be confined to a particular location e.g. the New York Stock Exchange and the London Stock Exchange 2. A market may also be dispersed, as is the market for foreign currencies which extends worldwide and is know as the Foreign Exchange market Ask for further examples of markets based on this example Next ask students for examples of markets that can be created and list these on the whiteboard using a spider diagram Sub-Development 1 (lesson structure and methodology) Ask students to close their workbooks and test books for the time being so that the class may examine markets in greater detail Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Explain to the students that there are 3 categories of market in our economies. These are as follows: 1. Factor Markets 2. Intermediate Markets / Producer Markets 3. Final Markets / Goods Markets Examine each of these markets in detail individually Factor Markets: A factor market is a market where a factor of production is bought and sold The buyer is the entrepreneur who wants to use the factor in the production of goods and services The seller is the owner of the factor of production in question Price is determined in the same way – this represents income to the owner of the factor of production Rent = income to the owner of the land Wages = the reward to the supplier of labour Interest = the return to the owner of capital Intermediate Markets / Producer Markets An intermediate market is one where output (i.e. raw material) is sold to be used as input in the production of another good Example: the output of the steel industry is bought by car manufacturing firms in the making of cars Final Markets / Goods Markets Final markets are markets that deal in goods and services that give consumers utility and for which they are therefore prepared to pay a price Examples: food, drink, clothing, furniture, household appliances For each market, elicit as many examples as possible of each market and draw these on the whiteboard At this point ask the students if they have any questions and answer any that are posed Sub-Development 2 (lesson structure and methodology) Re-explain to the students that every market works through the interaction of supply and demand. Ask the students what we mean when discussing the law of demand for a good eliciting the following: ‘we mean the quantity consumers are willing to buy at different prices’ Next ask the students what we mean when discussing the law of supply, eliciting the following: ‘we mean the quantity that producers would be willing to make available at different prices’ A market works on the principle that there is some price that satisfies both consumers and producers. Emphasise to the student that this point is extremely important to know and understand. At this point ask the students if they have any questions and answer any that are posed Examine the situation from the view of the consumer and from the view of the producer using different examples Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Sub-Development 3 (lesson structure and methodology) First consider the consumer and recap the Law of Demand Ask the students to define demand. Demand can be defined as follows: If price rises, quantity demanded falls and if price falls, quantity demanded rises Put this statement on the overhead projector so students can read the statements again. Again explain to the students that the Law of Demand is very important to know as it will help us understand how consumers operate in markets Next consider the situation from the point of the producer and recap on the Law of Supply Ask the students to define supply. Supply can be defined as follows: If price rises, quantity supplied rises and if price falls, quantity supplied falls Put this statement on the overhead projector so students can read the statements again. Explain that Supply is very important to know as it will help us understand how producers operate in markets Sub-Development 4 (lesson structure and methodology) Next recap on the Demand Schedule and Demand Curve. The teacher wants to ensure that students understand this extremely well as it is vital for many areas of economics Put an overhead on the projector illustrating the market for tea in Ireland – demonstrating the relationship between price and quantity This list will show the quantities that would be demanded at number of different prices. Ask the students what this table is called eliciting the following: a demand schedule Examine this table as a class, and highlight to each student that quantity demanded and sold will increase as price decreases Then explain to the students that demand can also be illustrated graphically. Ask the students what this graph is called, eliciting that this is known as a demand curve Then show an overhead of the demand curve for the table previously discussed on the tea market in Ireland. Explain the Demand Curve to the students and instruct them to take it down in their copy books Staying with the examples of the tea market in Ireland, look at the supply schedule of tea and look at the relationship between price and quantity Then present this information on a supply curve Discuss as a class the differences between demand and supply Continue with explaining the term excess supply Excess supply exists when quantity supplied is greater then quantity demanded Producers have no option but to lower the prices S > D = P decreases Next explain the term excess demand Excess demand exists when quantity demanded is greater then quantity supplied Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies In this case consumers would compete against each other for the available supply and price would be forced to increase D > S = P increases Next explain the term Equilibrium Price This is where supply = demand. By equilibrium we mean a situation from which there is no tendency to change If the price on the market e.g. tea is above the equilibrium price, there will be a downward pressure on price. Quantity supplied will exceed quantity demanded and producers will lower their price to get rid of surplus stock If the price on the market e.g. tea is below the equilibrium price, there will be an upward pressure on price. Quantity demanded will exceed quantity supplied and consumers will be competing for a limited supply of the good. Scarcity would exist and price would increase If no interference in the market occurs (by government of other agency), price will eventually settle at a level where quantity demanded equals quantity supplied. This position is called the market equilibrium Having defined demand and supply hand the students a copy of an old newspaper article advertising Playstation 3. The product has not yet launched on the European market and a customer paid over €11,000 for an advance version of the product. Discuss the laws of demand and supply in relation to this particular product Sub-Development 5 (lesson structure and methodology) Next present the students with a PowerPoint presentation This presentation will illustrate how the laws of demand and supply apply to factor markets and to goods markets This presentation will demand and supply in terms of equations and how they are represented on supply and demand curves It will also take into consideration what happens if there is a shortage in either of these markets Discuss the shifts in the demand curve and the shifts in the supply curve The final part of the presentation will take into account the equilibrium price As a product use the example of potatoes The PowerPoint presentation will illustrate effectively the demand / supply schedules on demand / supply curves It will also hold the students interest as it is creative and technologically orientated which students understand and have an interest in. Sub-Development 6 (lesson structure and methodology) For the final part of class, carry out a class activity as follows: Students will be asked to think of three items on their desks and to secretly set a price for each one of them on the index card that will be handed out the each one. Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies They will then fold their index cards so it can stand upright on their desks Students will then be instructed to place their items by their price list Students will then be invited to go ‘shopping’ and check out all the prices in the ‘shop’ Lead the students into discussion asking questions such as the following: Now that you can see how other merchants priced their items, how will it effect your pricing of the same item Were there some items that would be in high demand because of their low supply? How might that effect pricing? Students may want to stock their ‘shelves’ differently after doing some comparisonshopping and seeing the availability of certain items. Give the students the opportunity to price another 3 items of their choice and discuss their changes and why they were made. Lesson Plan – Law of Demand and Supply Aim of Lesson: The aim of this lesson is to introduce the students to the topic of markets and how markets work using the law of demand and the law of supply. Objective of Lesson: To define markets To explain what markets provide Examine the way in which markets work To define the law of demand To define the law of supply Identify what happens when demand exceeds supply Identify what happens when supply exceeds demand Explain how supply and demand affects choices To illustrate how markets and the law of demand and supply operate through class activity Materials Used: Whiteboard Overheads Textbook Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Tokens for bidding Chocolate bars Development 1 (lesson structure and methodology): Write the term ‘Markets’ on the whiteboard Ask the students if they can define what a market is Write their answers on the whiteboard, using a spider diagram Using an overhead show them the economic definition as follows: ‘A market is a mechanism by which potential buyers of a good or service are brought into contact with potential sellers of that good or service’. Explain simply that markets are where buyers and sellers meet Next discuss what economic questions markets provides answers to as follows: 9. What goods should be produced (and in what quantities)? 10. For whom are goods produced? 11. How are the goods to be produced (what combination of the factors of production should be used)? 12. What rewards should be given to those who supply the factors of production? Explain to the students when you look at the above 4 points, it is obvious that a market is a group of people rather then a particular place Continue that while a market can be confined to a particular location e.g. the New York Stock Exchange and the London Stock Exchange, a market may also be dispersed, as is the market for foreign currencies which extends worldwide and is know as the Foreign Exchange market Ask for further examples of markets based on this example Next ask the students if a market can be created? Try and elicit ‘yes’ from them and ask for reasons why and how Give an examples to them such as if a new vaccine is discovered to cure cancer – a market now exists for that vaccine Another example will be the design of new technology e.g. playstation 3 or The Wii Sub-Development 1 (lesson structure and methodology) Next examine how markets work Coordinate a class activity to introduce students to this The activity will allow students personal involvement in the concept of supply and demand which helps the students see how it relates to their everyday life Students will be given a box of tokens with two colours in it, and asked to select any number of them from 1 to a handful Place a value on the tokens AFTER the students have already selected their tokens Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Then present a bar of chocolate and let the students know that they will only receive a homework free lesson if they own this selected item of which the teacher has EXACTLY one of. Announce the bidding to be open at 10cents and they may use their tokens to purchase the item Continue auction until a student has paid a high price for this item and received it Then pull out a class supply of chocolate – the same chocolate as already bid for Announce that actually there is more then one item and teacher is now willing to open bids at 1 cent Students will have a shocked reaction to this exercise Continue to explain that they have just experienced the law of demand and supply and explain these now in detail Sub-Development 2 (lesson structure and methodology) Explain to the students that every market works through the interaction of supply and demand. Explain the following points to the students When discussing the law of demand for a good we mean the quantity consumers are will to buy at different prices When discussing the law of supply, we mean the quantity that producers would be willing to make available at different prices A market works on the principle that there is some price that satisfies both consumers and producers. Emphasise to the student that this point is extremely important to know and understand. At this point ask the students if they have any questions and answer any that are posed Examine the situation from the view of the consumer and from the view of the producer Sub-Development 3 (lesson structure and methodology) First consider the consumer – the Law of Demand Demand can be defined as follows: If price rises, quantity demanded falls and if price falls, quantity demanded rises Put these statements on the overhead projector so students can read the statements again. Explain that the Law of Demand is very important to know as it will help us understand how consumers operate in markets Put an overhead on the projector illustrating the market for tea in Ireland – demonstrating the relationship between price and quantity This list will show the quantities that would be demanded at number of different prices. This table is called a demand schedule Examine this table with the class, and highlight to each student that quantity demanded and sold will increase as price decreases Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Then explain to the students that demand can also be illustrated graphically and this is known as a demand curve Show an overhead of the demand curve for the table previously discussed on the tea market in Ireland. Explain the Demand Curve to the students and instruct them to take it down in their copy books Sub-Development 4 (lesson structure and methodology) Next consider the situation from the point of the producer – Supply Supply can be defined as follows: If price rises, quantity supplied rises and if price falls, quantity supplied falls Put these statements on the overhead projector so students can read the statements again. Explain that Supply is very important to know as it will help us understand how producers operate in markets Staying with the examples of the tea market in Ireland, we will look at the supply schedule of tea and look at the relationship between price and quantity Then present this information on a supply curve – the economic method in which we view supply As a class discuss the differences between demand and supply Continue with explaining the term excess supply Excess supply exists when quantity supplied is greater then quantity demanded Producers have no option but to lower the prices S > D = P decreases Continue with explaining the term excess demand Excess demand exists when quantity demanded is greater then quantity supplied In this case consumers would compete against each other for the available supply and price would be forced to increase D > S = P increases Next explain the term Equilibrium Price This is where supply = demand. By equilibrium we mean a situation from which there is no tendency to change If the price on the market e.g. tea is above the equilibrium price, there will be a downward pressure on price. Quantity supplied will exceed quantity demanded and producers will lower their price to get rid of surplus stock If the price on the market e.g. tea is below the equilibrium price, there will be an upward pressure on price. Quantity demanded will exceed quantity supplied and consumers will be competing for a limited supply of the good. Scarcity would exist and price would increase If no interference in the market occurs (by government of other agency), price will eventually settle at a level where quantity demanded equals quantity supplied. This position is called the market equilibrium Having defined demand and supply ask the student that bought the overpriced bar of chocolate to define what these terms mean to him in light of the experience he just had, Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies explain why he was motivated to pay such a high price for it, and let us know if he would have paid so much if he had know there were enough chocolate bars to go around. Lesson Plan on the topic of ‘Supply’ Aim of Lesson: The aim of this lesson is to incorporate the information students have learned from the topic ‘supply’, into workbook, exam and life related questions. Students should confidently and competently recognise and understand the factors that affect the supply of a good and relate it to life examples. Objective of Lesson: Recap and discuss supply curves which are exceptions to the rule of supply Recap and discuss the 5 factors affecting the supply of a good Comprehension of the details involved in each factor Understanding of the shifts in supply curve – both in the negative effect and positive effect Efficiently answer questions on supply that are workbook related, exam related and related to their daily lives Encourage an appreciation of economics throughout the class Materials Used: Whiteboard Overheads Textbook PowerPoint presentation Products: salt + pepper, potatoes + pasta, beans + peas, coffee + hot chocolate Homework sheet Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Development 1 (lesson structure and methodology): Ask the students to explain the basic law of supply that relates to most products, eliciting the following: as price increases, supply increases (P increases = S increases). If price decreases, supply also decrease (P decreases = S decreases). Question from homework should illustrate how the law of demand operates. Correct this question according to the law of supply. Next examine the 3 exceptions to the rule of Supply. These exceptions are put into practice with homework questions Ask the students to explain the first exception to the law Supply. That exception is as follows: Exception 1 = Perfect Inelastic Supply o If the quantity supplied is fixed, so that an increase in price will not bring forth further suppliers and a fall in price will not result in less being supplied e.g. fresh fruit, vegetables, open-air markets Next complete homework question in class so that this issue can be illustrated in economic terms on a graph. The students will be asked to explain the shape of the graph and a student will draw this on the whiteboard Students will then explain the answer to the questions with reference to Exception 1 Next ask the students to explain the second exception to the law of supply. This exception is as follows: Exception 2 = a minimum price is established below which supply will be zero o Suppliers are able to impose a minimum price (P1). At prices below P1 nothing will be supplied. At prices above P1 the curve will revert back to its normal upward slope as increase in prices = increase in supply o E.g. trade union where there is a minimum wage Next complete homework question in class so that this issue can be illustrated in economic terms on a graph. The students will be asked to explain to me the shape of the graph and a student will draw this on the whiteboard Students will then explain the answer to the questions with reference to Exception 2 Next ask the students to explain the final exception to the law of supply. This exception is as follows: Exception 3 = the firm reaches its maximum output o Depicts a situation where the firm increases output as price increases, up to its maximum level of output Q1. Any increase in price above P1 will have no effect on quantity supplied because the firm is operating at full capacity Complete homework question in class so that this issue can be illustrated in economic terms on a graph. The students will be asked to explain to me the shape of the graph and another student will draw this on the whiteboard Students will then explain the answer to the questions with reference to Exception 3 Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Draw the diagrams again on the whiteboard as per their explanations As the class are completing the questions ask the students to give further examples to support these exceptions Sub-Development 1 (lesson structure and methodology) The next section of the lesson will recap the factors that affect the supply of a good. There are 5 overall factors to consider. Ask the students to list these 5 factors Ask the students to briefly explain each of the 5 factors clearly and with good explanation and ask for examples to support their explanations. The factors that affect the supply of goods are as follows: Supply of a good depends on its own price o Goods which obey the law of supply o If price rise, quantity supplied rises o If price falls, quantity supplied falls Supply of a good depends on the prices of related goods o If price of a related good rises, while the price of the good the firm is making now remains the same or falls, it becomes attractive for the firm to supply the good that has increased in price o An increase in price or a related good will cause a fall in the supply of Good Y o Consequently it will switch resources to the production of the relatively more high priced good o A fall in the price of a related goodwill cause an increase in the supply of Good Y Supply of a good depends on the cost of production o If there is an increase in the cost of production of Good Y, there will be a reduction in supply. This will cause the supply curve to shift to the left o Possible causes for an increase in the cost of production are as follows: A rise in labour costs A rise in the cost of raw materials An increase in tax A reduction in subsidies o Similarly a fall in the cost of production will cause an increase in the supply of Good Y and will cause the supply curve to shift to the right o Possible causes for a decrease in the cost of production are as follows: A fall in labour costs A fall in the cost of raw materials A reduction in tax An increase in subsidies Supply of a good depends on the state of technology Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies o The methods of production available to the firm. As technology advances it improves the productivity of the firm and therefore increases supply o The supply curve will shift to the right o It is important to note that we do not discuss a ‘fall’ in the state of technology. This is because we assume that any method of production available to the firm now will always remain an option to the firm Supply of a good depends on the factors outside the control of the firm o Factors that are not planned in advance by the producer o Favourable unplanned factors E.g. favourable weather conditions Causes a shift in the supply curve to the right = increase in supply o Unfavourable unplanned factors E.g. a strike Causes a shift in the supply curve to the left = decrease in supply When students have completed listing and explaining the 5 factors affecting supply the teacher will write the supply function on the whiteboard as follows: Sy = f(Py, Pr, C, T, U) Continue with the homework. Question 4 incorporates all of the factors discussed above. Put up an overhead of a supply curve and for each point on question 4 the students will inform the teacher what happens to the supply curve and teacher will amend it with a whiteboard marker as required. Briefly recap the concept of supply using a PowerPoint presentation which will illustrate the shifts in the supply curves from a negative and a positive perspective. Sub-Development 2 (lesson structure and methodology) The final part of the lesson will involve group work and a group exercise. Students will be split into groups of 5 (4 groups all together) A team leader will be designated to keep the worksheet safe and complete the analysis in writing on behalf of the team Give each group 2 related products. The products are as follows: Salt + pepper Pasta + Potatoes Beans + Peas Coffee + hot chocolate With these products give them a worksheet with a certain amount of information (see attached) The group will be required to discuss the products and information supplied and plot their analysis on a supply curve As the students are undertaking this exercise, the teacher will walk around the classroom Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies This is to ensure teacher is available for questioning by the students and also to ensure management of the group work and maintain discipline If time allows discuss the analysis from each team. Otherwise begin the next lesson with their analysis and suggestions Lesson Plan - Markets Aim of Lesson: The aim of this lesson is to continue the topic of with the topic of markets, explaining how the laws of demand and the law of supply apply to the various markets. Objective of Lesson: To recap on the definition of markets To discuss what markets provide Examine the way in which markets work To discuss the types of markets To examine markets in operation To recap on the definition and explanation of the law of demand To recap on the definition and explanation of the law of supply Examine what happens when demand exceeds supply Examine what happens when supply exceeds demand Explain how supply and demand affects choices Define and discuss excess supply and excess demand Define and discuss equilibrium price Discuss shifts in the supply and demand curves To illustrate how markets and the law of demand and supply operate through class activity Materials Used: Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Whiteboard Overheads Textbook Newspaper clipping handout PowerPoint presentation Index price cards Introduction: . Ask the students to take out the newspaper clipping from the previous lesson. This clipping was on the product Playstation 3 which was not available in Europe until March 2007. A British man paid over €11,000 for an advance copy of the product. This is a great example of demand and supply that the students can relate to. Development 1 (lesson structure and methodology): Write the term ‘Markets’ on the whiteboard Students were asked in the workbooks to define a market, so a good definition is expected Randomly choose a student to answer this question Using an overhead support this answer using the economic definition as follows: ‘A market is a mechanism by which potential buyers of a good or service are brought into contact with potential sellers of that good or service’. Ask the students to explain simply what are markets, eliciting the point that markets are where buyers and sellers meet Next recap on what economic questions do markets provides answers to. Ask students randomly to elicit the following points: 13. What goods should be produced (and in what quantities)? 14. For whom are goods produced? 15. How are the goods to be produced (what combination of the factors of production should be used)? 16. What rewards should be given to those who supply the factors of production? Next ask students where one would find a market – eliciting as many examples as possible including the following: Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies 3. A market can be confined to a particular location e.g. the New York Stock Exchange and the London Stock Exchange 4. A market may also be dispersed, as is the market for foreign currencies which extends worldwide and is know as the Foreign Exchange market Ask for further examples of markets based on this example Next ask students for examples of markets that can be created and list these on the whiteboard using a spider diagram Sub-Development 1 (lesson structure and methodology) Ask students to close their workbooks and test books for the time being so that the class may examine markets in greater detail Explain to the students that there are 3 categories of market in our economies. These are as follows: 4. Factor Markets 5. Intermediate Markets / Producer Markets 6. Final Markets / Goods Markets Examine each of these markets in detail individually Factor Markets: A factor market is a market where a factor of production is bought and sold The buyer is the entrepreneur who wants to use the factor in the production of goods and services The seller is the owner of the factor of production in question Price is determined in the same way – this represents income to the owner of the factor of production Rent = income to the owner of the land Wages = the reward to the supplier of labour Interest = the return to the owner of capital Intermediate Markets / Producer Markets An intermediate market is one where output (i.e. raw material) is sold to be used as input in the production of another good Example: the output of the steel industry is bought by car manufacturing firms in the making of cars Final Markets / Goods Markets Final markets are markets that deal in goods and services that give consumers utility and for which they are therefore prepared to pay a price Examples: food, drink, clothing, furniture, household appliances For each market, elicit as many examples as possible of each market and draw these on the whiteboard At this point ask the students if they have any questions and answer any that are posed Sub-Development 2 (lesson structure and methodology) Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Re-explain to the students that every market works through the interaction of supply and demand. Ask the students what we mean when discussing the law of demand for a good eliciting the following: ‘we mean the quantity consumers are willing to buy at different prices’ Next ask the students what we mean when discussing the law of supply, eliciting the following: ‘we mean the quantity that producers would be willing to make available at different prices’ A market works on the principle that there is some price that satisfies both consumers and producers. Emphasise to the student that this point is extremely important to know and understand. At this point ask the students if they have any questions and answer any that are posed Examine the situation from the view of the consumer and from the view of the producer using different examples Sub-Development 3 (lesson structure and methodology) First consider the consumer and recap the Law of Demand Ask the students to define demand. Demand can be defined as follows: If price rises, quantity demanded falls and if price falls, quantity demanded rises Put this statement on the overhead projector so students can read the statements again. Again explain to the students that the Law of Demand is very important to know as it will help us understand how consumers operate in markets Next consider the situation from the point of the producer and recap on the Law of Supply Ask the students to define supply. Supply can be defined as follows: If price rises, quantity supplied rises and if price falls, quantity supplied falls Put this statement on the overhead projector so students can read the statements again. Explain that Supply is very important to know as it will help us understand how producers operate in markets Sub-Development 4 (lesson structure and methodology) Next recap on the Demand Schedule and Demand Curve. The teacher wants to ensure that students understand this extremely well as it is vital for many areas of economics Put an overhead on the projector illustrating the market for tea in Ireland – demonstrating the relationship between price and quantity This list will show the quantities that would be demanded at number of different prices. Ask the students what this table is called eliciting the following: a demand schedule Examine this table as a class, and highlight to each student that quantity demanded and sold will increase as price decreases Then explain to the students that demand can also be illustrated graphically. Ask the students what this graph is called, eliciting that this is known as a demand curve Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies Then show an overhead of the demand curve for the table previously discussed on the tea market in Ireland. Explain the Demand Curve to the students and instruct them to take it down in their copy books Staying with the examples of the tea market in Ireland, look at the supply schedule of tea and look at the relationship between price and quantity Then present this information on a supply curve Discuss as a class the differences between demand and supply Continue with explaining the term excess supply Excess supply exists when quantity supplied is greater then quantity demanded Producers have no option but to lower the prices S > D = P decreases Next explain the term excess demand Excess demand exists when quantity demanded is greater then quantity supplied In this case consumers would compete against each other for the available supply and price would be forced to increase D > S = P increases Next explain the term Equilibrium Price This is where supply = demand. By equilibrium we mean a situation from which there is no tendency to change If the price on the market e.g. tea is above the equilibrium price, there will be a downward pressure on price. Quantity supplied will exceed quantity demanded and producers will lower their price to get rid of surplus stock If the price on the market e.g. tea is below the equilibrium price, there will be an upward pressure on price. Quantity demanded will exceed quantity supplied and consumers will be competing for a limited supply of the good. Scarcity would exist and price would increase If no interference in the market occurs (by government of other agency), price will eventually settle at a level where quantity demanded equals quantity supplied. This position is called the market equilibrium Having defined demand and supply hand the students a copy of an old newspaper article advertising Playstation 3. The product has not yet launched on the European market and a customer paid over €11,000 for an advance version of the product. Discuss the laws of demand and supply in relation to this particular product Sub-Development 5 (lesson structure and methodology) Next present the students with a PowerPoint presentation This presentation will illustrate how the laws of demand and supply apply to factor markets and to goods markets This presentation will demand and supply in terms of equations and how they are represented on supply and demand curves It will also take into consideration what happens if there is a shortage in either of these markets Discuss the shifts in the demand curve and the shifts in the supply curve Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies The final part of the presentation will take into account the equilibrium price As a product use the example of potatoes The PowerPoint presentation will illustrate effectively the demand / supply schedules on demand / supply curves It will also hold the students interest as it is creative and technologically orientated which students understand and have an interest in. Sub-Development 6 (lesson structure and methodology) For the final part of class, carry out a class activity as follows: Students will be asked to think of three items on their desks and to secretly set a price for each one of them on the index card that will be handed out the each one. They will then fold their index cards so it can stand upright on their desks Students will then be instructed to place their items by their price list Students will then be invited to go ‘shopping’ and check out all the prices in the ‘shop’ Lead the students into discussion asking questions such as the following: Now that you can see how other merchants priced their items, how will it effect your pricing of the same item Were there some items that would be in high demand because of their low supply? How might that effect pricing? Students may want to stock their ‘shelves’ differently after doing some comparisonshopping and seeing the availability of certain items. Give the students the opportunity to price another 3 items of their choice and discuss their changes and why they were made. v Trudie Murray© St. Patrick’s College, Cork City Economics Methodologies